Our recent research (Dao and others, forthcoming) covering 21 advanced and emerging market economies sheds light on these competing explanations by decomposing headline consumer price inflation into underlying (core) inflation and headline shocks—deviations of headline from core inflation. We explain core inflation by long-term inflation expectations and broad measures of macroeconomic slack, such as the unemployment rate, the output gap, or the ratio of vacancies to unemployment. We explain headline inflation shocks by large price changes in particular industries, such as food, energy, or shipping, and by measures of supply-chain disruptions. We also allow for the pass-through over time from these industry price shocks to core inflation, which can occur through the effects of headline inflation on wages and other production costs.

Putting the different pieces together, we estimate the respective contributions of headline shocks, their pass-through into core inflation, broader measures of macroeconomic slack, and changes in long-term expectations to the rise and fall of inflation across countries.

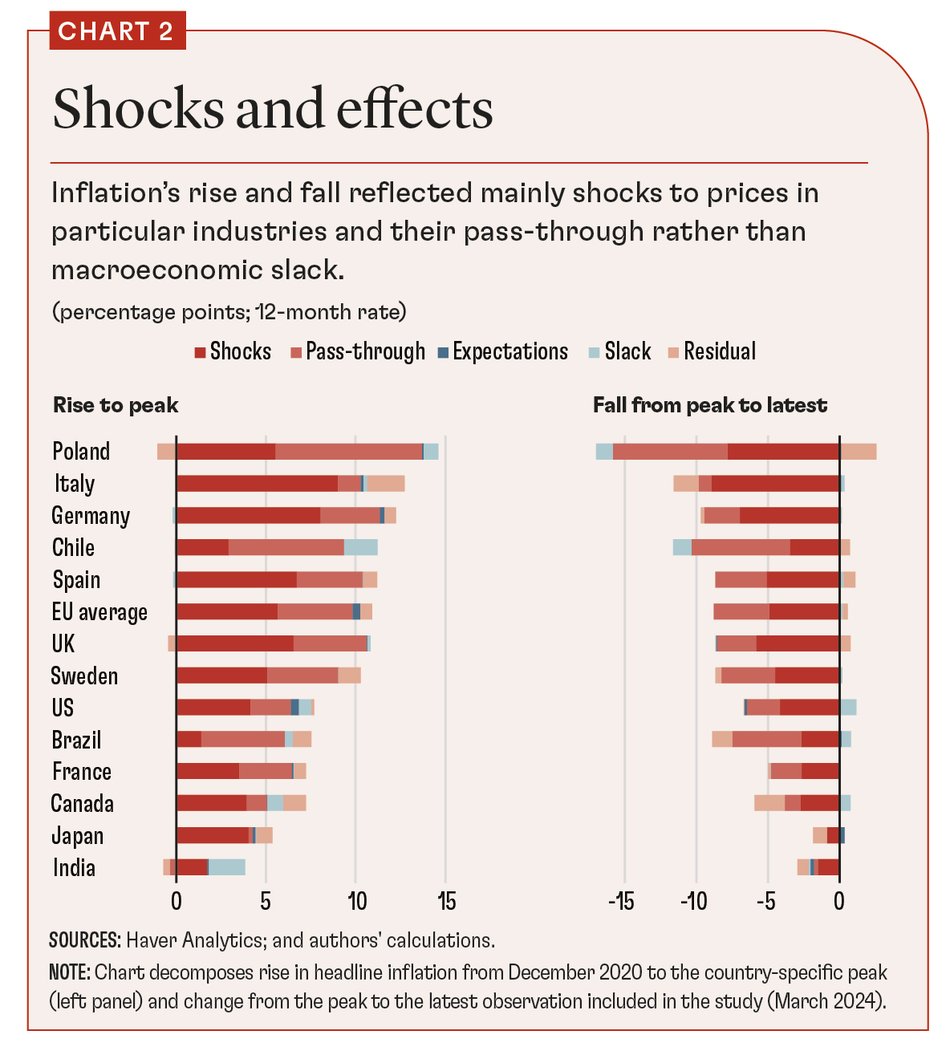

Overall, we find that headline shocks and their pass-through into core inflation account for most of the rise and fall of inflation. Broader measures of macroeconomic slack and changes in longer-term inflation expectations generally contribute little (see Chart 2).

