The Debt Web

The interwar period shows how a complex network of sovereign debt can aggravate financial crises

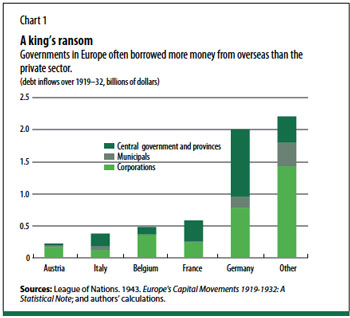

In the early 1930s, as the Great Depression took hold, the international capital flows that were critical to the functioning of the world economy dried up. The reasons are still debated: reckless behavior of speculators and banks, misguided monetary policies, and severe exchange rate misalignments are among the usual suspects. Few would argue that unsustainable fiscal policies and sovereign debt write-offs were the main reasons for the collapse of asset markets and global financial flows. Yet, in Europe in the 1920s and early 1930s, governments often received larger capital inflows than the private sector (see

Chart 1).

Using a unique new set of data compiled by the IMF that records sovereign debt at the instrument level, we took a close look at the web of debt—most of it incurred because of World War I—that linked the world’s major economies in the interwar period. We found that concerns among investors about the credibility of fiscal policies and sovereign debt service contributed to the severity and persistence of the financial disruptions associated with the Great Depression, even if they were not the trigger.

Our study of the interwar period shows how external sovereign debts can play an aggravating role in global financial cycles, especially when they represent the nodes of a complex financial web. As with the global crisis of 2008 and the euro area crisis of 2010, loss of investor confidence, sovereign debt market disruptions led by liquidity drought, and government intervention in the financial sector added to the external debt burden. Thus, the interwar period offers a telling lens not only for understanding the 2008 crisis, but also for identifying and interpreting present-day vulnerabilities.

In the years after World War I, countries faced very high levels of sovereign debt and an unforgiving macroeconomic environment. Most took steps to reduce deficits and spur growth. The United Kingdom pursued restrictive fiscal and monetary policies to bring down prices in support of the return to the gold standard at prewar parity. Austria and Germany, by contrast, initially failed to achieve fiscal and monetary reform and went down the road of hyperinflation. Italy, Japan, and to some extent, France experimented with capital controls and financial repression—government domination of banks or manipulation of money markets.

These strategies found parallels in the years following the 2008 crisis: Greece restructured its public debt, and Iceland and Cyprus adopted capital controls. Banks in Greece, Italy, Portugal, and Spain sharply increased holdings of their own governments’ debt. While such so-called home bias helps reduce government borrowing costs and provides fiscal breathing space in times of stress, it also obscures the pricing of risk, as it did during the interwar period.

Complicated networks

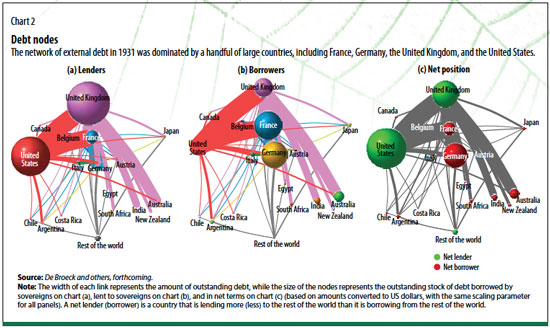

Sovereign debt interconnectedness between the wars was greater than could be inferred from net positions alone (see Chart 2). It took various forms:

Lending among allied governments and central banks during and after the war: Official external debt also included reparations imposed on Germany and some other countries. These added another layer of interconnectedness, as did attempts to make interallied debt service contingent on German reparation payments.

Sales of sovereign debt to private investors in foreign markets, which rose considerably in the 1920s: Underwriters and banks played an important marketing and risk-taking role in these issuances. For instance, JP Morgan & Co. was instrumental in floating foreign sovereign loans on the US market.

Sales of debt abroad by borrowers other than the sovereign, especially to US investors, which also grew in the 1920s: Germany encouraged external borrowing by the private sector and state and local governments to help generate foreign exchange for reparation payments.

These manifestations of interconnectedness fed into each other, rendering the global financial system vulnerable to sovereign stress. Successive rounds of multilateral and bilateral renegotiation added more links. Each agreement came with forgiveness of a sizable portion of the debt and provided refinancing for the bulk of the obligations, thereby intensifying the complexity of the network. This has important parallels with the 2008 crisis, when the buildup of public leverage—servicing debt through more debt—left the global financial system more vulnerable to shocks.

During the interwar period, many countries also had to issue foreign-currency debt abroad because they lacked well-developed financial markets at home. This left them vulnerable to the risk that the value of their debt would rise if their currency weakened, increasing the likelihood of default. The situation has parallels to examples of sudden stops in capital inflows in recent emerging market crises such as those in Argentina, Brazil, and Mexico in the 1980s and 1990s.

