Navigating Fragmentation, Conflict, and Large Shocks

June 21, 2024

Introduction

It’s a pleasure to be here with you today at this conference focused on the challenges that large shocks pose for the conduct of monetary policy.

In my presentation, I will discuss the impacts from one such large shock, Russia’s invasion of Ukraine: its direct effects on Ukraine itself, on neighboring countries, and on the global economy. The war is now in its third year, and Ukraine has endured enormous human suffering.

While the direct human and economic costs are staggering, I will argue that the war has been a turning point also for the global economy. It has increased fragmentation pressures and raised defense spending as countries implement measures to strengthen their economic and national security. Such measures help countries adapt to the new reality of conflicts. However, when compared with the decades of efficiency-driven economic integration, these measures will likely make the global economy more shock-prone with higher inflationary pressures, reduced potential output growth, and precarious public finances.

I will next consider several implications for policy:

- How should central banks conduct monetary policy in this more shock-prone environment?

- What is the role of additional tools such as foreign exchange intervention?

- How should fiscal, financial, and structural policies be deployed to support macroeconomic and financial stability?

Effects of war on Ukraine

Strong global support and the macroeconomic policies implemented by the authorities, including the National Bank of Ukraine, have helped Ukraine avoid the deep macroeconomic instability that often accompanies conflicts of this scale, and quite remarkably, have kept inflation from spiraling.

Even so, it is clear that the damage done to Ukraine’s economy is tremendous, with output roughly 25 percent below its pre-war level and much of the capital stock destroyed by war. Ongoing help is needed. The Ukraine Recovery Conference in Berlin (June 11-12) has just been discussing ways in which the world can help, and the IMF will continue to play its role.

Wider impact of the war

But Russia’s war in Ukraine has also cast a far wider shadow on the world. Let’s consider the effects we’ve seen thus far and focus especially on the direct effects of the war on Europe and on Ukraine’s immediate neighbors in Central, Eastern, and South-Eastern Europe (CESEE).

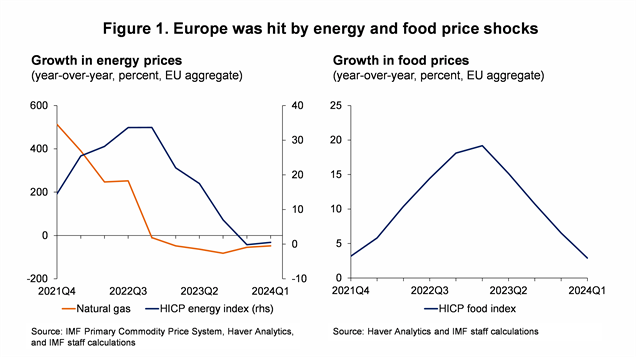

The first is on inflation. The war has been a major supply shock for the global economy, but particularly for CESEE and other European countries heavily reliant on natural gas from Russia. When the gas stopped, energy prices skyrocketed (Figure 1), boosting inflation and delivering a major hit to businesses and households. Disruptions in Ukraine’s exports of grain contributed to food inflation and compounded the hit to consumers. While efforts to conserve and shift energy use to liquified natural gas have paid off, governments have been saddled with more debt while many consumers still face higher energy bills than before the war.

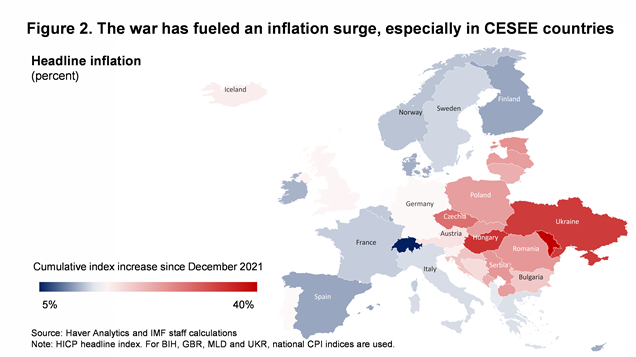

Clearly, as seen in the heatmap in Figure 2, the CESEE region has experienced the largest inflationary impact over the past two years. While inflation has come down a lot, the higher cumulative inflation rates in CESEE countries have left them with a potential competitiveness problem.

