A Strategic Pivot in Global Fiscal Policy

September 18, 2024

It is a pleasure to be here today to deliver the Whitaker Lecture. Ken Whitaker made extraordinary contributions to public policy through his diverse roles as head of the Finance Ministry, as central bank governor, and as a senator. In 1958 he famously engineered a strategic pivot in Ireland’s economic policies away from protectionism and towards encouraging foreign investment. Through his “Programme for Economic Development” Ireland’s economic fortunes were transformed.

Today, I will draw inspiration from Mr. Whitaker and use my lecture to push, more modestly, for a strategic pivot in global fiscal policy. This is critical to ensure that governments will have the resources needed to invest in structural transformations including climate change, and to fight the next crisis.

Global public debt has grown sizably over the last few years as governments tackled pandemics and energy and food insecurity. Public debt reached 93 percent of GDP in 2023 and is projected to approach 100 percent of GDP by the end of this decade. Debt in some of the largest economies like the US and China is projected to grow even faster than in the pre-pandemic years. Although public debt in Europe is expected to broadly stabilize, debt remains well-above pre-pandemic levels.

With monetary policy easing and unemployment at low levels in several countries, now is the time for a strategic pivot in fiscal policy. Such a pivot begins with a recognition of the true scale of fiscal risks: It is worse than you think. This calls for further recognizing that the economic consequences of high debt can no longer be dismissed in advanced economies. Borrowing costs and economic activity are increasingly impacted by loose fiscal policy. Lastly, for any fiscal strategy to succeed, economically and politically, it will need to focus on growth, guardrails, and grassroots.

I will develop each of these points in my lecture.

Scale of Fiscal Risks

First, let’s look at the true scale of fiscal risks. There are several upside risks here.

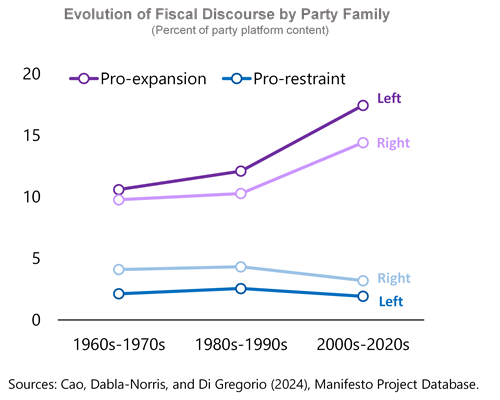

To start with, there has been a significant change in the political economy environment. New IMF research documents that over the last few decades the political discourse on fiscal issues has become increasingly favorable to higher government spending. Political manifestos (or platforms) have a growing share of statements favoring public spending.

At the same time, restraint discourse – the share of a political manifesto calling for an outright reduction of budget deficits or the limitation of public spending – has declined across the board over time. Moreover, political redlines on raising taxes are becoming more entrenched. This is the case both for advanced economies and for emerging and developing economies. This is the case regardless of party ideologies – left or right. This pro-expansion trend creates significant upside risks for the debt outlook. While now is a good time to reduce deficits in several countries, governments instead may choose to kick the can down the road.

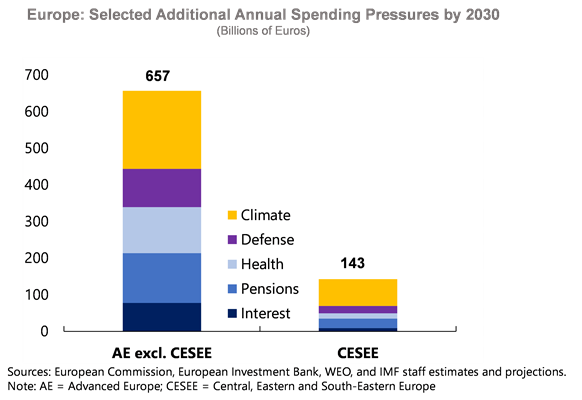

In addition to political shifts, there are big structural shifts that call for greater government spending. Countries will need to spend more on climate mitigation and adaptation, on healthcare and on pensions as populations age, and on defense needs as geopolitical tensions rise.

This new spending could amount to 7-8 percent of GDP annually on average for the global economy by 2030. For Europe this would add up to 2.5-5 percent of GDP, that is 550 billion to 1.1 trillion euros by 2030. These spending pressures may not be fully accounted for in baseline debt projections and are therefore likely to amplify upside risks to the debt outlook.

