Londoners gather near Big Ben: the U.K. economy is doing well, but prospects of Brexit cloud the horizon (photo: Luke MacGregor/Reuters/Newscom)

Economic Health Check

Economic growth has consistently been near the top among major advanced economies, the employment rate has risen to a record high, the fiscal deficit has been reduced, and major financial sector reforms have been adopted, the report notes.

Nevertheless, there are risks to the outlook, including the possibility of a reversal in recently buoyant housing markets, a wide external current account deficit and low household saving rate, and continued slow productivity growth. The referendum on the U.K.’s continued membership in the European Union, to take place on June 23, is a major source of uncertainty.

Reflecting in part uncertainty about the upcoming referendum, economic growth slowed in the first half of this year. If the country decides to stay within the EU, growth is expected to rebound later this year and to remain steady over the next few years. Inflation should gradually rise to target after the effects of past oil and other commodity price falls dissipate and as low unemployment helps push up wages.

Risks remain

“Despite the positive overall outlook, extending growth into the medium term will depend on addressing lingering domestic and external risks,” according to Philip Gerson, Deputy Director of the IMF’s European Department and U.K. Mission Chief.

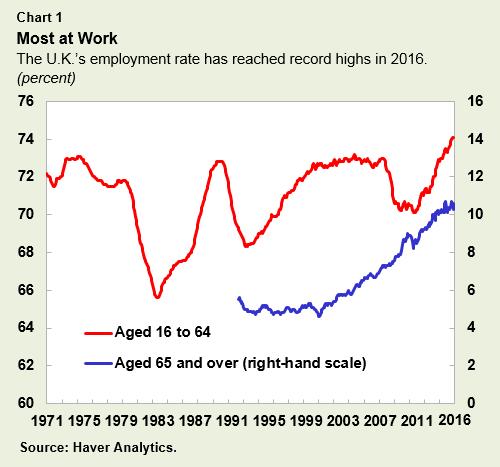

In common with many advanced economies, productivity growth has been low for several years. With employment at record highs (Chart 1) and the unemployment rate low, future income growth will increasingly depend more on boosting the amount of output per worker (that is, on higher productivity) than on increasing employment.

The U.K. also continues to struggle with a wide current account deficit. The large deficit to some extent reflects a low return on U.K. investments abroad, especially elsewhere in Europe. This should improve somewhat over time as economic conditions in other countries strengthen. In the meantime, the large current account deficit leaves the U.K. vulnerable to changes in economic sentiment that could make it more difficult to finance investment and hence slow growth.

Commercial and household real estate markets have been buoyant in recent years, and the share of new mortgages at high loan-to-income ratios has been rising. If this continues, households and banks will be more vulnerable to house price, income, and interest rate shocks.

Help growth and improve weak points

If the U.K. stays in the EU, macroeconomic policies should focus on promoting steady growth while reducing these vulnerabilities. Monetary policy should continue to support the recovery until inflationary pressures become stronger. Despite major progress since the crisis in reducing the fiscal deficit, it remains relatively high, and the government’s plan to steadily reduce the deficit and rebuild buffers is appropriate. However, government should still look for opportunities to encourage growth within the existing budget—for example by increasing spending on infrastructure, paid for through tax and pension reforms that could boost revenues or reduce outlays.

If the U.K. leaves the EU: substantial negative effect

A decision by U.K. voters to exit the EU would set off negotiations between the U.K. and the rest of the EU over the terms of its withdrawal and over the details of its future relationship with the Union. The U.K. would likewise need to renegotiate trade relationships with the 60 non-EU economies where trade is currently governed by EU agreements.

These negotiations could drag on for years, leading to a period of heightened uncertainty and risk aversion, which in turn would discourage consumption and investment and roil financial markets. In the long run, most formal assessments agree that the U.K. would be worse off economically if it were to leave the EU, as higher trade and financial barriers would lead to lower output and incomes.

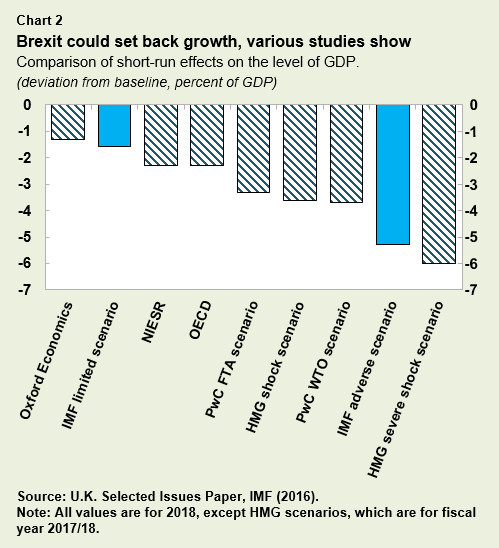

The IMF explored the potential impact of uncertainty on U.K. growth during the post-Brexit transition in two illustrative scenarios, referred to as the limited scenario and the adverse scenario (Chart 2). In both cases, the impact on output and employment could be significantly negative due to higher uncertainty. The longer this uncertainty persists, and the less advantageous the outcome of trade negotiations for the U.K., the larger are these short- and medium-run costs.

In the limited scenario in which uncertainty is relatively moderate and the U.K. is assumed to negotiate a status similar to what exists between Norway and the EU, output falls by 1.4 percent by 2019 (compared to the baseline case in which the U.K. remains in the EU). In the adverse scenario of long negotiations and a default to the trade rules of the World Trade Organization, GDP plunges by 5.6 percent by 2019 (again compared to the baseline case in which the U.K. remains in the EU), the study found.

Financial sector

In a separate, in-depth assessment of the U.K. financial sector, undertaken every five years and released along with the annual economic health check, the IMF observed that U.K. banks are well capitalized and better able to serve the economy, thanks to numerous reforms enacted to strengthen the country’s financial system in the wake of the global financial crisis.

“The United Kingdom has implemented a major wave of reforms that has re-shaped the country’s regulatory landscape since the crisis,” said Dimitri Demekas, Deputy Director in the IMF’s Monetary and Capital Markets Department, who led the IMF team of experts conducting the review. Designed to make the system more resilient and reduce the likelihood and costs of any future failures, the reforms put financial stability at the center of its new financial architecture.

The U.K. has also adopted a more rigorous, hands-on, and system-wide risk-focused approach to the supervision and oversight of the financial system. This approach was supplemented by reforms to strengthen the governance and conduct of financial firms. These reforms are key for strengthening confidence in the industry, following a series of episodes of misconduct in major U.K. financial firms.

Yet the implementation of reforms is not complete. The report said that the U.K. should complete the implementation of the post-crisis reform agenda in financial regulation and bank resolution, which it has championed globally.