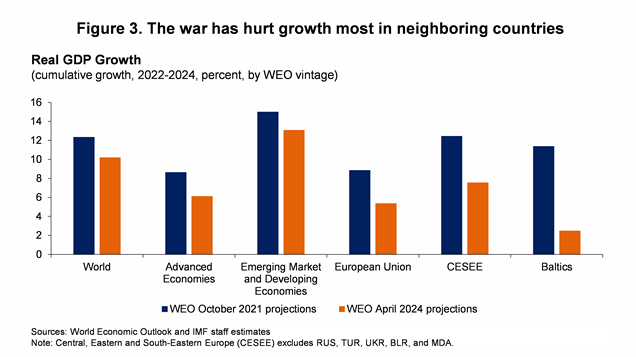

The second is on economic growth. The conflict has derailed the recovery from the COVID-19 pandemic, with the adverse effects on the terms of trade reducing consumer purchasing power, and the higher inflation forcing central banks to tighten monetary policy. Trade has also experienced a hit, especially for CESEE countries for which Russia was a major trading partner. Figure 3 corroborates how CESEE countries have experienced the biggest setbacks to their growth performance since the onset of the war, though the war has clearly had an adverse impact on a much broader set of countries.

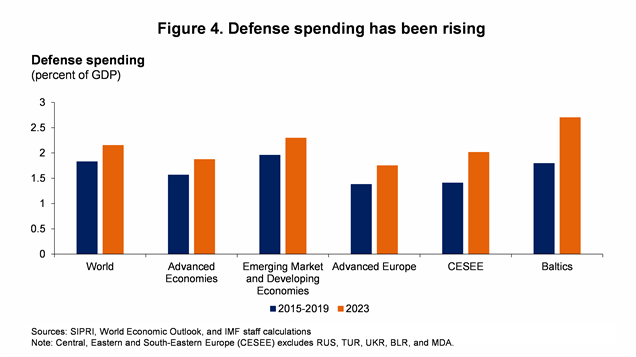

The third effect is on defense spending, which is likely to be on a permanently higher trajectory, given greatly increased national security concerns. While defense spending has increased globally, the effects have been particularly pronounced in the CESEE region, especially in the Baltics, as evident from Figure 4. Of course, the higher defense spending compounds pressures on public finances arising from the COVID-19 pandemic, green transition, and demographics, and will require difficult steps to ensure that debt remains on a sustainable path.

Turning point for geoeconomic fragmentation

The direct costs inflicted by Russia’s war in Ukraine are enormous. But it is easy to underestimate the ripple effects that the conflict is having on the geoeconomic landscape and global economy. In fact, I would argue the war in Ukraine has been a turning point for global economic fragmentation.

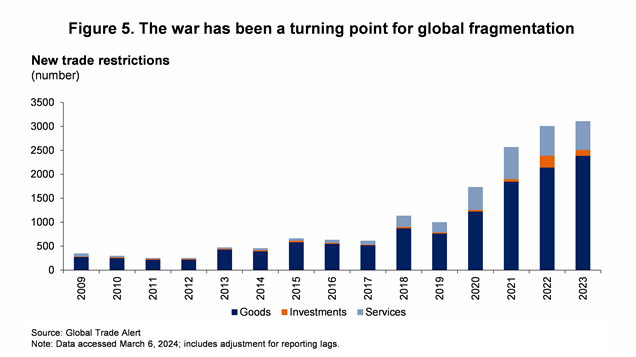

While globalization had slowed and national security and geoeconomic concerns had been on the rise before the war, Russia’s invasion of Ukraine has had a catalytic effect: geoeconomic fragmentation has accelerated and begun to force a rapid realignment away from what has been a highly efficiency-based and globalized model of trade. As Figure 5 shows, the number of new trade restrictions imposed in each of the last two years has tripled relative to 2019.

