Capacity Development

When government works well, people thrive. The IMF’s capacity development efforts enable governments to provide better services such as schools, roads, and hospitals. They foster a stable economic environment. And they help improve growth and create jobs.

The IMF serves as a global hub for knowledge on economic and financial issues. Over the past 50 years, it has established world-class expertise and built a repository of collective experience on which policies work, why they unleash growth, and how best to implement them. The IMF shares this knowledge with government institutions, such as finance ministries and central banks, through hands-on expert advice, peer-learning workshops, and policy-oriented training. This support is delivered to countries through expert advice delivered in-country and from headquarters, regional capacity development centers, and in-person and online training.

The IMF’s capacity development mission is an important complement to its surveillance and lending mandates. For instance, working with governments to improve their policies and processes helps increase the usefulness of IMF policy advice, keeps the institutions up to date on innovations, and helps address crisis-related challenges. At the same time, the IMF’s surveillance and lending work may help identify areas in which capacity development activities can have the biggest impact in a country.

The IMF’s capacity development efforts focus on the following areas:

- Fiscal policy: Advising governments on how to raise revenues and effectively manage expenditure, including tax and customs policies, budget formulation, public financial management, domestic and foreign debt, and social safety nets. This enables governments to provide better public services such as schools, roads, and hospitals.

- Monetary and financial sector policies: Working with central banks to modernize their monetary and exchange rate frameworks and with supervisory and regulatory authorities to enhance financial institutions’ oversight. This improves the countries’ financial stability, fueling domestic growth and international trade.

- Legal frameworks: Helping countries align their legal and governance frameworks to international standards so they can develop sound fiscal and financial reforms, fight corruption, and combat money laundering and terrorism financing.

- Statistics: Helping countries with the compilation, management, and reporting of their macroeconomic and financial statistics. This provides more accurate understanding of their economy and helps formulate more informed policies.

The Fund is preparing for the 2018 Quinquennial Review of the Fund’s Capacity Development Strategy. In February 2017, the Board provided feedback on the concept note for the review (see Box 2.1).

BOX 2.1 QUINQUENNIAL REVIEW OF THE IMF’S CAPACITY DEVELOPMENT STRATEGY

The IMF’s capacity development strategy was last discussed by the IMF Executive Board in June 2013. The discussion yielded the first integrated strategy for capacity development and concluded with several recommendations to update the capacity development governance structure, enhance prioritization, clarify the funding model, and strengthen monitoring and evaluation. Subsequently, the Board endorsed the 2014 statement on IMF Policies and Practices on Capacity Development.

Since 2013, significant progress has been achieved, particularly with respect to strengthening the capacity development governance and prioritization frameworks. Thus, the 2018 Quinquennial Review of IMF capacity development provides an opportune time to systematically review progress since then, identify remaining challenges, and lay out reform priorities in the period ahead. To this end—and as elaborated in the concept note, discussed by the Board in an informal session on February 24, 2017—the review will include backward- and forward-looking components:

- The backward-looking component will consider the prioritization, funding, monitoring and evaluation, and delivery of capacity development as set out in the 2014 statement.

- The forward-looking component will provide the opportunity to outline reforms to increase the impact of capacity development. Emphasis will be on making capacity development more effective and efficient while building on its existing strengths, including through (1) further strengthening the framework to ensure that it is targeted at the most important needs of countries as defined by both the country authorities and the IMF, (2) seeking innovative delivery methods, (3) sharing IMF knowledge in this area with the membership, (4) further integrating capacity development with IMF surveillance and policy advice, and (5) entrenching the results-oriented approach.

- The capacity development strategy review is planned to be discussed by the Board in May 2018. Conclusions from the 2018 review will be reflected in a revised statement on IMF policies and practices on capacity development.

![]()

Highlights: Fiscal Capacity Development

Revenue mobilization

Strengthening domestic revenue performance is a key objective of the 2030 Agenda for Sustainable Development and is included as one of the UN SDGs. Sound tax systems are an essential basis for strengthening revenues and achieving the SDGs. The IMF has long supported its member countries in building and modernizing their tax institutions and policies. In the past decade, it has provided ample technical assistance in tax policy and revenue administration. Many low-income developing countries have made significant progress in domestic revenue mobilization: tax-to-GDP ratio in low-income developing countries has on average risen by some 5 percentage points. This achievement, however, is not observed in all countries, and significant challenges remain.

Reflecting its commitment to the Addis Ababa Action Agenda of 2015, the IMF has significantly scaled up its work in this area and further developed external funding agreements with partners. The IMF launched the Revenue Mobilization Trust Fund (RMTF) in August 2016 as a successor to the successful Tax Policy and Administration Topical Trust Fund, doubling the resources available to assist lower-income countries in developing their tax capacity. The RMTF will help integrate new fiscal assessment tools (see Box 2.2); enable advice in the areas of global priority, such as international taxation and carbon taxes; and support the development of training activities needed to ensure sustainable progress. During the year, a new five-year phase of the Managing Natural Resource Wealth Trust Fund was also launched. This fund supports capacity building in countries with mining and petroleum activities to help them better manage these resources, including through tax design, collection, and macroeconomic management.