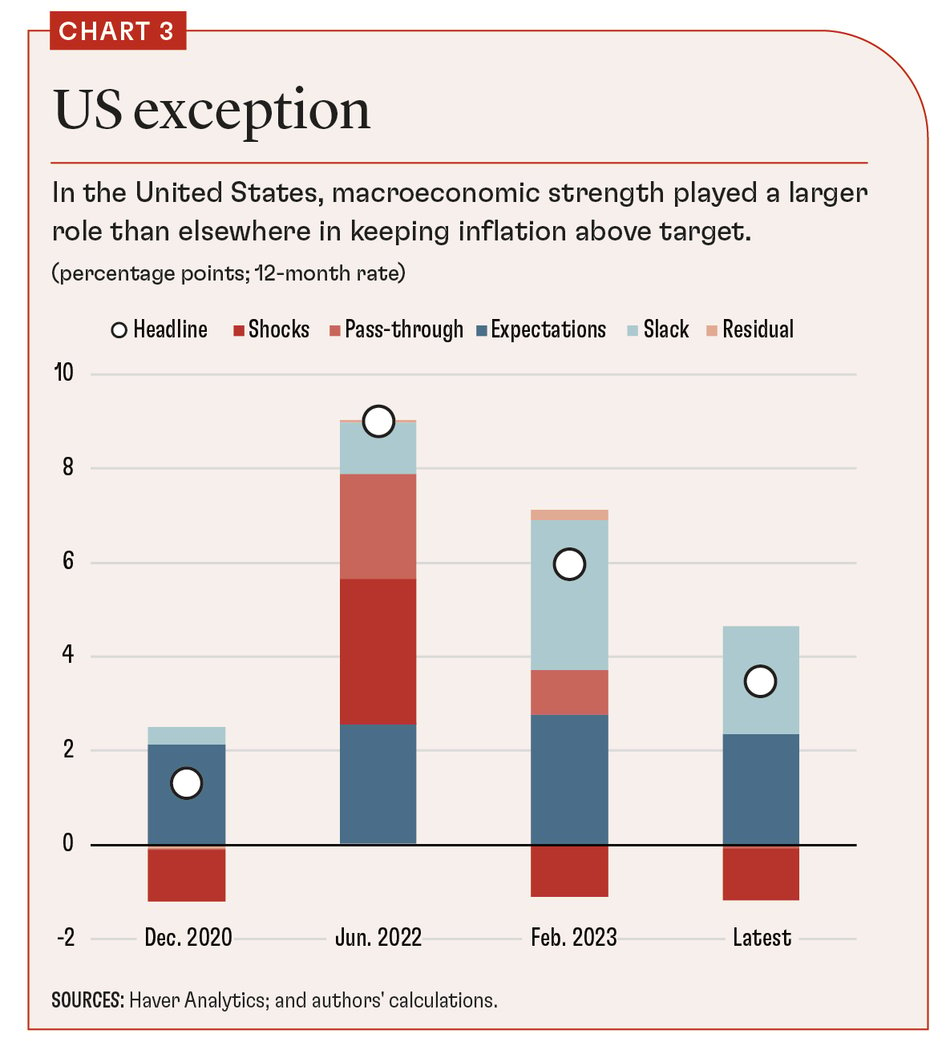

The United States is a significant exception. The contribution of broad macroeconomic tightness to inflation remains greater than in other economies despite the significant cooling of the labor market since early 2023. The fall in US headline inflation since February 2023 reflects equally the cooling of the broader economy and the fading pass-through from earlier headline shocks (see Chart 3).

The bottom line is that inflation’s rise and fall reflected primarily global drivers, but local circumstances mattered too. We find, for example, that differences in local energy price policies, including subsidies for people and businesses, explain differences in the role of energy price shocks in driving inflation. France, for instance, had large price-suppressing fiscal measures and a relatively small contribution of energy to headline inflation shocks.