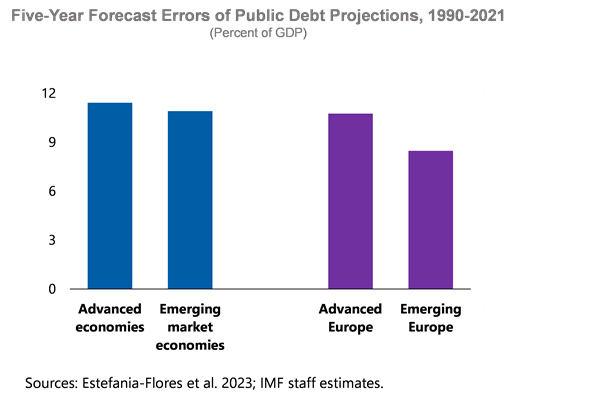

Finally, experience confirms there is an optimism bias in debt projections. Analysis covering the period between 1990 and 2021 shows that realized debt-to-GDP ratios in many countries tend to be significantly higher than projected over the medium-term. The two main reasons for this are optimistic growth projections – crises and pandemics are unforecastable --and realized fiscal adjustments that fall far short of plans. This bias can be seen in Europe, with outcomes exceeding forecasts significantly over a 5-year horizon. If history were to repeat itself, debt could rise by 8-11 percentage points of GDP above the baseline projections in European economies by 2030.

Consequences of elevated fiscal risks

As daunting as the fiscal risks are, you may think: ‘So what?’ Many advanced economies have kept high debt levels for a long time and nothing dramatic has happened. Why should we be concerned now? This leads me to my second main point: We should be concerned because we are no longer in the era of a global savings glut or of large-scale purchases of government bonds by central banks, both of which drove bonds yields to record lows.

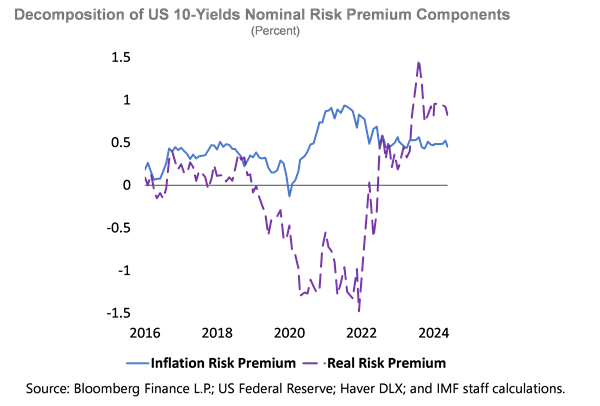

In the world we are in now, loose fiscal policy can increase term premia on government bonds as long-term debt sustainability comes into question. A decomposition of US 10-year nominal yields reveals that while inflation risk premium has declined in tandem with inflation, real risk premium has risen sharply in the last two years pushing up long-term interest rates well above pre-pandemic levels. The large current and expected fiscal deficits in the US are among the factors driving US borrowing costs higher.

Our April 2024 Fiscal Monitor shows that all else being equal, a 1 percentage point increase in the US primary deficit is associated with a rise in term premia of about 11 basis points in the quarters that follow. So, even for countries thought to be immune to debt dynamics, it might no longer be the case. If we turn to Europe, the recent increase in term premia in France may be seen as one more example of this change.

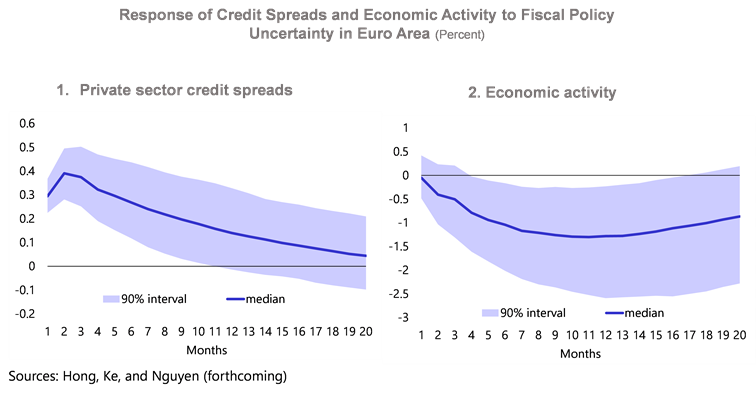

By driving borrowing costs higher, heightened uncertainty regarding the conduct of fiscal policy can dampen economic activity. IMF research finds that a significant increase in fiscal policy uncertainty, as proxied by a two standard deviation shock to our new fiscal uncertainty index, could, on average, increase private sector borrowing spreads in the Euro Area by 0.4 percent one month after the shock, and dampen economic activity by 1 percent after 6 months as financial conditions tighten.

Large deficits in major advanced economies are consequential not just domestically but also for the rest of the world. Analysis in the April 2024 Fiscal Monitor shows that a 1 percentage point spike in US rates is associated with a rise in long-term nominal interest rates of up to 90 basis points in other advanced economies, with a persistent impact over many months. The spillovers to emerging and developing economies are also substantial.

Fiscal strategy focused on growth, guardrails, and grassroots

I hope I have demonstrated why even advanced economies need to act resolutely to reduce deficits and address their growing debts. The key question is how to do this in an economically and politically sustainable manner. The answer includes growth, guardrails, and grassroots. Let me explain.

Growth

Higher growth is essential because it improves prosperity and living standards; reduces debt durably; and creates policy space to tackle mounting spending pressures.

Accordingly, fiscal adjustments need to be growth friendly. Our forthcoming Fiscal Monitor demonstrates that all fiscal adjustments are not alike. Cuts in public investment have a much larger negative impact on output than reducing energy subsidies and transfers that are not targeted to poorer households.

