Fiscal policies have provided large emergency lifelines to people and firms during the COVID-19 pandemic. They are also invaluable to increase a country’s readiness to respond to a crisis and to help with the recovery and beyond.

When the Great Lockdown finally ends, a strong economic recovery that benefits everyone will depend on improved social safety nets and broad-based fiscal support. This includes public investment in health care, infrastructure, and climate change. Countries with high debt levels will have to carefully balance short-term fiscal support for the recovery stage with long-term debt sustainability.

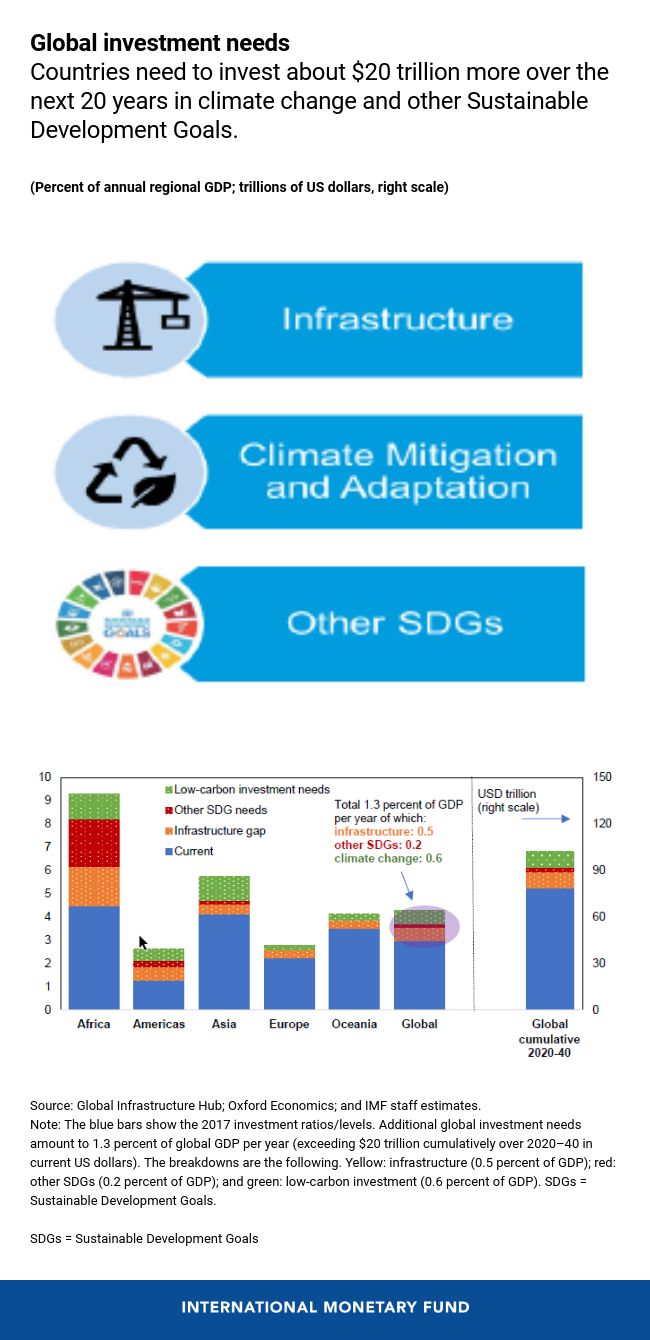

Countries need to invest $20 trillion more over the next 20 years in climate change and other SDGs.

The new Fiscal Monitor helps policymakers choose how to invest for the future in a fiscally prudent way, adopt well-planned discretionary policies to stimulate demand, and enhance social safety nets and unemployment benefits.

Enhance social safety nets for people

The pandemic has shown how vulnerable people are and served as a wakeup call for action.

In response, countries have temporarily extended unemployment benefits and expanded social safety nets to varying degrees. For example, the United States has legislated larger temporary lifelines in response to the COVID-19 pandemic than Europe partly because its social safety net has traditionally been smaller.

While some of these temporary lifelines will expire over time, making parts of these provisions permanent and upgrading the tax-benefits systems can also automatically stabilize people’s incomes in future epidemics and crises.