The IMF is working with member countries to achieve higher levels of revenue by integrating this priority more firmly into its surveillance function. In about two dozen countries where revenue mobilization is viewed as macro-critical, the IMF has provided additional policy advice in this area in the context of Article IV consultations. The IMF has also expanded its work on international tax policy in the context of surveillance, undertaking analysis and advice to assist a diverse set of its members in coping with tax avoidance strategies (that is, base erosion and profit shifting).

The IMF is also working on a new initiative on medium-term revenue strategies in partnership with the Organisation for Economic Co-operation and Development, World Bank, and United Nations that involves helping countries develop and implement comprehensive reform strategies that encompass tax policy, tax legislation, and tax administration.

Examples of the IMF’s revenue mobilization efforts include the following:

- After decades of civil war, Liberia in 2011 took on the challenge of reforming its tax code and establishing a modern revenue administration to help finance much-needed public services. In consultation with the IMF, the Liberian authorities developed an extensive reform program focused on improving the tax policy framework, establishing a robust organizational structure, strengthening core functions such as audit and taxpayer services, and building capacity through training and coaching.

These efforts helped lay the groundwork for the successful establishment of the Liberia Revenue Authority and set up systems to manage taxpayers in a more effective and risk-focused manner. Liberia’s tax-to-GDP ratio reached 19¼ percent in 2015, comparing well with its peers, and the revenue authority now plays a major role in supporting the government’s goal of becoming a middle-income country by 2030.

- In Mongolia, the IMF has worked with the authorities since 2010 to help strengthen its Large Taxpayer Office, which caters to some 400 companies that account for about 50 to 60 percent of total domestic revenue. The IMF organized a diagnostic mission to assess improvement areas in its structure, staffing, legal framework, core tax administration processes, and computer systems.

The Mongolian government and the IMF worked together to reorganize the taxpayer office into units based on tax administration functions (tripling the staff and creating a special mining audit unit), issue administrative guidance on practical application of tax laws, design industry-specific audit methods, and acquire a new computer system. The success of the reforms was evident in the high rate of on-time tax returns filed electronically and the sharp reduction in tax arrears.

Public Financial Management

The IMF works with its member countries to provide public financial and public investment management support to ensure that countries use their fiscal resources effectively and in support of sustainable development. For instance, in Senegal, the IMF assisted with the ongoing modernization of the Ministry of Economy, Finance, and Planning and the implementation of the country's public financial management reform agenda to ensure a smooth transition and sound changes among the General Directorate of Budget.

In Nigeria, the IMF helped the government implement a treasury single account, which now includes most ministries, departments, and agencies—representing about 98 percent of budgetary expenditure. Substantial idle funds (to the tune of 2 percent of GDP during August 2015–January 2016) were pooled into the Treasury Single Account from the bank accounts of ministries, departments, and agencies. Nigeria now has one of the most comprehensive treasury single accounts in the world.

The rollout of the new Public Investment Management Assessment program has been instrumental to the IMF’s ability to help countries identify strengths and weaknesses in their public investment management. These assessments are now being used to identify reform priorities, help shape follow-up capacity development by the IMF and other providers, and galvanize donor funding. For example, in Togo, based on the assessment results and recommendations, the World Bank has finalized, with financial support from the European Union (EU), a $15 million project mainly to strengthen project appraisal, selection, and procurement.

The IMF also increasingly recognizes the importance of peer learning in facilitating and encouraging public financial management reforms. For example, the IMF has supported the Latin American Treasuries (FOTEGAL) as a useful forum for sharing experiences within the region and a platform for the delivery of training and workshops. These efforts have helped countries in the region substantially improve the design and operation of the treasury single accounts, implement more active cash management, develop business continuity plans, and expand use of electronic payment instruments.

Support for Fragile States

A critical focus of the IMF’s fiscal capacity development continues to be support for members whose institutional and policymaking capacity has been affected by conflict or other shocks. For instance, in Haiti, the IMF helped achieve meaningful improvements in institutional capacity, including the establishment of a macro-fiscal unit in the Ministry of Finance and accounting functions across the government. In 2017, the treasury single account, covering budgetary central government, was further operationalized.

In Mali, since the 2015 peace agreement, the IMF has focused its capacity development efforts on key expenditure processes, cash management, and fiscal decentralization—the latter being a crucial provision in the peace agreement. During 2016–17, with the IMF’s assistance, the Malian authorities made noticeable progress to upgrade and roll out the Treasury's computerized accounting system to pool general government cash under the treasury single account and improve key institutions for public investment management.

