Abu Dhabi, United Arab Emirates: growth in Mideast oil exporters is projected to moderate in 2013 (photo: Worldwide/Newscom)

REGIONAL ECONOMIC OUTLOOK

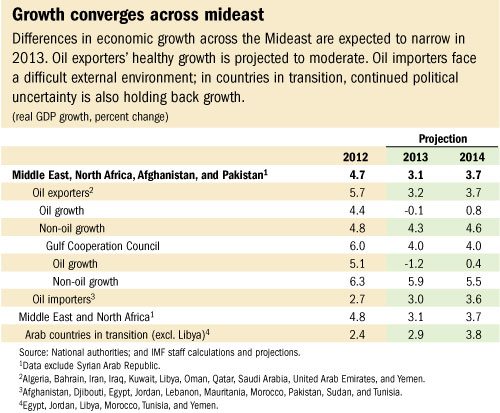

The healthy growth rates of the region’s oil exporters—Algeria, Bahrain, Iran, Iraq, Kuwait, Libya, Oman, Qatar, Saudi Arabia, the United Arab Emirates, and Yemen—are projected to moderate from an average of 5.7 percent in 2012 to 3.2 percent in 2013 (see table). This is mainly due to a scaling back of increases in oil production amid modest global demand.

By contrast, the region’s oil importers—Afghanistan, Djibouti, Egypt, Jordan, Lebanon, Mauritania, Morocco, Pakistan, Sudan, and Tunisia—face a difficult external environment. On average, this group of countries is projected to post moderate growth of 3 percent this year. In the Arab countries in transition, continued political uncertainty is also holding back growth.

“Economic conditions remain impaired across most MENA oil importers, with continued social unrest, complex political transitions, and an economic environment characterized by modest global growth, persistently high food and fuel prices, and weak domestic confidence,” IMF Middle East Department Director Masood Ahmed told a press conference in Dubai.

Oil exporters still buoyant

The region’s oil-exporting countries achieved robust growth of 5.7 percent in 2012 on account of the almost complete restoration of Libya’s oil production and strong expansions in the Gulf Cooperation Council countries. Economic growth is projected to fall to 3.2 percent in 2013, as oil production growth pauses in the context of subdued global oil demand. However, non-oil growth continues at healthy rates of about 4½ percent on average.

Elevated oil and gas export volumes and prices allowed oil exporters to accumulate current account surpluses of about US$440 billion in 2012. A small decline in projected global oil prices (based on futures markets) and an expected rise in imports will lead to a somewhat smaller—but still sizeable—current account surplus of about US$370 billion this year.

Risks to the global outlook have somewhat diminished in recent months but remain high.

Lower global economic activity, for example in the currently fast-growing emerging markets, would likely result in lower oil prices. A number of oil exporters are seeing widening non-oil fiscal deficits, making these countries more vulnerable to a prolonged drop in oil prices.

Steps to rein in spending

Fiscal break-even oil prices—the price levels that would ensure that fiscal accounts are in balance at a given level of spending—have been trending upward in most countries. In several countries, some degree of fiscal consolidation—measures to rein in spending and bring down the government deficit—will need to be considered to bring fiscal balances down to a more sustainable level.

“To build resilience to a possible sustained decrease in the oil price, oil exporters should contain increases in hard-to-reverse current government expenditures, like the wage bill and subsidies,” Ahmed said.

Effective social and capital expenditure can decrease dependence on oil revenues in the long term by promoting future growth in non-energy sectors. High-quality education can support job creation for nationals, the IMF says.

Oil importers under strain

In 2013, growth in the region’s oil importers is expected to recover, but only at a moderate pace, projected at close to 3 percent—a rate far below what is required to address these countries’ high rates of unemployment.

Investor confidence remains weak because of political uncertainty and social unrest across the Arab countries in transition and regional spillovers from the tragic conflict in Syria—including the cost of supporting refugees, disruptions to bilateral and transit trade, and heightened security concerns.

A challenging external economic environment continues to put pressure on international reserves in many oil importers. Sluggish global growth and recession in the euro area are holding back a quicker recovery in exports and tourism. Meanwhile, high global food and energy prices contribute to rising import bills.

Resolute actions needed

With high fiscal deficits and reduced international reserve buffers, many oil importers have no time to waste to embark on difficult policy choices—considerable fiscal consolidation—implemented in a growth-friendly and socially balanced way—and greater exchange rate flexibility. This should help maintain macroeconomic stability, instill confidence, preserve competitiveness, and mobilize external financing, thus putting in place important preconditions for a healthy economic recovery, the IMF says.

“Recent subsidy reforms, paired with measures to implement more targeted social protection, are making inroads into reducing fiscal and reserve pressures in some countries in the region. However, countries will need to further rationalize subsidies while at the same time putting in place better-targeted mechanisms to protect the poor,” Ahmed told reporters.

Reforms should not wait

Looking beyond the near-term challenges, it will be necessary for many countries across the region to press on with structural reforms to achieve inclusive growth and create permanent jobs, says the IMF.

“Important as it is now to focus on maintaining economic stability, it is vital not to lose sight of the fundamental medium-term challenge of modernizing and diversifying the region’s economies, creating more jobs, and providing fair and equitable opportunities for all,” Ahmed told the conference. He stressed a number of important reform areas that should not be delayed in order to unlock the region’s vast medium-term growth potential:

• Greater trade integration, both within the region and in the world economy, not only to boost growth but also as a catalyst for other important reforms.

• Business regulation and governance reforms to ensure simple, transparent, and evenhanded treatment for companies, and ultimately greater transparency and accountability of public institutions.

• Labor market and education reforms that will ensure adequate skill building and incentives for employment while maintaining adequate worker protection.

• Improving access to finance to help catalyze entrepreneurship and private investment.

• Public finance reform to help free up resources for high-priority expenditures and reduce vulnerabilities, which will also spur growth.

Ahmed underscored that, while comprehensive reform will take time, “a number of steps could be taken quickly, such as cutting back on often overlapping or discretionary regulations that complicate starting up or running a business, relaxing high minimum capital requirements and restrictions on foreign ownership, and dismantling non-tariff barriers to trade.” He added that “quick wins can also be made in the area of transparency through more consistent publication of government budgets.”

Role of the international community

In addition to providing technical assistance and policy advice to many countries in the region, the IMF has provided about $8.2 billion of financial support to Jordan, Morocco, and Yemen, and reached a staff-level agreement on a $1.75 billion loan to Tunisia last month. The global lender is also in discussions on a financial arrangement with Egypt and a second arrangement with Yemen.

Support from other international partners also remains crucial. “The international community has a vital role to play in supporting countries in transition. By providing policy and technical advice, financing, and trade access, bilateral and multilateral partners can help to support positive change,” said Ahmed.