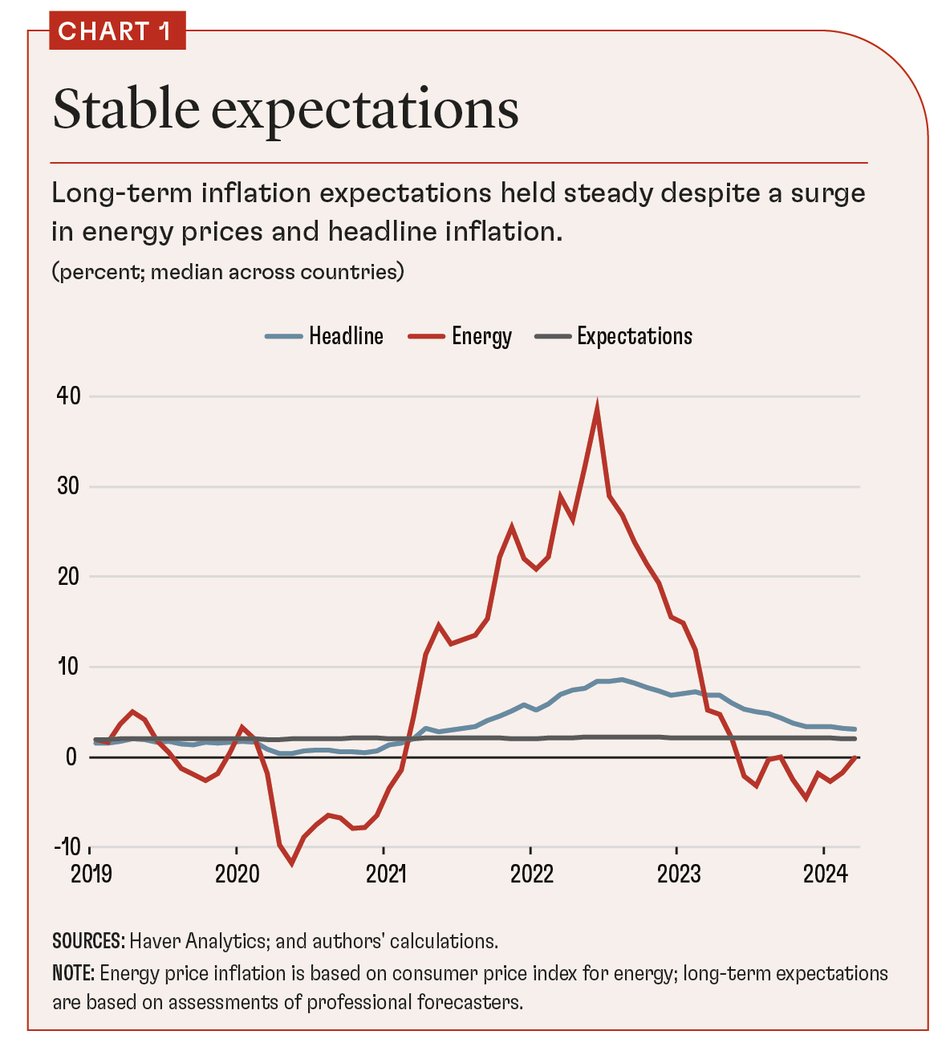

Monetary policy also played a critical role in defeating inflation. Throughout this period, long-term inflation expectations remained well anchored. This suggests that central banks retained credibility and that this helped prevent wage-price spirals. Global tightening of monetary policy may also have helped bring down global demand and hence energy prices. At the same time, energy shocks and their pass-through, as well as their reversal, account for the bulk of the rise and fall of inflation, without the need for a deep economic slowdown. Even so, in the case of the United States, strong macroeconomic conditions have been a more important contributor to core inflation than in other countries. Since March 2024, when our sample ends, US labor market conditions have further moderated, and this should help inflation return to target.