BOX 2.2 FISCAL ASSESSMENT TOOLS

The IMF has been effectively leveraging fiscal assessment tools to strengthen the analytical basis for designing effective and results-oriented capacity development programs in member countries.

- During FY2017, the Tax Administration Diagnostic Assessment Tool (TADAT) was applied in 19 countries, helping identify reform priorities for tax administrations.

- The Revenue Administration Fiscal Information Tool (RA-FIT) initiative gathered momentum with the launch of the International Survey on Revenue Administration (ISORA) in May 2016. This provides a convenient platform for gathering performance indicators for customs and tax administrations; more than 140 tax administrations have completed the survey.

- The Revenue Administration Gap Analysis Program (RA-GAP) provides an analytical basis for estimating the gap between current and potential revenues, and in the past year the tool has extended its scope to enable estimates of the corporate income tax gap.

- The Fiscal Analysis of Resource Industries (FARI) tool is a model-based framework that was initially designed to support the reform of mining and petroleum fiscal regimes. More recently, some tax administrations have started using an application of the tool for tax compliance and risk assessment.

- The Fiscal Transparency Evaluations (FTEs) assess country compliance with the IMF’s Fiscal Transparency Code. The IMF delivered five FTEs in FY2017, establishing for the participating members an important baseline for reforms. For example, recommendations in the Brazil FTE informed the discussion in the establishment of a Senate-based independent fiscal institution in December 2016, with a broad mandate to include assessments of the government’s fiscal targets and the evaluation of their fiscal impact. Similarly, the United Kingdom FTE, published in November 2016, was credited by the chancellor of the exchequer, during his autumn 2016 statement, for the decision to move to a single fall fiscal event, replacing the existing dual spring and autumn budgets. The chancellor argued that the move to the single event, well in advance of the start of the fiscal year, would allow for greater parliamentary scrutiny of budget measures.

- The Fiscal Stress Test was designed and released as part of the “Analyzing and Managing Fiscal Risks—Best Practices” Board paper, which applied fiscal stress tests to Iceland and Peru. Some advanced economies have already begun using the stress test internally to assess their exposures.

- The Public Investment Management Assessment (PIMA) is a comprehensive diagnostic tool that helps countries evaluate the strength of their public investment management practices from a macro-fiscal perspective. Introduced in the second half of 2015, the PIMA has been applied in 21 countries with different income and development levels. During FY2017, the PIMA was applied in six emerging market economies and six low-income countries.

- The Public-Private-Partnerships Fiscal Risk Assessment Model (PFRAM), developed by the IMF and the World Bank, is an analytical tool to assess the potential fiscal costs and risks arising from public-private partnership projects. The PFRAM was launched in April 2016, and has been applied in FY2017 in the IMF’s and World Bank’s technical assistance missions to emerging market economies and low-income developing countries.

![]()

Highlights: Monetary and Financial Sector Capacity Development

At a time of significant global economic risks and vulnerabilities, the IMF’s capacity development efforts in the monetary and financial sectors aim to address the critical needs of member countries: promotion of monetary and financial stability and prevention and management of crises. This includes supporting members in the core areas of financial regulation and supervision, monetary policy and central bank operations, debt management, and other aspects of financial stability.

The IMF is responding to the evolving needs of members, including by managing the impact of weak commodity prices on exchange rate policies, helping develop debt management capacity in oil-exporting countries, helping members shift from compliance- to risk-based financial supervision, supporting members’ Basel II/III implementation, and adapting macroprudential policies to emerging market economy needs.

Through its Managing Natural Resource Wealth Trust Fund, the IMF has expanded its capacity development to countries dependent on exporting natural resources. These countries have seen large fluctuations in their terms of trade recently. This puts pressure on their monetary policy frameworks—which often involve managed exchange rate regimes (if not outright pegs)—and on the stability of their financial systems. The IMF is adding resources to resource-rich countries in the areas of both monetary and macroprudential policies.

In November 2016, the IMF and the China Securities Regulatory Commission (CSRC) signed an agreement to enhance technical cooperation to support the commission's financial sector reforms. The cooperation will focus on securities markets regulation and supervision, systemic risk monitoring and prevention, and stakeholder communication.

The following are examples of the IMF’s monetary and financial sector capacity development:

- Modernizing monetary policy in central Africa: The IMF is stepping up its capacity development activities in the Central African Economic and Monetary Community to assist the authorities with managing the currently difficult external context. An IMF resident advisor in the IMF’s Central African Regional Technical Assistance Center is in regular contact with the regional supervisors to provide training sessions and workshops. From headquarters, IMF staff delivered intense, hands-on sessions on monetary policy implementation and emergency liquidity assistance to officials from the Banque des Etats d’Afrique Centrale (Bank of Central African States [BEAC]). The BEAC has demonstrated strong ownership of modernizing its monetary policy framework, reflecting several years of capacity development now coming to fruition. The IMF plans to assign a long-term advisor to assist the BEAC during implementation of the reforms.