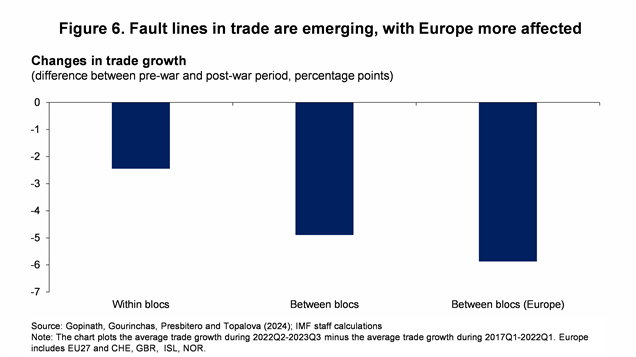

We are also seeing evidence of differences in trade flows between and across geopolitically aligned countries. While trade has declined globally since the war, it has fallen much less between groups of countries that are more aligned geopolitically than between countries that are more divergent (Figure 6), in particular for European countries;[1] and a similar pattern holds for FDI flows. Where before firms partnered up with select other firms to form tightly integrated global supply chains based mainly on logistics and costs, they now have to account for rising national-security constraints and geoeconomic uncertainties.

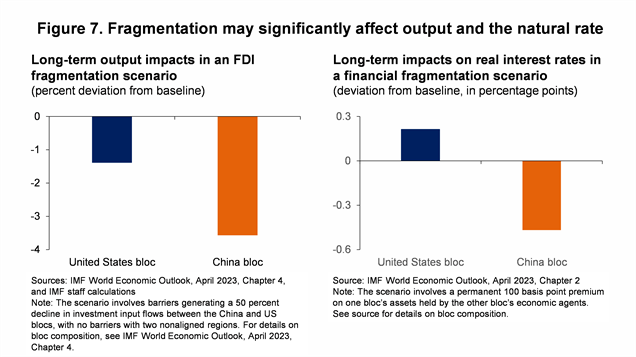

It is critical for countries and firms to build resilience. However, in the absence of sufficient guardrails, we could end up with severe fragmentation of the global economy and consequently lower productivity and income levels for everyone. For example, IMF model-based analysis taken from the April 2023 WEO (left-hand panel of Figure 7) suggests fragmentation could reduce the level of output in a bloc centered around China by over 3 percent in the long run. The scenario assumes the implementation of permanent barriers to cross-border investment flows that reduce output by depressing capital formation and weakening productivity growth.[2] In a financial fragmentation scenario, we could also see real interest rates in a U.S.-centered bloc increase due to a waning flow of savings from surplus economies in a China-centered bloc, and, conversely, some decline in real interest rates in the China bloc as they invest more of their savings domestically (right-hand panel of Figure 7).[3]

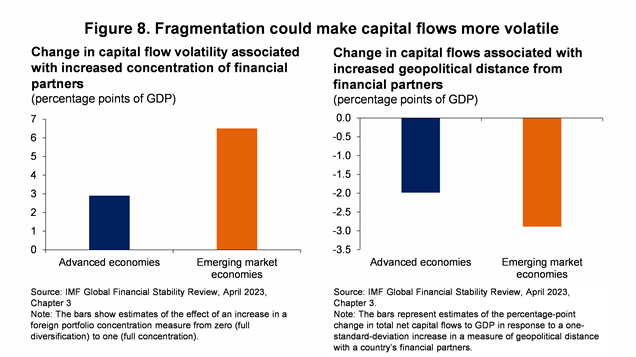

A less integrated global economy will not only be poorer, it will also be more shock-prone relative to the decades of peaceful integration. For example, when countries transact with fewer partners in financial markets, their ability to share and diversify risks weakens, leading to more volatile capital flows (left-hand panel of Figure 8).[4] This effect is especially pronounced for emerging markets, where capital flows are also more sensitive to geopolitical forces (right-hand panel of Figure 8), potentially jeopardizing their growth outlooks and convergence prospects.[5]

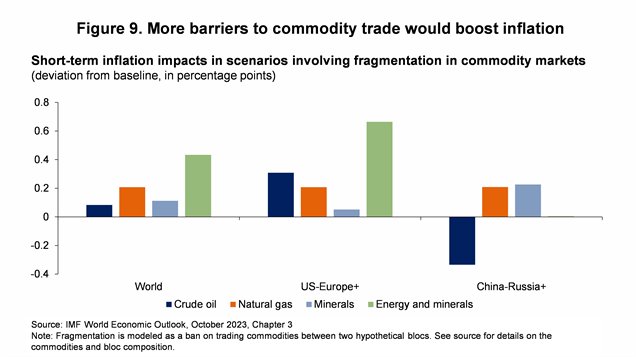

The fragmentation process could also unleash some powerful inflationary forces. For example, Figure 9 reports the inflation impacts that would occur in the first year of simulations where trade in various given commodity groups is banned between two geopolitical blocs.[6] The large impacts for some commodities and blocs partly reflect cases where importers have become highly dependent on a handful of suppliers and could therefore struggle to find substitutes in a more fragmented world. These supply-chain vulnerabilities are the legacy of decades of hyper focus on efficiencies and are also present in many other markets. While these vulnerabilities should abate as countries diversify their supply chains, the diversification process will involve price pressures of its own as those efficiencies unwind.

