China’s Service Sector Is an Underutilized Driver of Economic Growth

August 2, 2024

Reforms to rebalance demand toward consumption and further open the service sector can promote sustainable growth and help create jobs

China’s economic development over the last several decades has been remarkable amid rapid growth. We project growth will remain resilient at around 5 percent in 2024, despite the continued property sector adjustment.

At the same time, China has relied too much on investment as opposed to consumption. Diminishing productivity and an aging population risk restricting growth, which we expect to slow significantly in coming years, to around 3.3 percent in 2029. Addressing these challenges requires a comprehensive and balanced policy approach.

Given these circumstances, the country’s service sector is an underexploited driver of growth—which was also recognized at the Third Plenum. Reallocating resources to services has helped boost productivity over the past two decades. And it can continue doing so in the years ahead if supportive reforms are implemented.

Expanding the service sector can also help put more people to work—especially young people, who are disproportionately employed in service sectors like technology and education. Moreover, since emissions are lower in services, expanding the sector would help China reach its climate goals more efficiently.

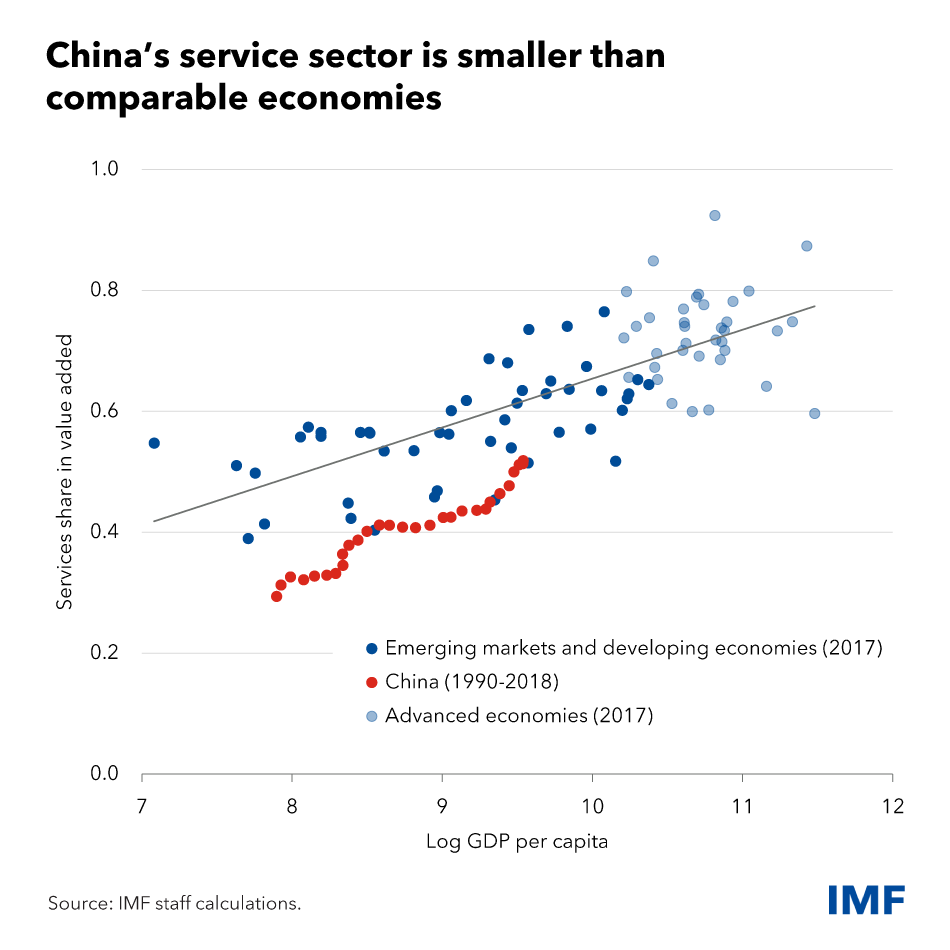

China does have significant further potential for expanding services, as we show in our latest annual review of the world’s second-largest economy. While the sector’s share of value-added to the economy has increased in recent years to just over 50 percent, it is still well below the average of about 75 percent for advanced economies.

Even though service sector firms have been highly innovative in China, company-level data indicate that the allocation of capital and labor across firms has been increasingly less efficient in the sector. This means that highly productive firms have been too small on average, suggesting difficulties attracting new capital and labor, while less productive firms were cornering too large a share of the market.