Contagion risks within a network are heightened when all participants are dependent on a single node, as was the case in the 1920s. Germany alone accounted for the bulk of the net exposure in the network. In the years after World War I, it became increasingly clear that Germany would be unable to service its obligations, including reparations, without some form of relief. That did not stop France, Italy, and the United Kingdom from linking their own debt service to German reparation payments.

Systemic risks

Successive rounds of negotiations to reduce Germany’s debt were based on overly optimistic economic assumptions and did not account for the possibility of a severe downturn such as the Great Depression. In other words, risks surrounding German reparations became systemic in the international financial network. Germany was too big to fail. The buildup of sovereign debt vulnerabilities came to a head when the sudden stop in international capital flows in 1931 cut off access to new funding. Some sovereigns could no longer service external debt with new borrowing and ceased payments. By 1933, they had written off a large part of their external obligations and instead came to rely on selling internal debt to domestic banks. Today, high sovereign debt and large global and regional nodes in financial networks could also transmit and amplify shocks to the system.

Common exposure to a single large debtor in the interwar period spilled over to the private sector through several channels. First, bilateral and multilateral negotiations in the 1920s involved new loans to debtor countries that were generally taken up by private investors. Consequently, the nations involved had an interest in protecting these investors against sovereign default.

Second, the central role of underwriters, both public and private, only worsened the imbroglio. Even more than today, the marketing and placement of external sovereign bonds was a delicate art. During the interwar period, governments often hired private underwriters (such as JP Morgan and Rothschild) to manage issuance and guarantee a minimum level of take-up, thereby assuming financial risk. In some cases, central and government-controlled banks acted as underwriters. France, Germany, Italy, Japan, and the United Kingdom all relied heavily on their money-issuing authorities to influence bond prices, advertise sovereign securities at home and abroad, act as underwriters, and share some risks with the government.

Third, contingent liabilities amplified the sovereign risk. Germany in the 1920s had encouraged local and state governments to borrow from private investors overseas. This became a source of moral hazard and a liability for the sovereign when local and state governments failed to pay. Austria took over a portion of the foreign liabilities of the country’s largest bank, Creditanstalt, in 1931.

These themes have parallels in the recent global financial crisis: private and public banks and sovereigns were directly or indirectly exposed to default risks stemming from governments. Intricate fiscal-financial linkages triggered questions about the best ways to reduce sovereign debt, and whether debt relief was an option.

Weak institutional arrangements

When the network unraveled in the early 1930s, the lack of an effective multilateral platform complicated the resolution of sovereign debt. The League of Nations could not act as a truly global institution, in part because the United States did not ratify the 1919 Versailles Treaty and did not participate in the newly established institution. This implied that the United States could not leverage international collaboration to handle the global fallout from the Great Depression, underscoring the dangers of having a major country withdraw from international agreements and institutions.

The absence of a global lender of last resort added to the vulnerabilities. The Bank for International Settlements lacked the tools to intervene when a country stopped paying. Set up in 1930 to help enforce external payment discipline on Germany, the bank provided emergency loans in mid-1931 but could not make long-term loans. There was also no effective international framework to prevent the slide into protectionism, uncoordinated devaluations, and trade wars in the early 1930s. The League of Nations did not have the kinds of lending facilities the IMF has today; at best, it could help design and negotiate domestic adjustment programs and coordinate guarantees for private lending granted by individual governments. As a result, prominent bankers such as Thomas Lamont and John Pierpont Morgan Jr. stepped in to fill the vacuum and informally represented the United States. Some distressed governments turned to “money doctors,” international bankers and financial advisers from the private sector, who were often unofficial emissaries of a great power. The breakdown of this arrangement in the early 1930s provides a vivid illustration of the benefits of international cooperation.

By studying the interwar period, we have seen how complex debt networks with large common exposures can heighten risks to the global financial system in the absence of effective international institutions. Immediately after World War II, new international institutions, including the IMF, and new financial support arrangements—the Marshall Plan in particular—were set up in response to shortcomings revealed during the interwar period. While there has been further progress in building institutions and regulatory systems since then, efforts to strengthen this architecture should continue lest the crises of the interwar period be repeated.

This article is part of a wider IMF project on sovereign debt in the interwar period. It relies on a data set that records sovereign debt at the instrument level, covering allied and enemy countries, as well as selected British Commonwealth members during 1913–45. The data set provides detailed time series of the amounts outstanding for the main sovereign debt instruments. The authors are collaborating with Professors Thomas J. Sargent of New York University and George Hall of Brandeis University on the project.

ART: ISTOCK / HAVANA1234

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.

Reference:

De Broeck, Mark, Nicolas End, Marina Marinkov, and Fedor Miryugin. Forthcoming working paper on interwar database and financial linkages, International Monetary Fund, Washington, DC.