Belgium: 2019 Article IV Consultation Concluding Statement

December 14, 2018

Important reforms implemented in recent years have supported growth and jobs in Belgium. But the reform agenda is unfinished and risks are rising. In this context, we encourage the authorities to take advantage of favorable economic conditions to press ahead with further reforms to enhance the economy’s resilience and boost its growth potential. The priorities should be to:

- Move toward a balanced budget in the medium term by making government spending more efficient.

- Continue to address labor market fragmentation and support the integration of vulnerable groups by improving incentives to work, strengthening education and training, reducing barriers to mobility, and better linking wages to productivity.

- Boost productivity growth by supporting entrepreneurship, increasing investment in infrastructure, strengthening competition in services, and streamlining regulations.

- Closely monitor the build-up of cyclical risks in the financial sector and stand ready to tighten macroprudential policy further.

Context

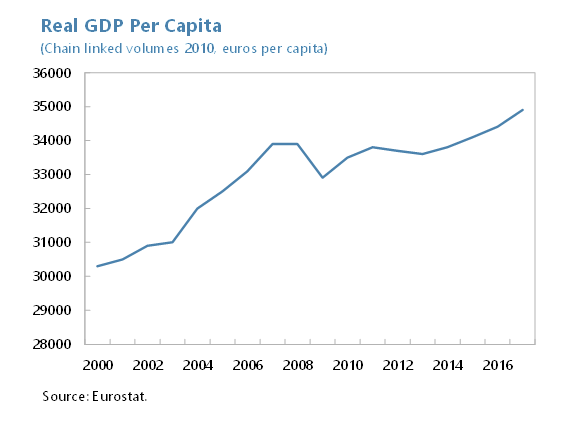

1. A decade after the onset of the global financial crisis, Belgium has achieved significant economic progress, supported by ambitious reforms. The economy has experienced nine consecutive years of expansion. Real GDP per capita has surpassed pre-crisis levels and employment is at historical highs. The government has contributed to these positive outcomes by delivering on much of its economic reform agenda, including a key pension reform, an overhaul of the corporate income tax regime, a reduction in labor taxes under the “tax shift,” and other labor market reforms to promote flexibility and strengthen competitiveness. The financial sector has also become more resilient thanks to structural changes and an improved regulatory and supervisory framework.

2. But there is scope to raise potential growth further and strengthen the resilience of the economy. Although Belgium weathered the crisis better than most of its peers, growth has slowed recently and is expected to remain modest at 1½ percent next year and over the medium term. Moreover, the economy is exposed to rising external risks related to escalating protectionism, higher energy prices, uncertainty related to Brexit, and increased financial turbulence in Europe. Domestic risks relate to a slowdown in the reform momentum in the context of upcoming elections. Thus, Belgium’s central challenge is to continue to build the foundation for higher potential growth while enhancing buffers against shocks.

Rebuilding fiscal buffers

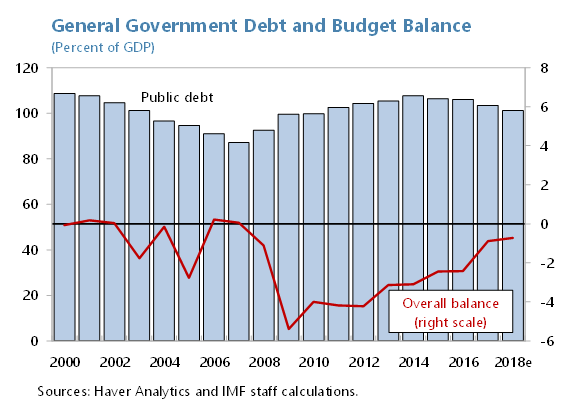

3. The government needs to do more to place public debt on a sustained downward path. The authorities have taken a number of measures to reduce the fiscal deficit and debt in recent years. Nonetheless, the deficit has not returned to pre-crisis levels despite nearly a decade of economic expansion, and it is expected to widen further, partly as a result of previously legislated tax relief coming into effect over the medium term. Public debt remains the fifth highest in the euro area at over 100 percent of GDP, leaving Belgium with little room to maneuver in the event of future shocks. In this context, the government should reduce the structural deficit by about ½ percent of GDP per year until structural balance is reached. This will require measures beyond what is included in the 2019 draft budget. Strengthened coordination at all levels of government will be critical for Belgium to achieve its fiscal goals.