- Building financial stability frameworks in Asia: Over the past 20 years, as Asian financial sectors have become bigger and closely intertwined, consolidating the monitoring and supervision of these financial conglomerates has become critical for detecting risks to financial stability. In recent years, countries such as Indonesia, the Philippines, and Thailand have worked with the IMF to institute a systematic approach to monitoring financial stability and strengthening the systemic oversight framework and risk analysis. The Bank of Thailand inaugurated its own Financial Stability Unit in 2016. The Philippines’ central bank has also set up a dedicated financial stability function. The Bank of Indonesia is developing the capacity for systemic risk assessment, macroprudential oversight, and stress testing.

- Bank restructuring in the Eastern Caribbean Currency Union: Following the 2008 global financial crisis, the Eastern Caribbean Currency Union (ECCU) faced high public debt and stretched finances, leading the Eastern Caribbean Central Bank (ECCB) to place three domestic banks into conservatorship. To strengthen its financial system through improved regulation and supervision, the ECCB worked with the IMF to revise banking legislative frameworks and increase the central bank’s ability to monitor progress made by the banks in conservatorship. Since the start of this effort, the ECCU has witnessed a regionwide implementation of modern banking legislation, leading to greater supervision and revisions to the region’s medium-term fiscal framework. By April 2016, all three conservatorships had been resolved. The effort also led to a new Banking Act and the Eastern Caribbean Asset Management Company Act, both approved in all ECCU jurisdictions.

- Upgrading banking supervision in the Kyrgyz Republic: The IMF’s 2013 financial sector assessment found weaknesses in the Kyrgyz Republic’s banking supervision pertaining to its legal framework. The IMF began working with the National Bank of the Kyrgyz Republic to establish a risk-based supervisory process and train the bank’s supervisory staff. The revised regulatory framework will align with international standards that support risk-based and consolidated supervision; prudential guidelines and the operational framework are also being strengthened. This project is currently underway and is expected to lead to full implementation, including an upgrade of the bank’s resolutions, guidelines, and regulations.

- Banking and insurance supervision in Montenegro: Launched in March 2017, the project focuses on understanding and assessing groupwide risks, enhancing the prudential framework and the assessment of asset quality, and increasing the effectiveness of credit risk management including the central bank’s ability to supervise this risk. The supervision will help the Insurance Supervisory Agency adopt a risk-based supervisory framework in preparation for implementation of the Solvency II regime. The project will also support the Insurance Supervisory Agency’s introduction of guidelines on corporate governance and requirement for risk management and internal controls.

![]()

Highlights: Statistics Capacity Development

High-quality, timely macroeconomic data are the foundation for all economic decision making. The IMF helps countries with compilation, management, and reporting of their macroeconomic and financial statistics data. This provides more accurate understanding of their economy—including of economic vulnerabilities and risks—and helps government officials design informed policies. Sound economic data also send a message of transparency and foster trust in government policies, thereby attracting investors who use such data to gauge macroeconomic stability.

In the past five years, IMF capacity development in statistics has grown by more than 20 percent. With funding from bilateral and multilateral partners, much of this is directed at low- and middle-income countries and at fragile economies. The IMF routes a significant portion of this effort through its 14 regional capacity development centers, six of which are based in Africa. IMF capacity development in statistics is provided by long-term resident advisors, supplemented by short-term experts and missions from IMF headquarters.

The IMF support focuses mainly on real sector and government finance statistics, with some work on external sector statistics. For example, through its Africa Regional Technical Assistance Center (AFRITAC) South—covering Angola, Botswana, Comoros, Lesotho, Madagascar, Mauritius, Mozambique, Namibia, Seychelles, South Africa, Swaziland, Zambia, and Zimbabwe—the IMF has assisted several countries in rebasing their national accounts statistics to update information on the structure of the economy and to further develop price indices, especially the consumer price index. This is helping countries provide more accurate information on inflation and price trends.

The IMF is in the second phase of a major initiative, the Enhanced Data Dissemination Initiative, to improve macroeconomic statistics in 45 countries across Africa, the Middle East, and the Central Asia region. Financed by the United Kingdom’s Department for International Development, the project has helped identify and develop new data sources, such as administrative tax records, especially for national accounts statistics. With the intensified implementation of the enhanced General Data Dissemination System (e-GDDS) framework, several countries are now disseminating data using an Open Data Platform.

