Cryptocurrencies and Decentralized Finance

June 24, 2022

My remarks today will focus on the risks and opportunities presented by crypto assets in an overall context of central banking in a post-Covid world. And with the volatile crypto market continuing to make headlines these days, it makes sense to focus on some of the risks of decentralized finance, or “DeFi,” which can be amplified by the volatility. To supplement the discussion, it will be useful to include a brief recap of the recent collapse of the stablecoin TerraUSD, which provides a useful example of the underlying risks of DeFi.

Cryptocurrencies carry with them a number of specific risks, such as market risks, liquidity risks, and cyber risks. Each of these can also apply to DeFi, and I will discuss each in turn. However, DeFi also presents significant opportunities. Without the need for a central entity and the accompanying labor and operational costs, DeFi has the potential to improve financial intermediation by enhancing efficiency and stability. These positive effects could also materialize through the increased competition brought on as DeFi providers enter markets traditionally occupied by conventional financial institutions.

What are the risks?

In general, digital assets are like the traditional ones that came before them in that they are subject to market risks, where the asset may appreciate or depreciate in value depending on the prevailing conditions in the market. When it comes to DeFi, market risks reflect a heavy reliance on crypto collateral. And the high volatility of crypto asset prices can often lead to frequent (forced) liquidation of DeFi lending. Interestingly, the volume of liquidation increases not only when the crypto price drops but also when it increases sharply. Collateral shortages can occur either when the price of collateral is decreasing or when the value of borrowing is increasing.

The recent spike in liquidation was due to the collapse of TerraUSD, which affected its DeFi lending platform, known as Anchor. In May of this year, total liquidation was around $1.4 billion, but $1.3 billion of this came from Anchor. Compared to May 2021—where we witnessed over $700 million in liquidation—in this most recent round in May 2022, liquidation from other platforms was much smaller, as outstanding debt also collapsed.

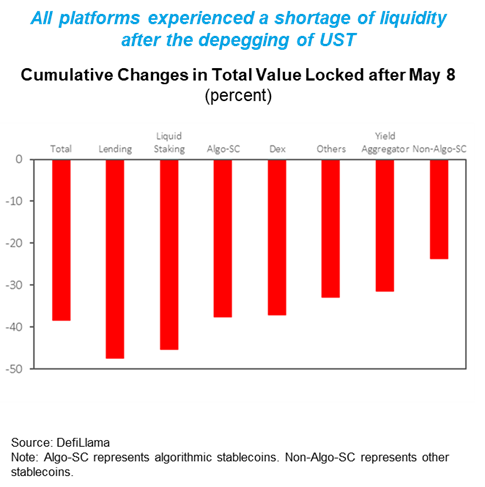

Turning now to liquidity risks, these tend to arise due to the high concentration of liquidity providers in any given segment of the market. Indeed, only a handful of accounts make up nearly half of the total liquidity of DeFi platforms.

Borrowers from DeFi platforms can repay the debt at any time. However, borrowers must always meet the collateral requirements. Suppose at any time a borrower’s collateral requirement falls below the required threshold as a result of adverse price movements. In that case, liquidation can be triggered by a liquidator who repays the debt and acquires the collateral in exchange for rewards—the liquidation bonus.

Finally, cyber risks, and in particular cyberattacks, are a critical risk for DeFi. The value of stolen crypto assets by cyberattacks increased substantially in 2021. The total value stolen in DeFi-related cyberattacks went from less than $100 million per quarter in 2020 to over $900 million in just the third quarter alone in 2021. And in most cases, over 30 percent of deposits were lost entirely—either because they were stolen by the attack or as a result of depositor withdrawals.

These attacks undermine the platform’s reputation and induce a massive amount of deposit withdrawals, which can trigger a liquidity shortage on the platform. Taken to the extreme, the effects of a serious attack can be so severe so as to shut down a platform.

New opportunities

Although DeFi has many risks, it also brings some opportunities. Chief among these, DeFi can potentially reduce costs of financial intermediation by bypassing and shortcutting the intermediation chain.

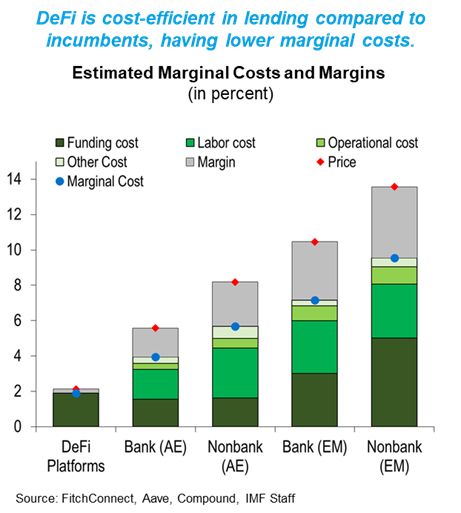

The left panel of the chart compares the estimated marginal costs of DeFi platforms and traditional financial institutions. As you can clearly see, the marginal cost of DeFi is much lower than the other banks and nonbanks in both advanced and emerging market economies, meaning DeFi is cost-efficient in lending. The low marginal costs incurred by the DeFi platforms are due to their automated and unregulated operation. Unlike traditional financial institutions, DeFi platforms do not bear labor and operational costs, because all aspects of the lending process are already automated using algorithms and interest rate models.