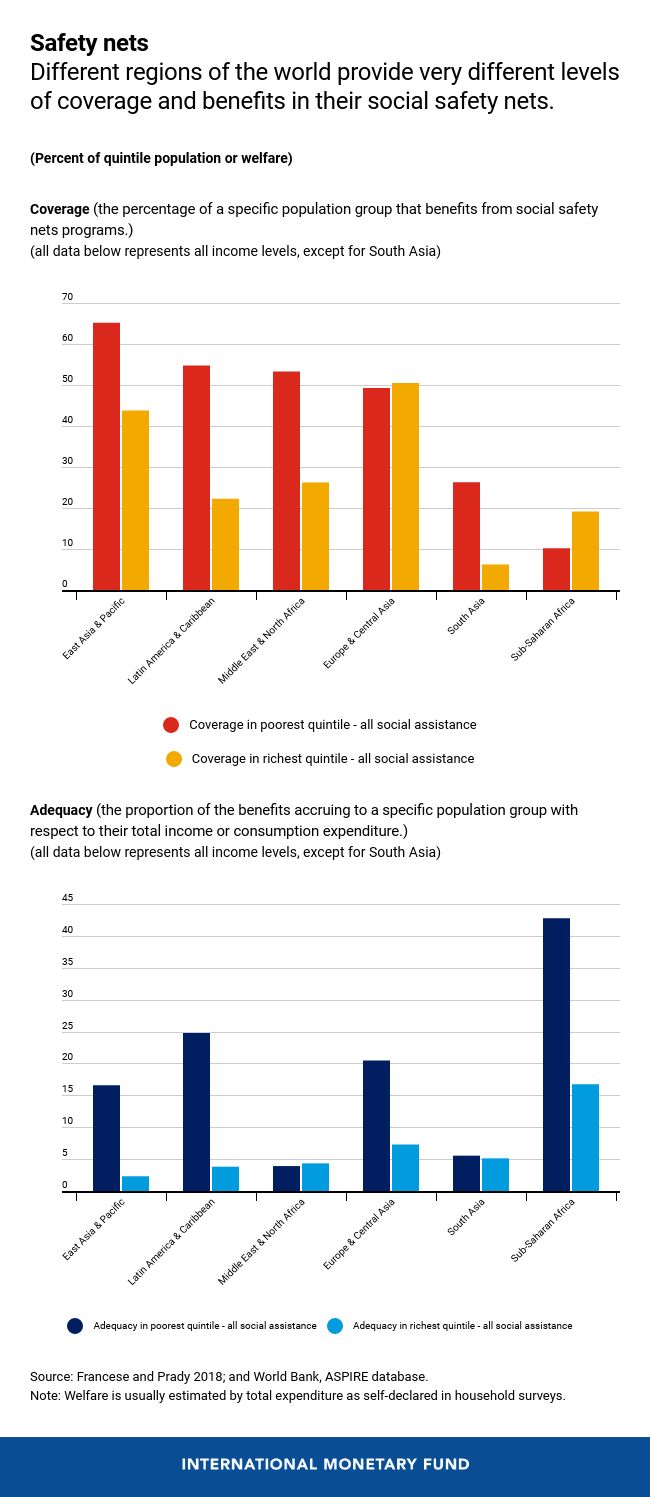

But what are the attributes of a good social safety net? Three matter the most:

- First, provide broad coverage and adequate benefits to vulnerable groups in a progressive way—that is, more generous benefits to the poorest.

- Second, preserve work incentives and help beneficiaries find jobs, obtain health care, and attend education and training.

- Third, strive to avoid a fragmented, complex web of social protection programs that ends up being more costly to run and not benefiting people in a fair and consistent way.

Against these yardsticks, governments in advanced economies can improve social safety nets by covering more people within existing programs and by improving the impact the benefits have on people’s lives.

In emerging market and developing countries, governments can fill gaps in coverage by expanding existing programs and using other delivery instruments. These include mobile phone networks and in-kind provision of goods and services—especially health, food, and transportation—to reach people most in need or currently left out.

Social safety nets could result in a better redistribution if a larger share of the poorest 20 percent of the population receive more benefits relative to the richest 20 percent of the population.

Plan discretionary policies

To help businesses rehire workers after the pandemic, governments could plan temporary payroll tax cuts to encourage firms to hire. To get people to spend, they can use time-bound value-added-tax reductions or consumption vouchers. Smaller investment projects can be accelerated. More broadly, countries can legislate in advance measures that would automatically activate in downturns, for example some social benefits and tax relief. This would get much needed fiscal support to people faster. At the same time, the scope of support depends on a country’s ability to finance these measures.

Invest for the future

Quality public investment is necessary in health care systems to protect people and minimize the risks from future epidemics. Other priorities include infrastructure, green technologies like wind and solar energy, and progress toward other Sustainable Development Goals such as education and access to clean water and sanitation. Additional investment needs are likely to exceed $20 trillion, globally at current prices, over the next two decades.

Considering the long lead time of capital projects like roads, bridges, and clean energy, governments should start now to review the investment pipeline. This will give them time to resolve bottlenecks and prepare a set of ready-to-implement projects they can deploy once the Great Lockdown ends.

Decisions, including whether and how much to scale up quality public investment, will depend on the needs in specific sectors and their economic and social benefits, financing capacity, and the efficiency of public investment. This last point is critical for all countries because one-third of funds for public infrastructure is lost worldwide to inefficiency and corruption.

For advanced economies with ample room in the budget such as Germany and the Netherlands, spending more on public investment is worthwhile because the value of the resulting assets will likely exceed the liabilities incurred given how low interest rates are. This in turn improves the public sector’s net worth. For countries with less room to maneuver when it comes to spending, such as Italy and Spain, they can redirect revenues and expenditures to increase investment.

In emerging markets and developing economies such as Brazil and South Africa, high debt levels and rising interest payments call for financing development in a prudent and sustainable way. These countries should try to achieve more with less. Raising tax revenues over the long term would be crucial for low-income developing countries such as Nigeria.

Managing higher government debt loads

Supporting the recovery with fiscal tools while managing higher government debt levels is a delicate balancing act. The pandemic and its economic fallout, along with policy responses, have contributed to a major increase in fiscal deficits and government debt ratios. As the pandemic abates and the economy recovers, government debt ratios are expected to stabilize, albeit at new—higher—levels. If the recovery takes longer than expected, debt dynamics could be more unfavorable.

As the pandemic subsides, countries can support their economic rebound with an eye on advancing credible medium-term reform plans.