All told, policymakers need to get ready to navigate a more volatile world whose key features are increasingly being shaped by fragmentation and conflict.

What does this mean for economic policy, especially central banks?

Let me first consider the implications for monetary policy. A more fragmented global economy will likely mean that inflation will deviate from target by larger magnitudes than in the past, and for more prolonged periods. Insofar as much of the shock volatility is supply-driven, central banks will face more difficult tradeoffs in stabilizing employment, and hence we would expect employment to also be more volatile around potential.

Protracted periods of high inflation may also change the structure of the economy and hence affect the transmission of shocks.[7] “Intrinsic” persistence in the Phillips Curve may rise as indexation in wage- and price-setting becomes more prevalent, or because inflation expectations become dislodged. Because high inflation generates large relative price changes, it may also affect price- and wage-setting as workers demand “catch-up” for real wage losses, while firms try to make up for higher wages by raising prices further. And while the Phillips Curve appears flat below full employment, nonlinearities may become pronounced in a high-pressure, high-inflation environment.

These features could give rise to substantial upward skewness in the response of inflation to large shocks—so that the response of inflation is asymmetric—even if the underlying shocks are symmetric. Of course, given that fragmentation and conflict are typically likely to increase cost pressures, asymmetry in the shocks would also tend to amplify upside inflation risks.

On the policy side, one implication is that central banks will have to be more cautious about “looking through” supply shocks. Such shocks may have small second-round effects if inflation is near target when the shock hits, so that little policy response is required. But transmission may change substantially—with second-round effects much bigger—if inflation has already been running high and the economy is hot so that producers can more easily pass on cost hikes. In these circumstances, a more aggressive policy response would be warranted.[8]

Somewhat more broadly, the possibility of significantly higher upside inflation risks has important implications for how inflation-targeting central banks conduct monetary policy. Given that inflation targeters aim to ensure that the forecast path of inflation converges to target at a medium-run horizon, “forecast-based policy rules”—which set the policy rate based on the forecast for inflation in the medium term—have natural appeal. But insofar as such rules focus on medium-term inflation outcomes under a central forecast that represents the “most likely” path for the economy, they may lead to poor macroeconomic outcomes if uncertainties are large and asymmetric. By the same token, it is important that measures of medium- or long-term inflation expectations remain close to target, but that in of itself should not be taken as a sign that policymakers are necessarily striking an appropriate balance of risks.

To be more concrete, policymakers may expect that the shocks currently boosting inflation should dissipate quickly under their central forecast, and thus think that little policy rate adjustment will be needed to induce inflation to converge to target in the medium run. We saw many advanced economy central banks basically take this approach when inflation ratcheted up a few years back. But this strategy can be problematic if upside risks are sizeable, and can allow inflation to drift up and make the economy more vulnerable to shocks. Accordingly, a risk management strategy that takes more account of tail risks seems desirable, and preferable to focusing heavily on a central forecast. Of course, identifying, weighting, and communicating the relevant risks are challenging tasks, and ones in which central banks will have to invest heavily over the years ahead—as Bernanke (2024) and Schnabel (2024) have recently emphasized.