However, this efficiency is still subject to high vulnerabilities. As depicted in the left panel, the gray areas are margins. The margins of DeFi are very small compared to the others. DeFi charges substantially lower margins compared to the traditional financial institutions, offering favorable prices to borrowers and high deposit rates to depositors, so that they can attract borrowers and depositors, while keeping their margins low. This is in part possible because DeFi doesn’t have to maintain regulatory buffers. But such low margins also raise concerns about under-pricing risks.

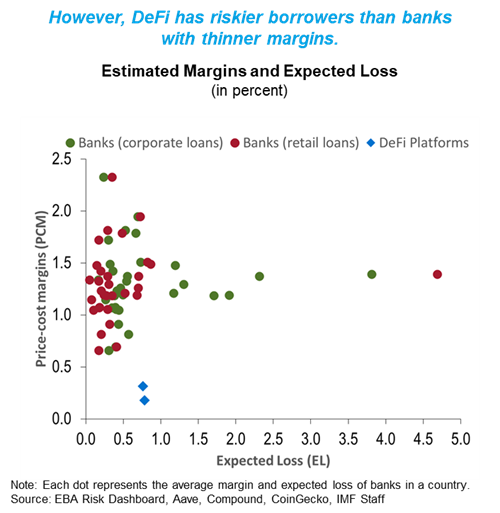

The right panel of the chart assesses margins against risk exposures. The estimated (average) expected losses of DeFi platforms are compared with those of banks. This depiction suggests that, given the same risk exposure, the DeFi margins are too low. Or, the other way round, DeFi is significantly underpricing their risks.

A paper by Igor Makarov and Antoinette Schoar on cryptocurrencies and DeFi suggests these lower marginal costs could be offset by higher upfront costs. As they state in the paper, given smart contracts do not allow for ex-post renegotiation or cancelation, the contract must be completed ex-ante. It therefore requires higher upfront costs of negotiating and specifying the precise terms of an agreement in all possible states of the world.

The collapse of TerraUSD (UST)

The aforementioned risks and vulnerabilities were proven when the third-largest stablecoin TerraUSD (UST) collapsed on May 9. Let me briefly explain what happened during the collapse and its effect on the market.

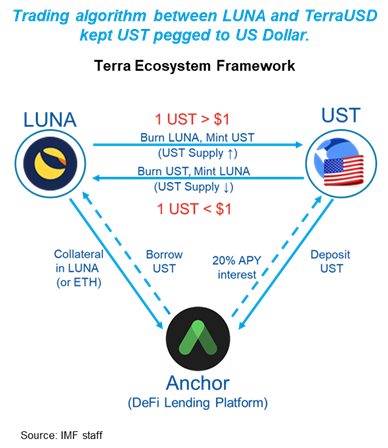

UST is an algorithm-stablecoin pegged to the US dollar. Algorithm-based stablecoins attempt to maintain a stable value via protocols that provide for the increase or decrease of the supply of the stablecoins in response to changes in demand.

However, unlike other cash or short-term asset-backed stablecoins, UST is designed to maintain its peg through arbitrage trading between UST and its sister crypto asset, LUNA, both of which are built on Terra blockchain. The protocol guarantees users the ability to trade 1 UST for $1 worth of LUNA regardless of the value of either token. The left panel of the chart depicts the nature of this relationship. When the value of 1 UST is higher than 1 US dollar, the algorithm burns $1 of LUNA and mints 1 UST, increasing the UST supply. In contrast, when the value of 1 UST is lower than $1, the UST is burned, and LUNA is minted to decrease UST supply.

If demand for UST rises and its price rises above $1 (1UST > $1), LUNA holders can bank a risk-free profit by swapping $1 of LUNA to create one UST token. Then the returned LUNA is burnt. If demand is low for UST and the price falls below $1 (1UST < $1), UST holders can exchange their UST tokens at a ratio of 1:1 for LUNA, which is worth more because of their scarcity. Then the returned UST is burnt.

The mechanism requires stable and consistent demand for LUNA and UST.

