Emerging markets hold both the reins of future growth and the keys to the future of multilateralism

As advanced economies turn increasingly inward, emerging markets have an important stake in the defense against global economic fragmentation.

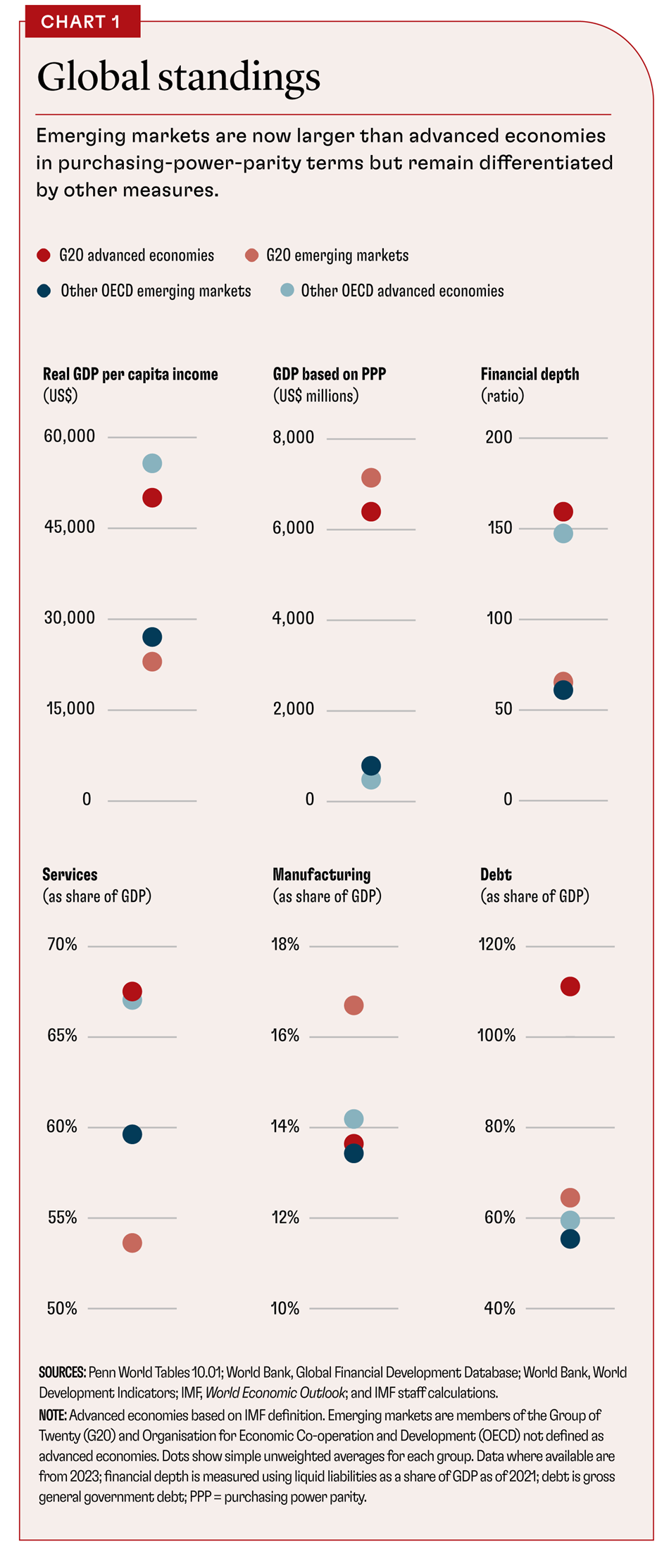

Having grown in both size and global economic stature—on the back of greater integration and hard-won reforms—emerging markets are not only a permanent fixture on the global economic stage but also expected to be natural champions of the multilateral approach.

Given their expanded global footprint, it might seem unusual that the concept of “emerging markets” is still in use. Until 1980, the IMF divided economies into two groups: a small clutch of “grown-up” wealthy, capital-rich “industrial countries” and a majority of “still-growing” poorer, labor-rich “developing countries.” In 1981, an enterprising employee at the International Finance Corporation, Antoine van Agtmael, devised the term “emerging market” to drum up interest in a new equity fund of 10 up-and-coming developing economies.

This label—evoking dynamism, potential, and promise—stuck. And it spawned a distinct asset class and numerous indices—such as the MSCI Emerging Markets Equity Index, introduced in 1988, and JP Morgan’s Emerging Markets Bond Index, created in 1991. These socialized investors to the new middle children of the global economy as they navigated growing pains and external shocks and faced currency crises, financial contagion, sudden stops, and growth accelerations.

However, many emerging markets are outgrowing both the term and the stereotype, given their global influence and greater policy credibility and sophistication. This raises questions: What does it take for markets to have finally emerged? And does it have any bearing on their place in the global economy?

Greater global sway

Perceptions of emerging markets are inevitably anchored in their economic and political origin stories, which are not only relatively turbulent but also more recent. Following the turmoil of the 1970s and 1980s, China’s accession to the World Trade Organization in 2001 ushered in a period of remarkable growth for emerging markets, until the global financial crisis. China’s development accelerated globalization and unleashed a commodity supercycle, which lifted global activity and enriched commodity-exporting emerging markets.

The tables turned after 2010 for emerging markets—notably commodity exporters. In China alone, annual GDP growth slowed by 4.6 percentage points between 2010 and 2019 and is expected to decelerate to just over 3 percent by 2029. Add to this the global fallout from the pandemic, fresh conflicts, commodity price shocks, the retrenchment of global capital, and escalating geopolitical tensions.