As members of the East African Community (EAC)—Burundi, Kenya, Rwanda, South Sudan, Tanzania, and Uganda—prepare for a monetary union, the countries needed to ensure harmonization of data; that is, a common set of consistent, comparable government finance statistics. Since 2013, with support from IMF statistics capacity development and financing from the government of Japan, the countries have expanded their monetary and financial statistics coverage, taken steps to harmonize the underlying source data, improved EAC-wide classifications, and made substantial progress in collecting data on intra-EAC positions—an essential component for compiling union-wide monetary statistics.

In addition, all EAC partner states will compile and disseminate their financial soundness indicators (FSIs) once South Sudan begins to disseminate the compiled data (planned in 2017). Together, the United Kingdom and Japan have financed work across the globe that has led to 30 new reporters to the FSI database since 2013.

The IMF, with financial support from Switzerland, also worked with five countries in southeastern Europe—Albania, Bosnia and Herzegovina, Kosovo, FYR Macedonia, and Serbia—on government finance statistics to enhance their fiscal policy formulation and analysis to help meet European reporting requirements. In the second phase of this work, which began in June 2016, countries have begun to analyze economic developments and underlying fiscal positions to formulate and implement macroeconomic policies, capture and assess fiscal risks, promote fiscal transparency, and work toward greater compliance with EU procedures for correcting excessive deficit or debt levels.

Additional work in the areas of real, external, government finance, and monetary and financial statistics, as well as on data dissemination, is being undertaken in eastern Europe, central Asia, southeastern Asia, and South America, with funding from Japan, Switzerland, and the Netherlands. This work will be complemented by two new topical trust funds for capacity development worldwide: the Financial Sector Stability Fund for financial sector statistics, and the Data for Decisions Fund for policy-relevant statistics. Both trust funds aim to provide more and better data to policymakers and help develop national statistical systems in support of the Sustainable Development Goals.

![]()

Highlights: Legal Capacity Building

Demand for technical assistance on legal issues in both program and nonprogram countries continued in FY2017 in anti-money-laundering and combating the financing of terrorism (AML/CFT) efforts, financial and fiscal law, insolvency, and claims enforcement.

The IMF continued its work in AML/CFT with the Financial Action Task Force (FATF), the World Bank, the Egmont Group of Financial Intelligence Units, and FATF-style regional bodies. The IMF led the assessment of Mexico under the revised international standard. It continued the successful global program of technical assistance under the multipartner AML/CFT Topical Trust Fund; delivered technical assistance on AML/CFT in Myanmar (funded by Japan) and Panama and on anticorruption efforts in Ukraine (funded by Canada) and in Qatar, Kuwait, and Saudi Arabia (all self-funded); undertook a regional legal drafting project on CFT in the Middle East and North Africa; and continued to coordinate its work both internally and with many international assistance providers.

In the area of financial and fiscal law, technical assistance on central banking, bank regulatory and supervisory frameworks, and bank resolution and crisis management were maintained at previous levels. In contrast, technical assistance on market infrastructures (payment systems) was minimal but continued to grow on legal frameworks for public financial management, as in previous years.

Technical assistance on tax law continued to see strong demand in the main areas of income tax, value-added tax, and tax procedures, with particular emphasis on international aspects, reflecting the increased global attention to international tax issues. Similarly, international tax law design issues were at the core of both a headquarters-based seminar and a training session in Kuwait, the latter focusing specifically on regional issues.

The IMF continued to provide technical assistance to its members on corporate and household insolvency and claims enforcement to help ensure early and rapid rehabilitation of viable businesses and liquidation of nonviable businesses, provide a fresh start for overindebted households, and improve the process of claims enforcement. The IMF also organized a workshop for high-level officials at the Joint Vienna Institute on corporate and household insolvency.

![]()

Highlights: Training

The IMF’s training program is an integral part of its capacity development mandate. The IMF helps train government officials so they improve their ability to analyze economic developments; develop diagnostic, forecasting, and modeling tools; and formulate and implement sound macroeconomic and financial policies. The IMF delivered 355 face-to-face training courses in FY2017, through theoretical lectures, analytical tools, and hands-on workshops, plus 19 online courses.

Curriculum review: After a two-year review and assessment, in 2017 the IMF completed a comprehensive revamp of its external curriculum that builds on its roots in policy-oriented macroeconomics and includes topics that meet the changing needs of its members and of the IMF’s evolving mandate. A total of 19 new courses were designed, developed, and rolled out during the year, spanning five areas: general macroeconomics, fiscal issues, monetary issues, the external sector, and finance, along with special topics such as inclusive growth. They all have in common an emphasis on hands-on training, country case studies, cross-country experience, and policy implications.

Online training: An increasing number of IMF courses are being delivered online. Offered as massive open online courses, or MOOCs, on the edX platform, these courses are made available to government officials and to the general public. These courses complement the IMF’s traditional face-to-face delivery: online training emphasizes introductory courses with a view both to extending the reach of the IMF’s training and preparing participants for face-to-face courses.