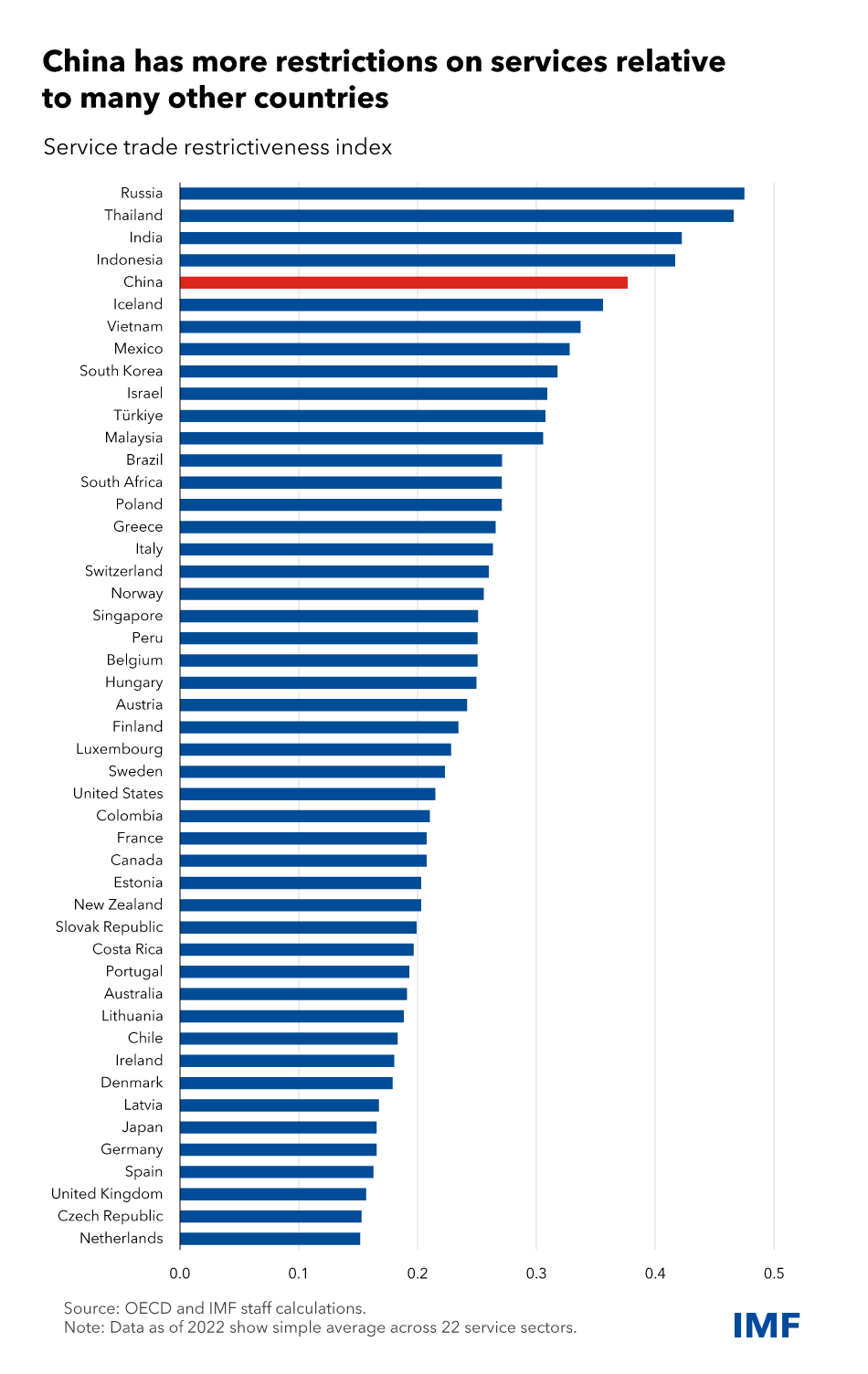

China should therefore prioritize reforms to improve the allocation of capital and labor in services. The sector remains subject to more onerous regulations compared with members of the Organisation for Economic Co-operation and Development, including restrictions on domestic and foreign entry as well as significant regulatory hurdles. Easing regulatory requirements, further reducing local protectionism, and allowing more businesses to enter and compete in services—including reduced trade and foreign entry restrictions—can boost productivity and support growth.

China should also prioritize rebalancing the economy to strengthen demand for services. Improving social safety nets and making taxes more progressive would reduce the need for precautionary savings, especially by middle- and lower-income households, and allow greater spending on services. Increased coverage and better unemployment and medical benefits would further boost consumption. In this context, this year’s increase in old-age benefits by 19 percent for rural and non-working urban residents is a small but welcome step.

Overall, the service sector can create jobs and drive sustainable growth in China. Ideally, policies to help rebalance demand toward consumption would be combined with reforms that lower barriers to entry and ease other regulatory restrictions that have prevented capital and labor from being efficiently allocated in the past. We estimate that a comprehensive package of market-based structural reforms, enhancements to the social safety net, and pension reforms can raise the GDP by close to 20 percent over the next 15 years relative to the baseline, or about 1 percentage point higher potential growth per year over the medium term.

****

Sonali Jain-Chandra is the IMF mission chief for China. Siddharth Kothari and Natalija Novta are senior economists for China in the Asia and Pacific Department.