Terraform Labs, the entity running the Terra project, envisaged its plans for both crypto and real-world use cases: payment, lending, exchanges, and so on. One example is Anchor, a DeFi lending protocol, where users can deposit UST and/or borrow UST by pledging LUNA as collateral.

Anchor attracted UST deposits with the promise of 20 percent return and held close to 75 percent of UST before the fall. These unsustainably high returns were subsidized by the Luna Foundation Guard, which is an entity backstopping the Terra ecosystem by providing liquidity in case of a market crash, holding crypto assets—for example, Bitcoin, Avalanche, or others—as reserves.

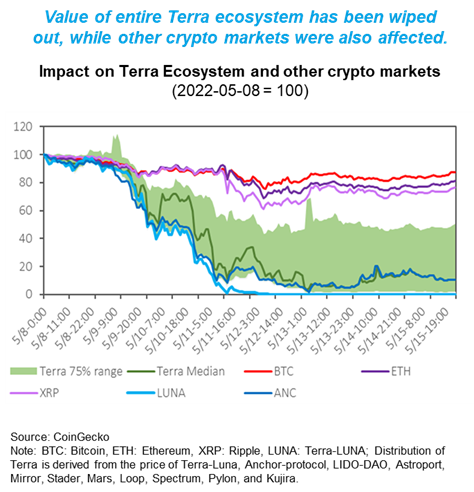

In the end, the pegging mechanism, as well as interventions by the developers, failed to defend the peg. As you can see from the right panel of the chart, UST traded at around $0.1–0.2 as of May 18, 2022, and now UST is not traded in the most major exchanges.

The collapse of UST was triggered by large withdrawals of UST from both crypto exchanges and the Anchor protocol. It is unclear why and who initiated the withdrawal, but the amount of the withdrawal was large enough to significantly de-peg the UST from 1 US dollar.

As the large withdrawals occurred, the peg stabilization mechanism kicked in (as intended) by increasing the supply of LUNA, but it put large downward pressure on LUNA’s price. In turn, the sudden plunge in LUNA’s value depleted the collateral value in Anchor, triggering the simultaneous liquidation of LUNA. UST holders, losing confidence in the peg, sold UST in a panic, and a “death spiral” collapsed the Terra system. Total value locked—that is, the value of user funds deposited in a DeFi protocol—of Anchor and other DeFi platforms in Terra blockchain dropped in parallel.

Spillovers

The collapse of UST affected not only the Terra ecosystem but also other DeFi platforms and other crypto assets. In response to the collapse of Terra ecosystem, the Luna Foundation Guard began to release its reserves to bring UST back to its 1 US dollar peg.

As shown in the left panel, the massive inflow of BTC to the market dragged down Bitcoin prices, aggravating the sell-off in crypto markets. The incident underscored the market, liquidity, and concentration risks in the market, dealing a confidence blow to the viability and stability of some crypto projects.

The failure in the Terra ecosystem caused ripple effects to the entire crypto market and weighed on risk sentiment. The massive liquidation and withdrawal from Anchor wiped out its liquidity pool almost entirely in the first three days since the onset of this event.

The right panel shows many of the other DeFi platforms also experienced large withdrawals, as already noted.

Policy recommendations

The interconnectedness among DeFi, stablecoins, and traditional financial institutions is growing. As the concerns related to crypto assets are increasing, policymakers should be proactive in their actions in order to prevent negative spillover effects in financial markets.

DeFi poses unique challenges to regulators. It is difficult to regulate anonymous entities without a centralized governance body. Compounding this, in many countries, the legal environment remains uncertain as lawmakers have yet to adequate address DeFi in regulatory legislation.

To address legal uncertainties, regulators should prepare regulatory surveillance and globally consistent regulatory frameworks. As a first step, a more indirect approach would be to address regulatory gaps in the overall crypto ecosystem. As DeFi has no centralized body, the other centralized entities in the crypto ecosystem that have enabled the development of DeFi could be the focus of regulation. For example, stablecoin issuers could be the main regulatory target, given the importance of stablecoins to DeFi. Discussion is ongoing in international standard-setting bodies—such as the Basel Committee on Banking Supervision, the Committee on Payments and Market Infrastructures, and the International Organization of Securities Commissions—regarding the regulatory framework on stablecoin issues.

The second step is to regulate key functions within DeFi directly. This approach should take the form of collaboration between regulators and private sector. Authorities should also encourage DeFi platforms to adopt robust governance and establish self-regulatory organizations. Transparent and credible governance structure can be a natural entry point for regulators.

Closing the current regulatory gaps would help to ensure that DeFi risks currently at play are minimized, while still allowing borrowers to reap the benefits these decentralized financial services have to offer.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org