Customized training: Increased demand from member countries for training material tailored to country needs has led the IMF to respond more flexibly to these changing needs with new modular courses, which can be customized. In some cases, the IMF is working with specific institutions within member countries on such customization. For example, the IMF has worked with central banks in Ghana, Mozambique, the East African Community region, and Sri Lanka on a forecasting and policy analysis system to strengthen their monetary policy frameworks. Other customized training initiatives include a course on cross-border position statistics for Chinese officials at IMF headquarters, projects on dynamic stochastic general equilibrium modeling for policy analysis in China and Bolivia, and training in financial programming and policy in the Central African Economic and Monetary Community.

![]()

IMF Capacity Development in Numbers

Initiated by member countries, IMF capacity development support, which includes both institutional and policy development (technical assistance) and staff development (training), has reached all 189 members. Capacity development represented over a quarter of the IMF’s administrative spending in FY2017. Most of this spending was on technical assistance, which represents 23 percent of total administrative spending, while training accounts for 5 percent (see Figure 2.5).

![]()

IMF capacity development activities continued to grow in FY2017, reflecting mainly greater delivery to sub-Saharan Africa, the Middle East and Central Asia, and Europe. Delivery of technical assistance on fiscal and legal topics increased. Total direct spending on capacity development activities (externally and IMF financed) was $267 million in FY2017, compared with $256 million in FY2016, a growth of 4 percent (Figure 2.6). The externally funded component amounted to $134 million, or 50 percent of the total, and grew by almost 6 percent in FY2017.

![]()

Technical Assistance

Technical assistance delivery declined slightly in FY2017. Increased delivery in sub-Saharan Africa, the Middle East and central Asia, and Europe was broadly offset by declines in the Western Hemisphere and Asia and the Pacific (Figure 2.7). About half of all IMF technical assistance continues to go to low-income developing countries (Figure 2.8).

In FY2017, sub-Saharan Africa received the largest share of technical assistance, reflecting the high number of low-income developing countries in this region. Delivery of technical assistance on fiscal topics increased, in response to demand from the membership (Figure 2.9). Fiscal topics continued to constitute slightly more than half of the technical assistance provided by the IMF.

![]()

![]()

![]()

Training

During FY2017, the IMF delivered 225 training events through its Institute for Capacity Development (ICD) training program, in which 9,517 officials from 183 member countries participated. Most of these events were delivered through the IMF’s network of regional training centers and programs and online courses, with the remainder delivered at IMF headquarters or other overseas locations. A wide range of topics meet different needs, spanning macroeconomic policies, forecasting and macroeconomic modeling, financial programming and policies, financial sector issues, specialized fiscal courses, macroeconomic statistics, safeguards assessments, and legal issues. Emerging market and middle-income economies received the largest share of the ICD training program, 57 percent of the total for the year (Figure 2.10). Regionally, the share of the Middle East and central Asia was the largest at 27 percent, followed by sub-Saharan Africa and Asia and the Pacific (Figure 2.11).

The IMF’s massive open online courses, which are free, continued to grow with the addition of a "Macroeconomic Diagnostics" course and an Arabic version of "Financial Programming and Policies, Part 1." With 19 online courses delivered across five languages, participation in online training remained strong in FY2017. The largest share of users came from sub-Saharan Africa, which represents 28 percent of online training. Since the program was launched in late 2013, more than 34,000 active participants have enrolled in the IMF’s online courses. Of those, about 9,400 government officials and 9,800 members of the general public from 186 countries have successfully completed an online course.

![]()

![]()

![]()

Partnerships for Capacity Development

Strong global partnerships underpin the IMF’s capacity development activities. The financial contributions from partners, paired with the IMF’s own resources, enable delivery of high-quality capacity development services, aligned with member country needs and with IMF and global priorities (see Table 2.5).

Table 2.5

IMF partners in capacity development

In FY2017, new contributions to IMF capacity development of $126 million were received, and activities financed by partners totaled about $150 million, roughly half of total capacity development activities. Over the past five years, the top five contributors to IMF capacity development were Japan, the EU, the United Kingdom, Switzerland, and Canada. In FY2017, the IMF deepened existing partnerships with the EU, Japan, the United Kingdom, Germany, Switzerland, the Netherlands, Australia, Belgium, and Luxembourg.

Key partnership highlights include the following:

- Japan, the largest contributor to the IMF’s capacity development efforts, disbursed $29 million in FY2017, and signed an agreement in April 2017 to expand the IMF’s online learning program.

- The European Commission, through its Directorate-General for International Development and Cooperation, signed a new Strategic Partnership Framework with the IMF in December 2016 for developing countries focused on achieving the UN SDGs.

- Another Strategic Partnership Framework with the United Kingdom’s Department for International Development will improve communication and coherence and ease funding decisions.

