(Version in Español)

Benjamin Franklin famously said these are the only things that we can be sure will happen to us. Certainly taxation has been much to the fore of public debate in the last few years. The latest Fiscal Monitor takes a close look at where tax systems now stand, and where they might, and should be headed. Can we tax better, could we—if we wanted to—raise more revenue, and how does fairness come into it?

A better way to tax

The IMF’s broad advice on the revenue side of consolidation is straightforward.

- Before raising rates, broaden bases by scaling back exemptions and special treatments, and thereby getting more people and entities to pay taxes;

- Rely more on taxing consumption rather than labor;

- Strengthen property taxes; and

- Seize opportunities to raise revenue while correcting environmental and other distortions by, not least, carbon pricing (to address climate and other pollution challenges).

How have the advanced countries done relative to this advice? Not especially well. Increases in rates of value-added tax, or VAT, for instance, have been more evident than has broadening of the tax base. Many countries have increased social contribution rates (linked to the financing of pensions and the like, but often affecting workers much like a tax). And effective carbon pricing is as remote as ever.

There are exceptions. Portugal has managed significant VAT base broadening. And thirteen or so countries have adopted bank levies of the kind that the Fund recommended back in 2010. But, overall, countries have honored the advice largely in the breach.

Taxing times

There is no “right” size of government—that varies with countries’ circumstances and social preferences. As a technical matter, however, one can ask how the revenue that a country raises compares with the revenue raised by other, similarly placed, countries. The Fiscal Monitor provides country-by-country estimates of what we call ”tax effort”—essentially, how well a country is currently doing on raising tax revenue when compared to other countries that are similar in per capita income and other characteristics. This pattern is quite complex, but the chart conveys a sense that for the advanced economies, effort is already in many cases high—a score of 1.0 on the horizontal axis means that a country is raising pretty much the most one could expect. The vertical axis represents the additional effort needed in terms of garnering enough tax revenue to help them meet half of their consolidation needs (as defined in the Fiscal Monitor). The chart also shows that several countries, including notably the United States, whose “effort” is relatively low could meet a good part of their consolidation needs by fairly modest increases.

The estimated effort in emerging markets and low-income countries (not shown in the chart) is, on average, not especially low. But there is nonetheless in many cases scope to raise more. For instance, low-income countries with “effort” below their group median could raise 3.5 points of GDP more by rising to that level.

The Fiscal Monitor also looks at how to realize this unexploited revenue potential. How much of the gap is due to poor policy versus how much is from avoidance and evasion? What we find, broadly, is that while flawed design is the predominant problem in most advanced economies, elsewhere improving compliance is the key.

The fairness factor

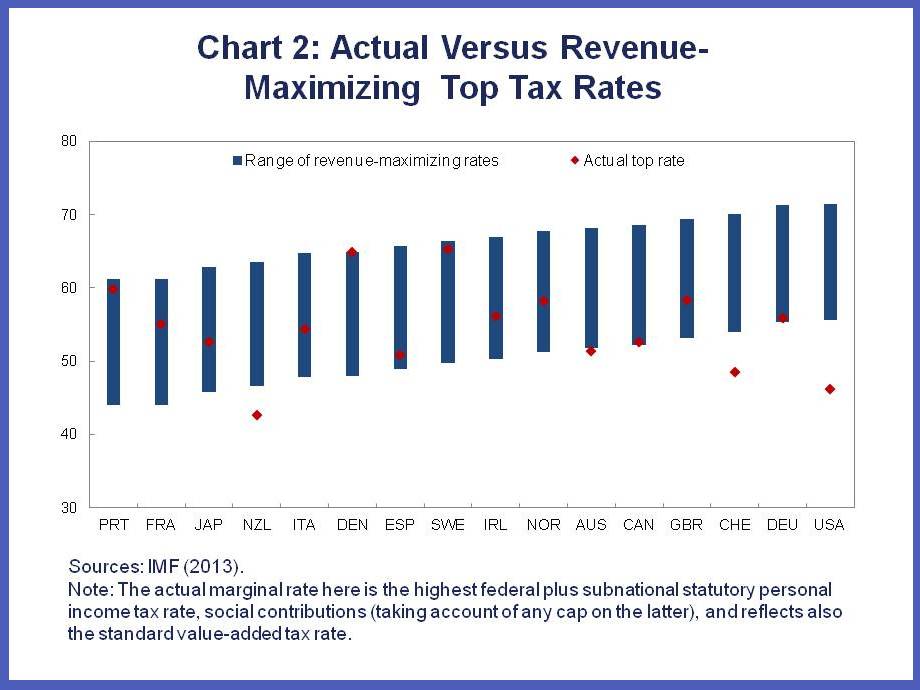

The current focus on international tax avoidance reminds us that for people to accept a tax system as legitimate, they must also see it as fair. Progressivity has fallen a lot over the last three decades or so, and inequality has increased. So we ask whether the rich could pay more. We first calculate the top rate of tax that would maximize revenue in advanced economies, putting it in a range of percentages, and compare that with what the top marginal rates now actually are (Chart 2). In many cases, current top rates are below, or to the lower end of, the estimated range of revenue-maximizing rates. Whether top rates should be raised depends on social judgments that we try to clarify in the Fiscal Monitor but ultimately leave to the reader.

Making good tax reform happen

Recent experience confirms that hard economic times are generally not good times for tax reform. While there is no silver bullet, the experiences reviewed in the Fiscal Monitor point to clear lessons. Transparency is critical, but may not be enough. Effective communication is essential—only if people are persuaded that taxes are being raised fairly and will be put to good use, will they support reform.