Capital flows to emerging market and developing economies went through several boom-bust cycles in recent decades, often partly driven by external developments such as monetary policy decisions in major advanced economies. During the recent global monetary tightening, inflows to many emerging market and developing countries proved relatively resilient, benefitting from robust policy frameworks and healthy international reserves. However, some of the most vulnerable countries were disproportionately affected by higher external borrowing costs, as illustrated by a sharp slowdown in Eurobond issuance.

Eurobonds are international debt instruments issued by countries in a currency different from their own, typically the US dollar or the euro. Eurobonds are primarily used by higher risk emerging market and developing countries because they avoid the limitations of their often less-developed domestic capital markets, allowing borrowers to access foreign capital and diversify their funding sources. But unlike local currency bonds, Eurobonds involve exchange rate risk for the borrower, and their interest rates are particularly sensitive to monetary policy settings for the currency of issuance.

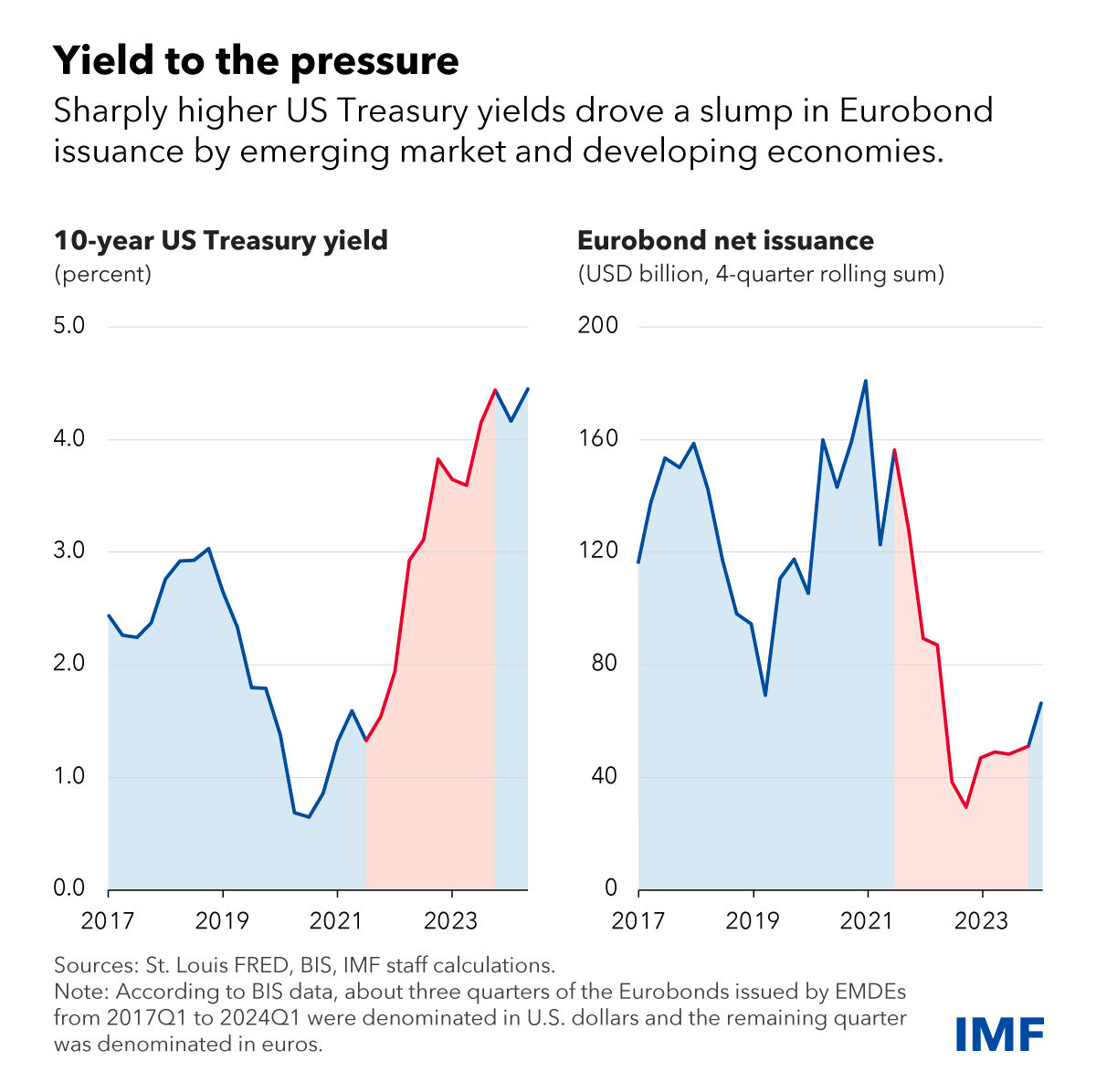

The Chart of the Week highlights the sharp slowdown of Eurobond net issuance by emerging market and developing economies, which fell to an annual $40 billion in 2022-23, down 70 percent relative to the prior two years. During this period, 26 of 75 countries saw net Eurobond outflows, totaling $58 billion (including countries like Bolivia and Mongolia). These outflows resulted from maturing Eurobonds exceeding new issuance, rather than outright sales by global investors.

The reduction in Eurobond flows reflected a combination of tightening external financial conditions and pre-existing vulnerabilities in affected economies, such as fiscal and external sustainability challenges. Some countries with more robust fundamentals and policy frameworks were able to substitute foreign currency issuance with local currency debt, funded in part by domestic investors. Many countries responded by cutting investment to reduce imports, weighing on economic growth. Many countries also drew on their reserve buffers, which could reduce their ability to withstand future shocks.

Net Eurobond issuance has a strong negative association with advanced economy interest rates, approximated by the 10-year US Treasury yield. When bond yields in the United States and other advanced economies slumped during the pandemic, borrowers in emerging market and developing economies took advantage of cheap borrowing costs to issue debt.

During the subsequent tightening of monetary policy by the Federal Reserve and other major central banks, Eurobond inflows in many lower-rated emerging market and developing countries dried up as borrowing rates reached prohibitive levels. Eurobond issuance diminished even as the interest rate differential widened in favor of emerging market and developing economies, pointing to the importance of external interest rates for this type of capital flows.

This year, global interest rate conditions have started to become more favorable for borrowers, as central banks in several major advanced economies moved toward easing monetary policy. This supported a recovery in Eurobond issuance to $40 billion in the first quarter of 2024 as countries such as Benin and Côte d’Ivoire returned to the market. The onset of a Fed easing cycle may support an additional rebound in Eurobond issuance and a broader revival of capital flows to emerging market and developing economies.