- In the context of the G20 Compact with Africa, in April 2017 Germany strengthened its support for IMF capacity development with a contribution of €15 million for all regional capacity development centers on the continent (see Box 2.3).

- The IMF took significant steps toward expanding its network of partners, including an agreement signed by India for approximately $33 million to cover activities related to the new South Asia Regional Training and Technical Assistance Center (see Regional Highlights on Asia).

- Close engagement continued with several private foundations, including the Bill and Melinda Gates and Hewlett Foundations.

IMF partnerships on global thematic funds, which directly respond to the Financing for Development Agenda, ensure that less-developed economies have the tools they need to reach their post-2015 SDGs.

BOX 2.3 G20 COMPACT WITH AFRICA

Growth in Africa has weakened since 2014 in the wake of the recent commodity price decline, but its medium-term prospects remain strong. Its potential will be achieved only with sustained effort to harness Africa’s demographic dividend, boost private capital inflows and mobilize domestic finance, and seize the opportunities presented by globalization to deliver economic transformation and create productive jobs.

To accelerate growth, investment rates and efficiency need to increase. Priority should be given to investment in infrastructure, which is critical to attract private investment, connect Africa’s regional markets, and better integrate those markets into global value chains. It is estimated that the regional deficit in physical infrastructure reduces growth by 2 percentage points a year. Of the approximately $100 billion a year Africa needs to close the infrastructure gap, slightly less than half has financing.

The G20 Compact with Africa presents a broad set of potential mutual commitments between interested African and G20 and partner countries—with support from international organizations—to raise private investment and increase efficient public investment in infrastructure. The commitments are detailed in a report commissioned by the G20 finance deputies for the G20 Finance Ministers and Central Bank Governors Meeting in Baden-Baden, Germany, in March 2017 and prepared jointly by the IMF, World Bank, and African Development Bank.

Participation in the Compact with Africa will send a strong signal to private investors about African countries’ interest in attracting investment and their commitment to implementing key reforms. The G20 will ensure high political visibility and raise investor awareness and confidence. The countries will benefit from a comprehensive but modular approach and coordinated engagement by the IMF, World Bank, and African Development Bank to support national efforts to devise and implement reform programs to boost private sector investment.

G20 members and other partner countries will encourage their domestic investors to respond to the investment opportunities in participating African countries, and knowledge sharing among partners will enhance their engagement with these participants. African countries will seek to create a more enabling environment for private investment, better mobilize domestic revenue and finance, and create space to scale up critically needed public investment in infrastructure while ensuring debt sustainability.

The IMF will share its expertise in the areas of debt management, fiscal transparency, tax administration and reform, resource management, public investment management, and data standards through its network of Regional Technical Assistance Centers in Africa.

Recent highlights include the following:

- New phases of the Revenue Mobilization Fund (RM)—supported by Australia, Belgium, the European Union, Germany, Japan, Luxembourg, the Netherlands, and Switzerland—and the Managing Natural Resource Wealth Fund (MNRW)—supported by Australia, the European Union, the Netherlands, Norway, and Switzerland—were launched in July 2016 to ensure sustained support for countries in strengthening tax capacity and effectively mobilizing natural resource wealth.

- The Data for Decisions Fund (D4D) was endorsed by IMF management in March 2017 and will improve the quality, coverage, timeliness, and dissemination of macroeconomic statistics of beneficiary authorities. The D4D Fund will also sustain the Financial Access Survey, portions of which are used to measure UN SDG indicators.

- In support of the objective that financial inclusion and development go hand in hand with financial stability, the Financial Sector Stability Fund (FSSF) was officially launched in April 2017; first pledges were made by Italy and Luxembourg.

