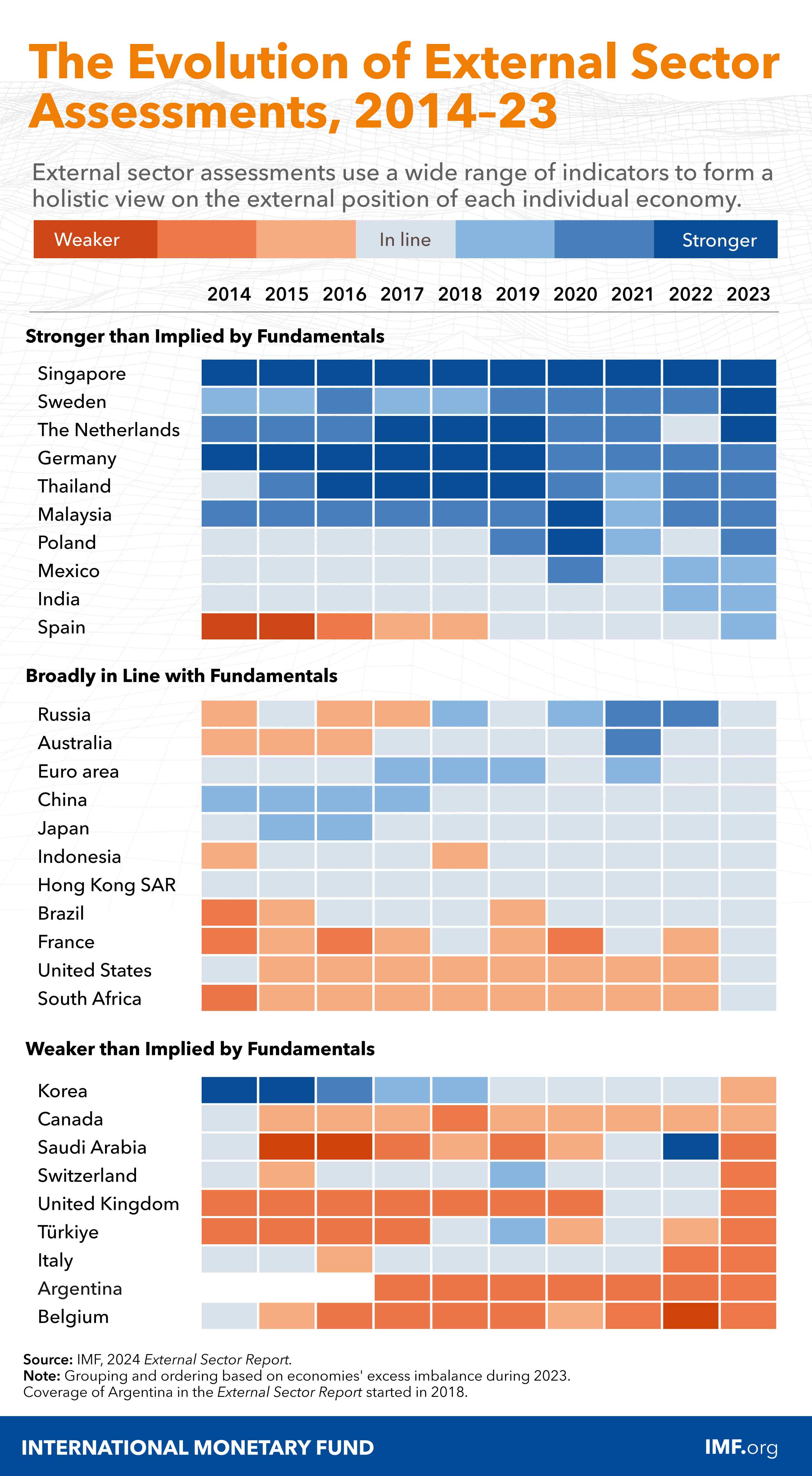

This year’s report provides the external sector assessment of 30 of the world’s largest economies on the basis of their 2023 data. With tight monetary policy conditions in key advanced economies continuing in 2023, the US dollar remained strong in 2023 and early 2024 by historical standards, while other reserve currency movements have been mixed. Net capital inflows to emerging market and developing economies recovered slightly from the lows experienced in 2022 but remained negative in 2023. Gross inflows and outflows in emerging markets declined, however. Against this background, the global current account balance (defined as the cross-country sum of absolute values of current account) narrowed significantly in 2023, while the excess global current account balance (in excess of the current account norms) has remained broadly unchanged relative to 2022.

The report also analyzes the historical pattern in the external sector implications of energy price swings. Energy-importing countries are exposed to adverse effects of negative oil supply shocks but can adopt several policy measures to soften the impact. Possible implications of the clean energy transition and the evolving correlation between the oil price and US dollar are discussed. Lastly, the report contains external sector assessments of individual economies, which are based on a wide range of methods including a multilaterally consistent model of current accounts.

Chapter 1: External Positions and Policies

Chapter 2: Navigating the Tides of Commodity Prices

Chapter 3: 2023 Individual Economy Assessments

Publications

{kind=link}

December 2025

Finance & Development

- More Data, Now What?

Annual Report 2025

- Getting to Growth in an Age of Uncertainty

Regional Economic Outlooks

- Latest Issues