However, emerging markets are not the unwilling hostages to global developments they once were. On the contrary, recent IMF research highlights how emerging markets now are increasingly influential both locally and globally. Growth spillovers from domestic shocks in these economies have not only increased over the past two decades but are now comparable to those from advanced economies.

As a result, emerging markets are very much in the driver’s seat when it comes to global growth—both the highs and the lows. The performance of emerging market members of the Group of Twenty (G20) accounted for almost two-thirds of global growth last year. Fading prospects for these same economies have also driven more than half of the almost 2 percentage point decline in medium-term growth prospects since the global financial crisis. This weight will likely only increase.

Furthermore, despite China’s continued global economic heft, emerging markets are increasingly less reliant on its prospects. Their recent resilience can also be traced to an overall improvement in fundamentals—for instance, improved current account balances, lower dollar-denominated debt, and higher reserves—and better monetary and fiscal policy frameworks. And with the climate transition highlighting the gap between demand and supply for critical minerals such as copper and nickel, trade fragmentation and postpandemic diversification mean that the importance of emerging markets in global supply chains is set to grow.

Converging to advanced

Despite their expanding global influence and the increases in incomes and wealth they have secured for their populations, graduation to the “A(dvanced)-list” has remained elusive for all but a handful of emerging markets. To be an emerging market is to be left waiting with no clear end to the (emergence) process and somewhat overlooked on the global stage.

The IMF added “advanced economy” to its lexicon in the May 1997 World Economic Outlook. It grouped the four newly industrialized economies in East Asia and Israel with the existing 23 “industrial countries” of the time, based loosely on comparable per capita income levels, well-developed financial markets, a high degree of financial intermediation, diversified economic structures with relatively large and rapidly growing service sectors, and a declining share of employment in manufacturing. Since then, only 13 more economies have joined their ranks—all from Europe, except for Macao SAR and Puerto Rico—while the group as a whole has seen its share of global activity decline from 75 percent to 60 percent.

How did these countries make it? Two paradigms emerge. The first is that of the “Asian Tigers,” which pursued rapid export-oriented industrialization—as in Japan—through state intervention to develop comparative advantages in certain sectors (such as textiles in Hong Kong SAR and heavy and chemical industries in Korea). The second is the central and eastern European example of broad institutional reforms anchored by accession to the European Union and foreign capital inflows. In that setting, the extra step of joining the euro area by meeting the four economic convergence criteria also guaranteed an automatic invite to the A-list.

And here’s the problem (in both cases): to have emerged is to have converged. To do so—even by building comparative advantage in just one link of global value chains—requires large amounts of capital either from domestic or foreign savings, underpinned by a coherent policy framework that can survive the political cycle. In theory, emerging market and developing economies should be a magnet for external flows, as their smaller capital bases and strong growth potential translate into attractive real returns. In practice, we have the so-called Lucas paradox, the observation that capital does not flow from rich to poor countries. Instead, convergence requires funding domestically, unless there are Marshall Plan–scale capital injections at hand. As the latter are not so easy to come by, many emerging market and developing economies are at the mercy of fickle international capital flows amid weak governance and underdeveloped financial systems.

Multilateral mantle

But even if emerging markets still fall short of advanced economy standards, carving up economies into these two categories seems increasingly irrelevant in recent years. The growing depth of emerging markets’ integration into the global economy and their sheer size—both in terms of GDP and population—and diversity mean they are now just as significant and just as systemic as most advanced economies. That several advanced economies are reverting to inward-looking policies reinforces this prerogative: emerging markets are no longer bystanders but have a vested interest in the success of the multilateral approach. After all, globalization, cooperation, and the uninterrupted flow of goods, services, capital, and know-how have been—and will remain—instrumental to their growth, productivity, innovation, and poverty reduction.

Of course, some of the largest emerging markets have already been exercising their global economic rights as part of the G20—the only capital G group of countries indifferent to the emerging-advanced dichotomy. With 7 of the 10 recent presidencies held by emerging markets—with South Africa set to take up the torch in 2025—they have been able to promote issues they see as domestic and global macro-critical priorities: for example, inclusivity and investment (Türkiye 2015); innovation and technology diffusion (China 2016); the future of work, infrastructure, and sustainable food (Argentina 2018); female and youth empowerment (Saudi Arabia 2020); productivity and resilience (Indonesia 2022); green development and digital public infrastructure (India 2023); and inequality, revenue mobilization, and global governance (Brazil 2024).

However, just as emerging markets are stepping up, so too must international organizations engage further with them in the global interest. The IMF, for instance, must continue to tailor policy advice to country-specific circumstances. This requires even greater understanding of emerging markets and stronger expertise in their issues. The IMF must also review its resources and lending facilities—active and precautionary, financial and nonfinancial—to ensure an adequately funded global financial safety net and a suite of fit-for-purpose tools for systemically important emerging markets. And their growing importance should be legitimized in global governance.

Despite the label, emerging markets are now at the heart of global policymaking and global growth. At a time of growing uncertainty over the global economic environment and increasingly selective policies, international organizations can lean more heavily on these natural allies, which have a growing stake in keeping the flame of multilateralism lit, to overcome the immense global challenges we face.

AQIB ASLAM is a division chief in the IMF’s Research Department.

PETYA KOEVA BROOKS is a deputy director in the IMF’s Research Department.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.