4. Achieving a more sustainable fiscal position hinges on making spending more efficient. At over 50 percent of GDP, Belgium has one of the highest spending ratios in Europe, even as its public investment is among the lowest. The government should reduce duplication in the public administration, streamline the civil service, curtail the high level of subsidies, and better target social benefits to the most vulnerable. This will reduce the deficit and also create space for needed investment in infrastructure and preparations for the energy transition. Moreover, as population aging will add to pension and healthcare spending, the authorities should build on previous reforms to further bolster the sustainability of the pension system. Spending reforms should be complemented by measures to safeguard revenues, including further reducing certain deductions and exemptions. Further revenue-neutral reductions in labor taxation could also be considered, which would support employment and growth.

Raising potential output

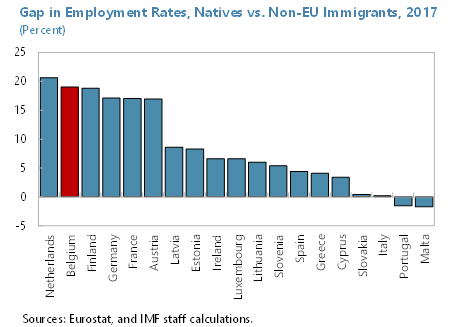

5. Reforms to reduce the fragmentation of the labor market are key to supporting higher, more inclusive growth. Despite strong gains in employment owing in part to recent reforms, vulnerable groups—especially non-EU immigrants, the young, and the low-skilled—remain largely excluded from the labor market. Moreover, regional disparities in competitiveness and unemployment persist, and labor supply-demand mismatches are widespread. The jobs deal agreed over the summer contains welcome measures to encourage labor force participation and should be implemented without delay, including the reform of the unemployment benefits system. But more efforts are needed to address educational gaps, improve the quality of training and lifelong learning, and reduce barriers to mobility, especially for vulnerable groups. Better linking wages with productivity can help to improve the allocation of resources and support overall competitiveness.

6. Unlocking the economy’s growth potential also requires removing bottlenecks to business growth. Belgium suffers from anemic business dynamism and a weak entrepreneurial culture, as evidenced by low rates of entry and exit of firms and a relatively low share of high-growth firms. The government’s initiative to promote equity financing and develop an ecosystem for young, innovative firms with growth potential is encouraging. But the authorities should not stop there. Further efforts are needed to streamline and harmonize regulations, increase investment in infrastructure, including in energy, improve the efficiency of R&D spending, and strengthen competition in services (particularly in regulated professions).

Safeguarding financial sector stability

7. The financial sector has become more resilient since the crisis, but new challenges are emerging. Banks have reduced their balance sheets, bolstered capital and liquidity buffers, and adopted more conservative business models. Nevertheless, increased competition in an environment of low interest rates has weighed on interest margins, fueled strong credit growth, and led to weakening credit standards. This has resulted in rising corporate and household debt and pushed up housing prices, posing risks to asset quality. External risks related to global financial market volatility and uncertainty related to Brexit add to challenges.

8. In this context, the authorities should monitor vulnerabilities closely and stand ready to take proactive action as needed. We welcome the new macroprudential measures aimed at the housing market and encourage the authorities to stand ready to activate the countercyclical capital buffer to build up further resilience, should cyclical risks persist or intensify. The authorities could also consider revising the framework for macroprudential decision-making to ensure the ability to deploy a broad range of macroprudential policies in a timely manner. At the same time, the supervisory authorities need to continue to enhance risk monitoring and ensure the feasibility and effectiveness of bank resolution strategies. We also encourage them to enhance preparedness of the financial and non-financial sectors for Brexit.

The mission thanks the authorities for their constructive policy dialogue and kind hospitality.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: Gediminas Vilkas

Phone: +1 202 623-7100Email: MEDIA@IMF.org