Currencies and sectors

So what was the currency and sector composition of emerging market debt at

the end of 2019, just before the pandemic? While portfolio debt, composed

of emerging market government and corporate borrowing in bonds, constitutes

a significant portion of their external debt, cross-border bank loans are

equally important. Yet these loans are not included under portfolio flows.

In emerging markets, a disproportionate share of external liabilities (65

percent) is in portfolio debt (bonds) and other investment debt (loans), in

about equal amounts. Portfolio equity and foreign direct investment

constitute the remaining 35 percent. Sovereigns account for over 60 percent

of the portfolio debt, whereas banks and corporate loans together account

for 80 percent of other investment debt (Avdjiev and others 2020). Although

sovereigns can borrow externally via local currency bonds, most

cross-border bank and corporate bonds and loans are in US dollars.

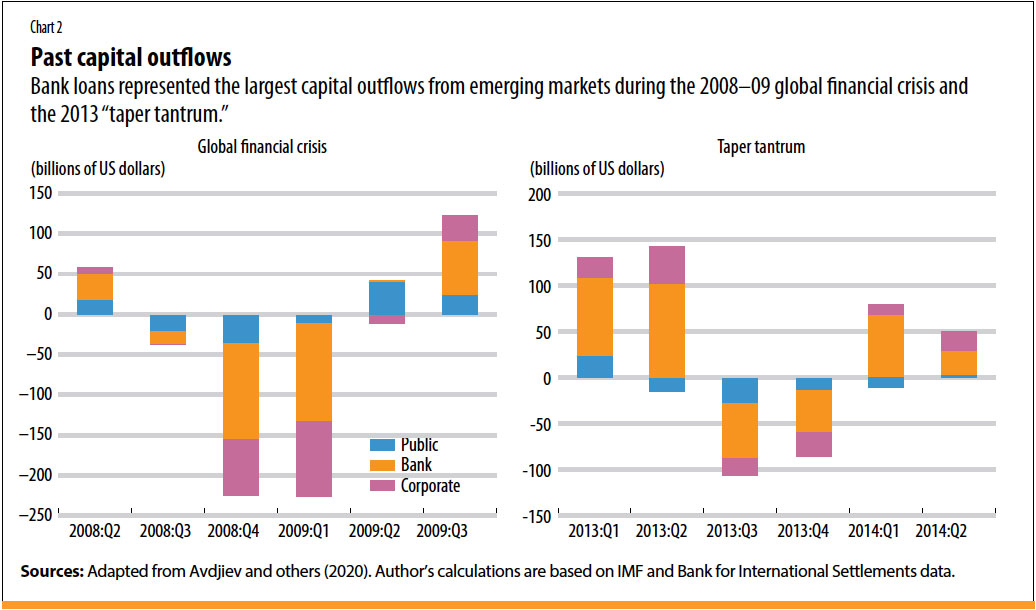

It is important to know which borrowing sector and what type of asset class

lost the most foreign capital during previous emerging market crises, such

as the 2008 global financial crisis and the 2013 “taper tantrum,” when US

Treasury yields surged on speculation that the Federal Reserve would slow,

or “taper,” its purchases of financial assets to boost the economy. During

those episodes, the largest capital outflows from emerging markets were

cross-border bank loans, followed by cross-border corporate loans and

corporate bonds, as shown in Chart 2.

The 2008 and 2013 episodes show that what we witnessed in terms of capital

outflows from emerging markets at the beginning of the pandemic in

March–May 2020 actually could have been worse. During the financial crisis

and taper tantrum episodes, outflows focusing on total debt of the private

sector—as opposed to portfolio debt alone—were understandably much larger

than the $30 billion in portfolio debt outflows early on in the pandemic.

As for the $70 billion that left portfolio equity, this was not surprising

since this is the riskiest emerging market asset class and COVID-19 was the

biggest shock since the global financial crisis in terms of investor flight

from risk.

Banking and corporate debt flows for emerging markets stayed intact in

2020, unlike during the global financial crisis and the taper tantrum,

thanks to fast, clear, and unprecedented action by the Federal Reserve. US

monetary policy is the key determinant of emerging market private sector

flows, which are in dollars and borrowed from private creditors, and

sensitive to the risk appetite of global investors.