Sweden Concluding Statement for the 2019 Article IV Consultation

February 21, 2019

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF's Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

Macroeconomic policies must continue to support Sweden’s economic resilience. Growth is expected to slow in 2019, with material downside risks from the global economy and domestic demand. Monetary policy should defer further rate hikes until the economic outlook is consistent with durably meeting the inflation target. Automatic fiscal stabilizers should operate fully to cushion lower growth. Reducing the fiscal surplus to its medium-term target by 2020 would provide a small stimulus while protecting buffers.

Timely structural reforms to sustain strong and inclusive growth would also reinforce confidence. Labor market reforms should aim to support employment of the low‑skilled and migrants, aided by enhanced education and training. Comprehensive housing market reforms, especially of rent controls, tax policies, and construction regulation, are essential to lower barriers to labor mobility and growth and to contain inequality.

Financial sector risks should continue to be monitored closely. The macroprudential stance is appropriate following the adoption of stricter amortization requirements. Any anti-money laundering issues in domestic institutions must be addressed and regional cooperation should be strengthened. Household level balance sheet data should be collected to enhance risk monitoring and the design and evaluation of measures. In the innovative e-krona project, the authorities should also explore regulatory options to ensure reliable and efficient private payments.

Monetary Policy

Accommodative monetary policy supported strong domestic demand gains that drove solid economic growth in 2016-18. Job creation was particularly rapid, reducing unemployment to 6.2 percent by the end of 2018, although wage rises have increased only modestly. CPIF inflation of just over 2 percent during 2018 was partly driven by energy prices, with CPIF inflation excluding energy running at 1.5 percent in 2018’Q4.

But an economic slow-down appears to be underway owing to falling dwelling investment, softening consumption linked to a correction in housing market sentiment, and weaker global growth impacting exports. Growth is expected to decline to 1.2 percent in 2019, before rebounding to around 2 percent in later years. Aided by some depreciation of the krona, CPIF inflation excluding energy is expected to rise to 1.7 percent by end 2019 and to gradually converge to target thereafter, benefiting from a further pickup in wage rises.

This outlook for Swedish growth and inflation is subject to additional uncertainty given the downside risks to global growth from factors such as potential trade disruptions, together with domestic uncertainties including the path of dwelling investment. A patient and data‑dependent monetary policy is appropriate in these circumstances, consistent with the Riksbank’s deferral of further rate increases until the second half of 2019, depending on whether the economic outlook and inflation prospects are as it expects.

The parliamentary review of the Riksbank law is undertaking important analysis of Sweden’s current monetary and financial stability arrangements. As recommended by the IMF’s FSAP in 2016, the Riksbank’s financial stability role should be put on a firmer legal footing, by providing explicit mandates for it to monitor systemic financial risks and to provide emergency liquidity to banks. It will also be important to protect the Riksbank’s financial autonomy, such as in relation to capital and dividends.

Fiscal Policy

Sweden has strong fiscal buffers, with gross debt of 38 percent of GDP, net debt among the lowest of advanced economies, and a surplus of about 0.8 percent of GDP in 2018. Its relatively strong automatic fiscal stabilizers should therefore operate fully to cushion the economy and jobs against swings in growth, including in 2019.

A new medium-term target for the fiscal surplus of 0.33 percent of GDP became effective this year. Reducing the cyclically-adjusted surplus to this target by 2020 would release a modest 0.2 percent of GDP in resources to facilitate reforms to bolster inclusive growth. The resulting fiscal stimulus in 2019-20 would be small, with low risk of overheating at a time of slowing growth and still low inflation, and fiscal buffers would remain strong.

Sweden will likely raise public investment in coming years, as it faces demographic shifts that require more schools, healthcare, and housing facilities. Major infrastructure investments such as new railway lines are also being considered. If these factors raise public investment beyond past norms, a temporary cut in the medium-term surplus target should be considered to avoid adjustments in taxation or other spending.