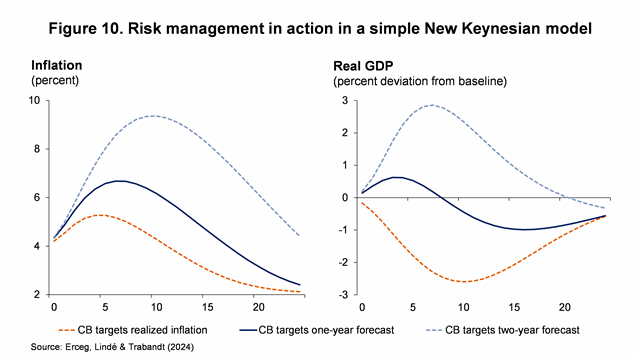

With this in mind, I’ll next illustrate the problems of a forecast-based rule in a simple New Keynesian model.[9] In the model, cost-push or “markup” shocks are used to proxy for the effects of supply shocks. The model implies that cost-push shocks have small and transient effects on inflation when inflation starts near steady state, but embeds some ingredients mentioned above to allow large shocks to generate big and persistent effects on inflation. These include a nonlinear Phillips Curve and an endogenous indexation mechanism that leads to more indexation when inflation has been running significantly above target. Critically, the persistence of the cost-push shock is unknown to policymakers, who must estimate it using the Kalman filter.

Figure 10 shows how problems arise when the central bank relies on a medium-term inflation forecast, but the shock turns out to be more persistent:[10] by the time policymakers realize their mistake, the endogenous indexation mechanism has boosted second-round effects significantly and inflation is far more difficult to control. By contrast, the orange lines in the figure focus on a situation where the central bank reacts directly to realized core inflation rather than a medium-term forecast. This helps preempt the inflation surge, albeit at some cost to output.

In practice, central banks must balance the costs of underreacting to the shock when it turns out to be persistent with those of overreacting when it in fact proves transient. While striking an appropriate balance isn’t an easy task, it is critical to ensure that inflation doesn’t drift too far from target for too long—especially for emerging markets where inflation expectations tend to be less well-anchored than in advanced economies.[11] Hence more focus on nearer-term forecasts and progress on realized inflation may be warranted in setting policy rates, while recognizing some short-run costs to output and employment.

Responding to higher capital flow volatility

For emerging markets, capital flow and exchange rates are also of key concern, and there are good reasons to expect that capital flow volatility will be higher in a more conflict-prone environment. The Fund’s Integrated Policy Framework (IPF) is helpful in identifying conditions under which FXI—and possibly inflow CFMs—may be helpful in improving the policy tradeoffs facing EM central banks.[12] Overall, the bar for FXI should be set fairly high, as allowing the exchange rate to adjust flexibly is typically desirable if FX markets are reasonably deep and financial stresses are modest. Thus, even if fragmentation results in significant terms of trade shifts, there is not necessarily a strong case for using FXI. The case for FXI is stronger if FX market depth is low and the economy faces external shocks associated with deteriorating investor sentiment and tightening financial conditions. But even in this case, the central bank must be cognizant of the intertemporal tradeoffs involved in using FXI to support the exchange rate, including the risk that it may compromise its future ability to provide liquidity support in FX. These intertemporal considerations are more salient when reserves are limited and there’s a significant risk that shocks may persist or intensify—a key risk in the case of military conflicts.

Need for supportive financial, fiscal, and structural policies

The monetary policy actions needed to contain inflation in a more shock-prone environment may also fuel financial market stress. In this environment, central banks may be fearful of taking warranted steps to tighten policy for fear of undermining the financial system (often called “financial dominance”). Hence there is a high premium on enhancing the resilience of the financial system.

This entails deepening the monitoring of financial risks, including risks that may arise from a higher-for-longer environment. Particular attention should be devoted to the sovereign-bank nexus, to risks from nonbanks, and to risks to the payments system, including from cyber. Ensuring adequate prudential buffers, possibly further building capital where profits are strong, can help by deepening resilience. And central banks and other authorities need to be ready to mitigate the risk of crisis through ensuring ELA readiness and through effective resolution strategies.

Responsible fiscal policy is also critical. An expansionary fiscal stance puts more onus on monetary policy to cool demand pressures, and sharper policy tightening can amplify financial vulnerabilities. Moreover, it may undermine the credibility of monetary policy—and make the task of central banks more difficult—by increasing concerns about fiscal dominance. Hence fiscal policy shouldn’t work at cross purposes with monetary policy. Given that defense spending and spending in areas such as refugee support may ratchet up for countries in close proximity to conflict, it is important to balance these needs by paring spending in other areas, while remaining mindful of the need to protect vulnerable populations.