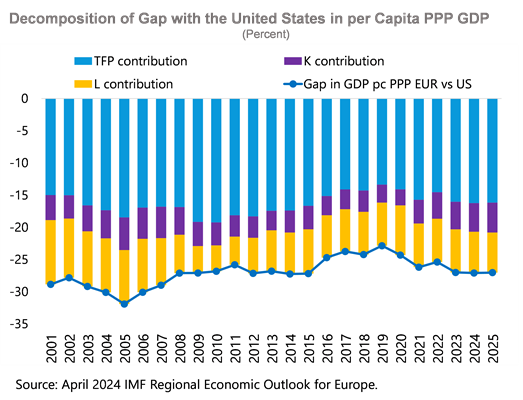

As is the case for many countries, Europe needs to raise productivity and stimulate innovation to lift its medium-term growth prospects. Productivity in the EU is only 78 percent of that in the United States, and this gap is most dramatic in the technology sector.

The singular reform that can help close this productivity gap and that will be fiscally friendly is “strengthening the single market.” The EU should remove remaining barriers to trading inside the block. This will incentivize firms to undertake research and development and other investments in new technologies that only pay off with a large customer base. Opening the electricity and telecommunications sectors are good examples of this.

Advancing the capital markets union is essential to ensure a better, more innovation-friendly, allocation of financing within Europe. Completing the banking union will likewise allow borrowing costs to converge further across the EU and improve the allocation of credit. All these measures will help raise business dynamism in the region.

Guardrails

In addition to investing in growth, it is important to have guardrails to protect against political expediencies and optimism bias.

Medium term fiscal rules and independent fiscal councils provide such guardrails for fiscal policy. They help reduce fiscal policy uncertainty and strengthen transparency.

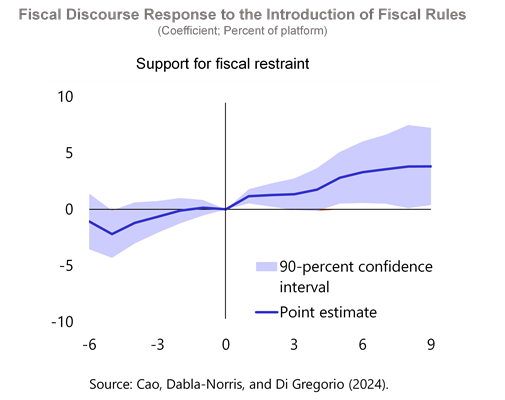

Our research shows that the adoption of fiscal rules that impose operational constraints on the budget balance result in a higher share of pro-restraint fiscal discourse over subsequent election cycles. However, rules alone do not suffice. Fiscal rules need to be complemented with independent fiscal councils to provide oversight, reduce optimism bias in economic forecasts, and help inform the public about risks surrounding public finances and policy tradeoffs.

The new EU fiscal rules are a major development that can help put public finances on a sustainable path. The cumulative fiscal adjustment called for by these rules appears broadly appropriate and similar to IMF staff recommendations. Compliance, however, is critical. The immediate need in many countries is to adopt the deficit-reducing measures needed to stabilize and lower debt burdens.

Most EU countries also have established national fiscal councils. Going forward, these national councils could complement efforts by the European Fiscal Board and provide enhanced checks and balances.

And here, Ireland is a very good example with a council formed in the wake of the Global Financial Crisis. Its adoption demonstrates how these councils can play a valuable role in improving budgetary management, and in helping discipline government decisions around spending and taxation.

Grassroots

In addition to growth and guardrails, the third ingredient of the strategy calls for a focus on ‘grassroots,’ by which I mean efforts to engage with civil society and other key stakeholders to help shape the public discourse towards more sustainable fiscal policy.

Pioneering research from Stefanie Stantcheva at Harvard shows that providing timely and nonpartisan information to societies can reduce misperceptions and shape public support for difficult policies. In the case of climate mitigation policies, our own research shows that support for carbon pricing policies rise when information on its positive impacts is shared with the public.

As the upcoming World Economic Outlook will establish, public ownership of complex reforms will require not just effective communication strategies, but also mechanisms that allow for stakeholders to contribute to the design of these reforms, and strong institutional frameworks that foster trust among the population.

Let me conclude. Political and structural trends are increasingly pressuring governments to spend more and borrow more. If history is any guide, the trajectory of debt will be worse than any of us project today, and considerably so. This is not sustainable, and we need to strategically pivot.

Countries, especially those where output is close to potential, like the US and most in Europe, need to start now on a path of gradual fiscal consolidation. The strategy with the greatest chance of success should focus on growth; have effective guardrails to ensure compliance; and foster close engagement with all stakeholders, including civil society, to ensure their buy-in.

Thank you very much for the opportunity to give the Whitaker lecture and to make the case for a strategic pivot in fiscal policy. To quote the Irishman of the 20th century, Ken Whitaker, “Explanation, admonition and exhortation are a necessary lead-up to policy decisions.” So, let’s get to work. Thank you.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org