Labor Market

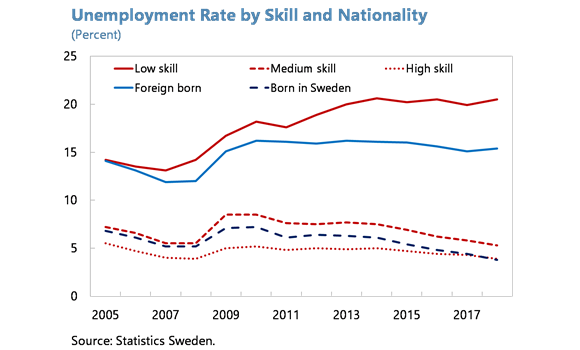

Employment of the foreign born has increased substantially in recent years, yet the unemployment rate of the foreign born still greatly exceeds that of natives. The social partners’ plan for “entry agreements” to enable migrants and the low‑skilled to combine work and training at reduced cost to employers will help to address these challenges.

It is also important that the “January agreement” that was made when forming the new government includes steps to strengthen the integration of migrants together with measures to enhance education and training. When reviewing employment protection arrangements, the social partners should seek to facilitate labor market entry by the low‑skilled and migrants, such as by further extending trial periods, in addition to increasing flexibility for small- and medium-sized enterprises. Reforms of the Public Employment Service need to be carefully designed and monitored to improve job matching and work skills development, especially for migrants and the low-skilled.

Swedish wage rises tend to follow those in Germany. This pattern reflects the leadership of wage rises agreed by the industrial sector for wages negotiated in other sectors under the Industrial Agreement of 1997. In recent years, the resulting wage rises have been subdued relative to the tightness of domestic labor markets, contributing to low inflation, thereby prolonging low interest rates and a weak krona.

The social partners should consider updating wage formation to reflect structural changes in the Swedish economy, including the rise of other sectors such as services. One option is to broaden the range of sectors that set the benchmark for wage rises, which would likely tighten linkages to domestic economic trends such as inflation expectations and productivity, enhancing Swedish macroeconomic stability. Moreover, to increase flexibility to adapt to shifting labor demand, including demographic change, the mandate of the National Mediation Office should drop adherence to the industrial sector wage benchmark, to enable a greater focus on its goals for real wage growth, higher employment, reducing labor market conflicts, and facilitating changes in relative pay.

Housing Market

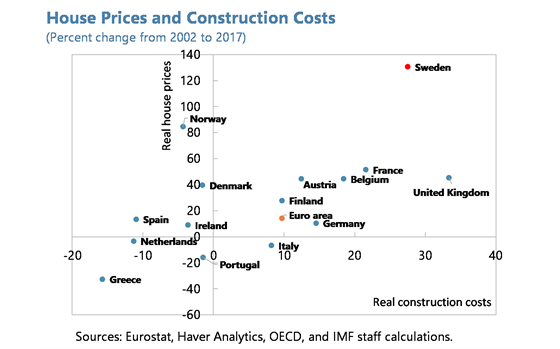

After rising substantially for many years, Swedish housing prices declined by 6 percent in late 2017, and have since stabilized with a rise of 2 percent in 2018. This mild decline reflected a surge in apartment completions concentrated at the luxury end of the market. However, housing starts have fallen sharply, by 16 percent in 2018, partly due to lower prices, but also because the pre-sale financing that some property developers relied upon has become much less available as it is considered too risky by households.

A notable fall in dwelling investment is therefore expected in 2019, despite housing prices remaining high relative to household income in the main centers where housing shortages are most evident. In these areas, long queues for rent-controlled apartments force households to either purchase apartments that are among the most expensive worldwide, incurring high debts, or to pay substantially higher rents for other apartments. These barriers to labor mobility weigh on Swedish productivity and incomes, and raise inequality across regions and between generations.