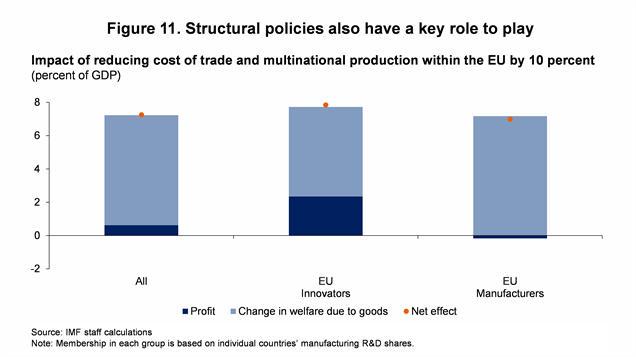

Structural reforms (Figure 11) can also help counterbalance some of the effects of fragmentation by strengthening potential output growth and increasing resilience to shocks. As we discussed earlier, larger, economically integrated regions will generally be less prone to shocks than smaller ones. A corollary of this fact for European economies not yet part of the European Union is that deepening their links with the EU will be beneficial. And for the EU itself, moving closer to a true “single market”—by lowering barriers to cross border mobility in services, goods, and labor—will add to its strength and resilience. While there has been considerable progress, mobility on certain key dimensions, especially of labor, remains far below that in the United States.

Closing remarks

Let me close by returning to the situation of our host country and their remarkable success in maintaining macro-financial stability and supporting economic activity despite the ongoing war. Are there any early lessons from Ukraine’s response to Russia’s invasion? My preliminary assessment is on four fronts.

First, Ukraine embraced the principle that macroeconomic stability goes hand in hand with its national security. To avoid an economic collapse, Ukraine made tough but quick and innovative decisions following the initial shock of the war. They implemented emergency monetary and FX policies by raising interest rates, fixing the hryvnia to the dollar and introducing FX and capital controls. They also used some monetary financing to finance the war, negotiated official and private debt standstills, and rationalized discretionary public expenditures. Core functions of the state were preserved: pensions were paid, bank branches remained open, and tax ratios remained high.

Second, almost 30 months into the war, the Ukrainian authorities have shown great agility and adaptability in their policymaking. Monetary financing has ceased; the domestic bond market has been revitalized; domestic revenue mobilization and external debt restructuring are underway; the exchange rate peg was replaced by a managed float to prevent further external imbalances; and FX controls are being cautiously eased to enable investment flows.

Third, while the first two lessons highlighted how nimble policy has helped safeguard macro-stability and support economic activity, another lesson to be drawn is the importance of coordinating monetary and fiscal policies, while maintaining institutional independence. For a shock of the magnitude that has been caused by the war in Ukraine, an aligned response across monetary and fiscal policy was and remains essential.

Fourth, the Ukrainian authorities realized very early on that fighting a war and maintaining macro-financial stability would require enormous resources. They quickly turned to external donors for assistance; a multiyear financing arrangement with the IMF anchors their macro policy, accompanied by the 4-year 50-billion euro Ukraine Facility with the EU and large contributions from the US and other partners. To sustain donor confidence, they continue to advance with difficult structural reforms to build strong institutions that will support the country’s post-war future.

Such singular focus on maintaining macro stability with policy agility and ownership combined with sustained reforms and external support have supported Ukraine through its wartime challenges, setting the stage for a robust recovery on their path to EU accession.

References

Adrian, T., Erceg, C., Kolasa, M., Lindé, J., and P. Zabczyk. 2021. “A quantitative microfounded model for the Integrated Policy Framework”. International Monetary Fund Working Paper no. 2021/292.

Baba, C., and J. Lee. 2022. “Second-round effects of oil price shocks – implications for Europe’s inflation outlook.” International Monetary Fund Working Paper no. 2022/173.

Ball, L., Leigh, D., and P. Mishra. 2022. “Understanding U.S. inflation during the COVID-19 era”. Brookings Papers on Economic Activity, fall 2022: 1—54.

Basu, S., Boz, E., Gopinath, G., Roch, F., and F. Unsal. 2023. “Integrated monetary and financial policies for small open economies”. International Monetary Fund Working Paper no. 2023/161.

Basu, S., and G. Gopinath. 2024. “An Integrated Policy Framework (IPF) diagram for international economics”. International Monetary Fund Working Paper no. 2024/038.

