Motorcyclist buys fuel in Malaysia. Lower oil prices offer an opportunity to lower energy subsidies, say IMF economists (photo: Zainal Abd Halim/Corbis)

ECONOMIC HEALTH CHECK

Growth will be driven by domestic demand, underpinned by healthy labor markets, low interest rates, and the recent fall in oil prices. The global recovery, while moderate and uneven, will continue to support Asia’s exports, say the report’s authors.

Regional mix

Performance across the region is expected to be mixed (see table). China’s economy is slowing to a more sustainable pace—6.8 percent GDP growth in 2015, and 6.3 percent in 2016, while growth in Japan is picking up to 1.0 percent this year, and 1.2 percent next year.

India’s growth rate is expected to rise to 7.5 percent this year and next, making it one of the fastest growing economies in the world. Within the Association of Southeast Asian Nations (ASEAN), while Malaysia is expected to slow, the Philippines should see growth increase. Overall, lower commodity prices are a net positive for Asia, although several commodity exporters (Australia, Indonesia, Malaysia, and New Zealand) will be adversely impacted.

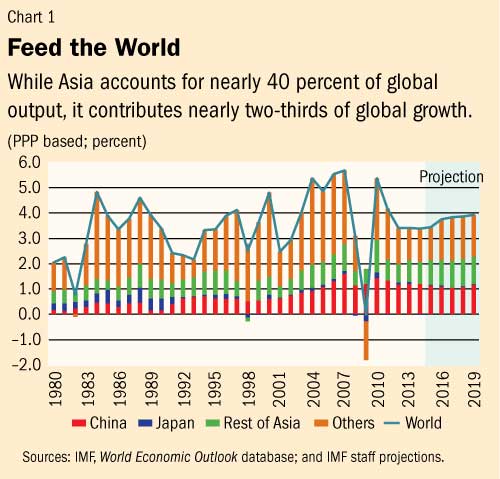

Asia will remain the global growth leader, even though potential growth—the economy’s speed limit—is likely to slow (Chart 1). While Asia accounts for nearly 40 percent of global output, it contributes nearly two-thirds of global growth. Asia’s leading role in world growth is set to continue over the medium term despite slowing potential growth, which reflects weaker productivity gains, the effects of aging, and infrastructure bottlenecks.

Risks tilted to the downside

The outlook could be vulnerable to adverse events, says the report. This reflects the potential for slower-than-currently-expected growth in China and Japan, which could spill over to the rest of the region—and the global economy—through trade and financial channels.

Debt levels—including foreign currency-denominated debt—have increased rapidly in recent years, and Asia is now more vulnerable to financial market shocks, and persistent U.S. dollar strength, which would raise the cost of servicing debt, and could curtail demand.

The large swings in the value of the major reserve currencies could create an uncomfortable trade-off between financial stability and competitiveness. On the other hand, lower energy prices could provide a further boost to Asia’s growth if more of the savings on oil import bills is spent.

Policies to boost resilience and growth

Most Asian policymakers have in place broadly appropriate interest rate and fiscal policy settings, although the risk of renewed financial volatility may warrant a somewhat tighter monetary policy stance in some countries. Maintaining flexible fiscal and monetary policies to effectively manage aggregate demand will remain important in the future, say the report’s authors.

The authors observed that lower oil prices have provided an opportunity to undertake further fiscal reforms aimed at lowering energy subsidies, and measures have been taken in a number of countries, including Malaysia, India, and Indonesia.

Financial and macroprudential policies should continue to address financial sector risks. This will be particularly important to increase resilience to shocks, and to contain the buildup of systemic risk associated with shifting financial conditions, and volatile capital flows.

As global financial conditions adjust to diverging monetary policies in advanced economies, flexible exchange rates should remain a shock absorber. While exchange rates should also be allowed to adjust to balance of payments flows, foreign exchange intervention should remain in the toolkit to address disorderly market conditions.

The IMF’s Regional Economic Outlook calls for a strong push for structural reforms across most, if not all, economies in the region. The report notes that in addition to boosting productive capacity, structural reforms can help rebalance growth toward consumption, which remains a priority for some major Asian economies, including China and Korea.

In economies where aggregate demand is relatively weaker such as Korea and Thailand, combining structural reforms with temporary macroeconomic stimulus would mitigate the risk of deflation. Critical areas include reforms to state-owned enterprises, and financial liberalization in China, initiatives to raise services productivity, and labor force participation in Japan, and measures to address supply-bottlenecks—including by expanding essential infrastructure, and deregulating key sectors—in India, ASEAN, frontier economies, and small states.

The role of trade and finance in Asia

The Regional Economic Outlook also discusses, in two background studies, the role of global value chains (GVCs) in trade, and intra-regional financial integration in Asia.

The expansion of GVCs has been pronounced in Asia, especially emerging Asia. In addition, emerging Asian economies have moved more upstream (i.e. providing intermediate inputs to other countries), rather than downstream (i.e.processing inputs from more upstream countries), and have captured a growing share of GVC-related value added.

The rise of GVCs has altered the responsiveness of trade volumes to exchange rate changes. Using a new measure that adjusts for participation in global value chains, the study suggests that both exports and imports in the global value chain react positively to a real depreciation, with upstreamness (downstreamness) tending to amplify (dampen) the impact.

Limited cross-border financial transactions

The financial integration study finds that around 20-30 percent of cross-border portfolio investment and bank claims are intraregional, much lower than the intra-regional trade share in total trade.

Home bias—the tendency to invest more in the home country rather than abroad—is particularly strong in Asia, thus limiting cross-border financial transactions within, and outside the region.

The analysis shows that financial integration increases with the size, and sophistication of financial systems and the extent of trade integration. But, restrictions on foreign asset holdings, barriers to foreign bank entry, and differences in regulatory and institutional quality hinder financial integration.

Promoting financial market development, and trade linkages, including through greater harmonization of regulation, will foster financial integration within the region, potentially enhancing the intermediation of Asia’s large saving pool.