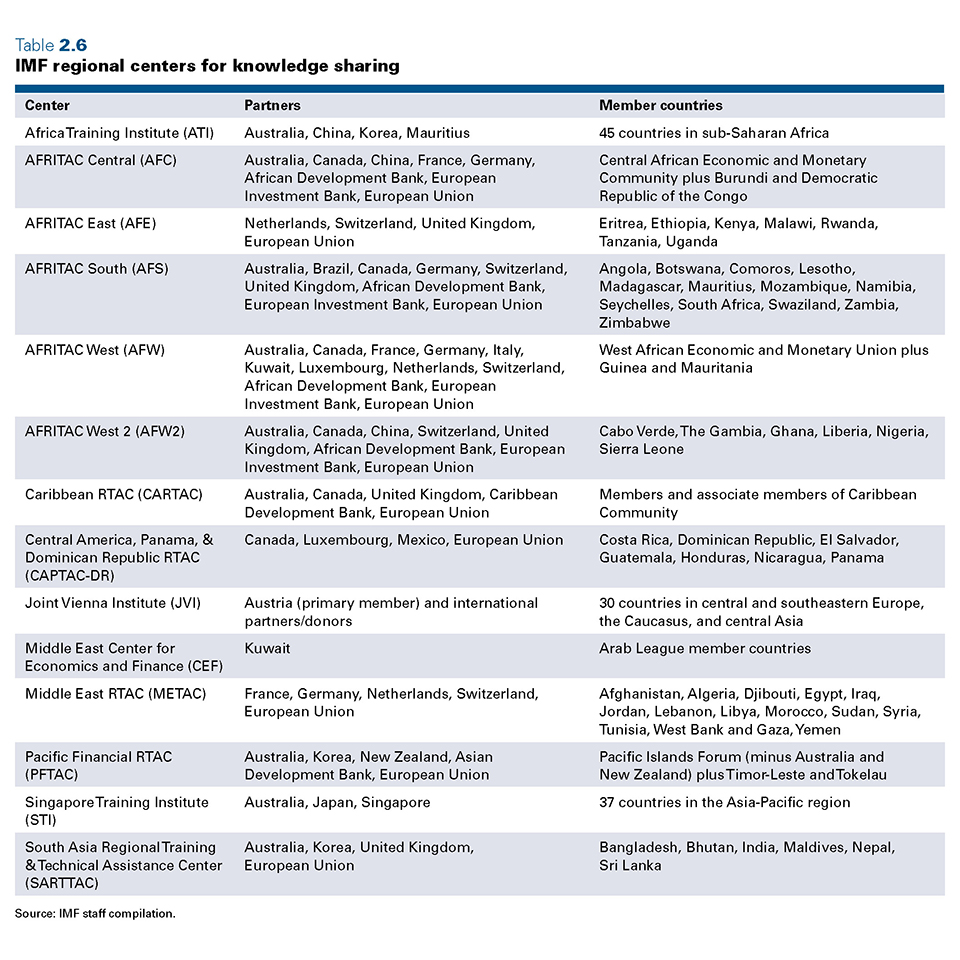

Regional capacity development centers remain the backbone of the IMF’s capacity development infrastructure, delivering about half of the IMF’s capacity development efforts. The centers facilitate an enhanced ability for the IMF to respond quickly to a country’s emerging needs, as well as closer coordination with other development partners on the ground.

These locally based regional centers anchor IMF support for knowledge sharing and are financed jointly by the IMF, external development partners, and member countries. Table 2.6 lists the main centers.

Table 2.6

IMF regional centers for knowledge sharing

Highlights in FY2017 include the following:

- The European Union continued to be the IMF’s largest partner for the regional centers; in FY2017 alone, it signed agreements to support the South Asia Regional Training and Technical Assistance Center, the Caribbean Regional Technical Assistance Center, and the Central African Regional Technical Assistance Center.

- The Middle East Regional Technical Assistance Center welcomed four new members—Algeria, Djibouti, Morocco, and Tunisia—with the start of its new program phase in May 2016, and will scale up operations in the coming year.

- The IMF’s oldest center, the Pacific Financial Technical Assistance Center, began its newest program phase in November 2016, with all 16 member countries and territories contributing approximately 10 percent of the center’s budget; additional funds from New Zealand, Australia, the European Union, the Asian Development Bank, and Korea helped get the new phase off to a strong start.

- The new program phase of the Caribbean Regional Technical Assistance Center began in January 2017 with an $11 million (Can$15 million) contribution from Canada and with a new member, Curaçao. Two more countries—Aruba and Sint Maarten—are considering joining the center.

- Thanks to additional contributions by Luxembourg to the Central America, Panama, and Dominican Republic Regional Technical Assistance Center, the center is fully funded for the remainder of its current program phase, through April 2019.

- The global network of IMF regional capacity development centers was further bolstered with the South Asia Regional Training and Technical Assistance Center’s official inauguration in February 2017. Member countries—notably India—financed two-thirds of the center’s budget.

![]()

The South Asia Regional Training and Technical Assistance Center

The South Asia Regional Training and Technical Assistance Center is the newest addition to the IMF’s global network of 14 regional centers and began operations in January 2017. This is the first center to fully integrate training and technical advice and is a model for the IMF’s future capacity development work—see Regional Highlights on Asia in Part 1.

![]()

Common Evaluation Framework

A new common evaluation framework was launched in FY2017. Key elements of the framework are grouped around the following objectives:

- Producing shorter, more focused, and more comparable evaluations

- Improving the information supporting evaluations

- Spending the same level of resources on evaluation while allocating these scarce resources more efficiently

- Using the information from evaluations to alter practices or shift the targeting of capacity development resources

The common evaluation framework is intended to provide cross-activity and cross-IMF comparability, permit aggregation, and enable an overall assessment of performance. Around this common approach, the framework allows flexibility to adapt evaluations to reflect the wide range of IMF capacity development.