Beaudry, P., Carter, T.J., and A. Lahiri. 2023. “The central bank’s dilemma: look through supply shocks or control inflation expectations?” NBER working paper no. 31741.

Bernanke, B.S. 2024. Forecasting for monetary policy making and communication at the Bank of England: a review.

Brandão-Marques, L., Casiraghi, M., Gelos, G., Harrison, O., and G. Kamber. 2023. “Is high debt constraining monetary policy? Evidence from inflation expectations”. International Monetary Fund Working Paper no. 2023/143.

Brandão-Marques, L., Górnicka, L., and G. Kamber. 2023. “Exchange rate fluctuations in advanced and emerging economies: same shocks, different outcomes” in: Gelos, G., and R. Sahay (eds.), Shocks and Capital Flows: Policy Responses in a Volatile World, Washington, D.C.: International Monetary Fund.

Chen, K., Kolasa, M., Lindé, J., Wang, H., Zabczyk, P., and J. Zhou. 2023. “An estimated DSGE model for integrated policy analysis”. International Monetary Fund Working Paper no. 2023/135.

Erceg, C., Lindé, J., and M. Trabandt. 2024. “Monetary policy and inflation scares”. Forthcoming IMF working paper.

Gelos, G., and Y. Ustyugova. 2017. “Inflation responses to commodity price shocks – how and why do countries differ?” Journal of International Money and Finance 72: 28—47.

Gopinath, G., Gourinchas, P.-O., Presbitero, A.F., and P. Topalova. 2024. “Changing global linkages: a new cold war?” International Monetary Fund Working Paper no. 2024/076.

Gudmundsson, T., Jackson, C., and R. Portillo. 2024. “The shifting and steepening of Phillips curves during the pandemic recovery: international evidence and some theory”. International Monetary Fund Working Paper no. 2024/007.

Harding, M., Lindé, J., and M. Trabandt. 2023. “Understanding post-COVID inflation dynamics”. Journal of Monetary Economics 140, supplement: S101-S118.

International Monetary Fund. 2023. World Economic Outlook: A Rocky Recovery. April 2023.

International Monetary Fund. 2023b. Global Financial Stability Report: Safeguarding Financial Stability amid High Inflation and Geopolitical Risks. April 2023.

International Monetary Fund. 2023c. World Economic Outlook: Navigating Global Divergences. October 2023.

International Monetary Fund. 2023d. Integrated Policy Framework – Principles for the Use of Foreign Exchange Intervention. International Monetary Fund Policy Paper no. 2023/061.

Schnabel, I. 2024. “The future of inflation (forecast) targeting”. Keynote speech at the thirteenth conference organized by the International Research Forum on Monetary Policy, “Monetary policy challenges during uncertain times,” at the Federal Reserve Board of Governors in Washington, D.C., on April 17.

[1] See Gopinath, Gourinchas, Presbitero, and Topalova (2024).

[2] See chapter 4 in International Monetary Fund (2023).

[3] See chapter 2 in International Monetary Fund (2023).

[4] See chapter 3 in International Monetary Fund (2023b).

[5] Ibid.

[6] See chapter 3 in International Monetary Fund (2023c).

[7] For details on some of these structural changes, see Ball, Leigh, and Mishra (2022), Gelos and Ustyugova (2017), Gudmundsson, Jackson, and Portillo (2024), and Harding, Lindé, and Trabandt (2023), among others.

[8] On this point, see also Beaudry, Carter, and Lahiri (2023).

[9] For details on this model, see Erceg, Lindé, and Trabandt (2024).

[10] In the figure legend, the “one- year forecast” means that the central bank responds to the inflation forecast four quarters in the future, while the “two-year forecast” implies responding to the inflation forecast eight quarters in the future.

[11] See, among others, Baba and Lee (2022), Brandão-Marques, Casiraghi, Gelos, Harrison and Kamber (2023), and Brandão-Marques, Górnicka, and Kamber (2023).

[12] See Adrian, Erceg, Kolasa, Lindé, and Zabczyk (2021), Basu, Boz, Gopinath, Roch, and Unsal (2023), Basu, and Gopinath (2024), Chen, Kolasa, Lindé, Wang, Zabczyk, and Zhou (2023), and International Monetary Fund (2023d).

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org