The “January agreement” includes promising steps to tackle Sweden’s dysfunctional housing market. But more fundamental reforms should be sought given the scale of the problem, while recognizing that change will take time and that measures to smooth the adjustment will be needed. Key elements of a reform package would include:

- Making the rental market work: in addition to fully liberalizing rents of newly constructed apartments, there is a need to phase out existing controls. A common approach is to apply market rents when there is a change in tenant. Access to the housing allowance could be expanded to cushion this adjustment, while also applying a temporary “windfall” tax on significant rental income gains. To help reduce market rents more quickly, rental supply should be increased, such as by reducing impediments to sub-letting and to households renting out their own apartments, while containing potential macrofinancial risks.

- Taxing property to rebalance the housing market: Sweden’s property tax was capped in 2008 to be among the lowest in the OECD, limiting the cost to households of occupying housing beyond their needs. A broad-based increase in the ceiling on the property tax would be most efficient, but an increase targeted to the main centers could be considered to incentivize mobility where it is most needed. Abolishing the interest on deferrals of capital gains taxes will help ease deterrents to mobility. An additional step to be considered is to tax only a portion of the capital gains on primary dwellings. Implementing a phase out of mortgage interest deductibility—which boosts housing demand and prices—would have limited impact on household finances currently given the low level of interest rates.

- Producing housing that is affordable : it is important to simplify the planning process to reduce the overall costs of construction. Productivity in the construction sector should be enhanced by strengthening competition, including by harmonizing land sale procedures across the municipalities and preventing requirements beyond the national building standards in the approvals process. The government should also expand existing subsidies for construction of affordable rental apartments, together with those for student and elder housing in view of changing demographics.

Financial Sector

The expansion of Finansinspektionen’s (FI) macroprudential mandate from February 2018 addresses a key recommendation from the IMF’s FSAP for Sweden in 2016. Subsequent macroprudential measures have been well targeted: the stricter amortization requirement effective from March 2018 contains vulnerabilities from high loan-to-income (LTI) mortgages; while the 0.5 percentage point increase in the countercyclical capital buffer from September 2019 helps address broader increases in bank risk-taking.

The macroprudential stance is appropriate, yet risks should remain under close watch. Housing prices are now estimated to be more in line with longer run fundamentals and mortgage lending growth has declined, especially the share of high LTI mortgages. But vulnerabilities persist such as potential spillovers from financing difficulties among smaller property developers. Collecting household level balance sheet data remains essential to monitoring macrofinancial risks and for designing and evaluating measures.

Concerns about the effectiveness of anti-money laundering and counter-terrorist financing (AML/CFT) frameworks have become prominent in the Nordic-Baltic region. The Swedish AML/CFT framework has been strengthened in recent years, including through new legislation in 2017. FI has allocated additional resources to AML/CFT supervision and is currently monitoring the situation in domestic institutions. The authorities should identify and address any issues in Swedish institutions and continue to work to correct any remaining deficiencies in Sweden’s AML/CFT framework. Given the highly integrated financial sector in the region, strong cooperation and frameworks are key to the effectiveness of the AML/CFT regime.

Nonbanks have begun to enter the mortgage market, helping to sharpen mortgage loan pricing. It is important that these lenders meet the same consumer protection and macroprudential requirements, while ensuring that compliance costs are manageable. Commercial property valuations appear to be stretched by historical standards, and FI should continue to review the adequacy of banks’ risk management and the health of commercial property borrowers. Following the default of a clearing member in Nasdaq Clearing, the FI should assess measures to contain risks and improve the efficiency of default management procedures.

“Cash-free” transactions are more prevalent as digital payments take over, potentially leaving no alternative to private payment services. The Riksbank’s innovative e-krona project is garnering global attention and has made progress with analyzing potential demand and the implications for financial stability. In the ongoing work, the authorities should also explore regulatory options to ensure reliable and efficient private payments.

The mission appreciates the candid and insightful discussions with the Swedish authorities and other counterparts.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: Andreas Adriano

Phone: +1 202 623-7100Email: MEDIA@IMF.org