Back to Basics

What Is Money?

Finance & Development, September 2012, Vol. 49, No. 3

Irena Asmundson and Ceyda Oner

Without it, modern economies could not function

Money may make the world go around, as the song says. And most people in the world probably have handled money, many of them on a daily basis. But despite its familiarity, probably few people could tell you exactly what money is, or how it works.

In short, money can be anything that can serve as a

• store of value, which means people can save it and use it later—smoothing their purchases over time;

• unit of account, that is, provide a common base for prices; or

• medium of exchange, something that people can use to buy and sell from one another.

Perhaps the easiest way to think about the role of money is to consider what would change if we did not have it.

If there were no money, we would be reduced to a barter economy. Every item someone wanted to purchase would have to be exchanged for something that person could provide. For example, a person who specialized in fixing cars and needed to trade for food would have to find a farmer with a broken car. But what if the farmer did not have anything that needed to be fixed? Or what if a farmer could only give the mechanic more eggs than the mechanic could reasonably use? Having to find specific people to trade with makes it very difficult to specialize. People might starve before they were able to find the right person with whom to barter.

But with money, you don’t need to find a particular person. You just need a market in which to sell your goods or services. In that market, you don’t barter for individual goods. Instead you exchange your goods or services for a common medium of exchange—that is, money. You can then use that money to buy what you need from others who also accept the same medium of exchange. As people become more specialized, it is easier to produce more, which leads to more demand for transactions and, hence, more demand for money.

Many monies

To put it a different way, money is something that holds its value over time, can be easily translated into prices, and is widely accepted. Many different things have been used as money over the years—among them, cowry shells, barley, peppercorns, gold, and silver.

At first, the value of money was anchored by its alternative uses, and the fact that there were replacement costs. For example, you could eat barley or use peppercorns to flavor food. The value you place on such consumption provides a floor for the value. Anyone could grow more, but it does take time, so if the barley is eaten the supply of money declines. On the other hand, many people may want strawberries and be happy to trade for them, but they make poor money because they are perishable. They are difficult to save for use next month, let alone next year, and almost impossible to use in trade with people far away. There is also the problem of divisibility—not everything of value is easily divided, and standardizing each unit is also tricky; for example, the value of a basket of strawberries measured against different items is not easy to establish and keep constant. Not only do strawberries make for bad money, most things do.

But precious metals seemed to serve all three needs: a stable unit of account, a durable store of value, and a convenient medium of exchange. They are hard to obtain. There is a finite supply of them in the world. They stand up to time well. They are easily divisible into standardized coins and do not lose value when made into smaller units. In short, their durability, limited supply, high replacement cost, and portability made precious metals more attractive as money than other goods.

Until relatively recently, gold and silver were the main currency people used. Gold and silver are heavy, though, and over time, instead of carrying the actual metal around and exchanging it for goods, people found it more convenient to deposit precious metals at banks and buy and sell using a note that claimed ownership of the gold or silver deposits. Anyone who wanted to could go to the bank and get the precious metal that backs the note. Eventually, the paper claim on the precious metal was delinked from the metal. When that link was broken, fiat money was born. Fiat money is materially worthless, but has value simply because a nation collectively agrees to ascribe a value to it. In short, money works because people believe that it will. As the means of exchange evolved, so did its source—from individuals in barter, to some sort of collective acceptance when money was barley or shells, to governments in more recent times.

Even though using standardized coins or paper bills made it easier to determine prices of goods and services, the amount of money in the system also played an important role in setting prices. For example, a wheat farmer would have at least two reasons for holding money: to use in transactions (cash in advance) and as a buffer against future needs (precautionary saving). Suppose winter is coming and the farmer wants to add to his store of money in anticipation of future expenses. If the farmer has a hard time finding people with money who want to buy wheat, he may have to accept fewer coins or bills in exchange for the grain. The result is that the price of wheat goes down because the supply of money is too tight. One reason might be that there just isn’t enough gold to mint new money. When prices as a whole go down, it is called deflation. On the other hand, if there is more money in circulation but the same level of demand for goods, the value of the money will drop. This is inflation—when it takes more money to get the same amount of goods and services (see “What Is Inflation?” in the March 2010 issue of F&D). Keeping the demand for and supply of money balanced can be tricky.

Manufacturing money

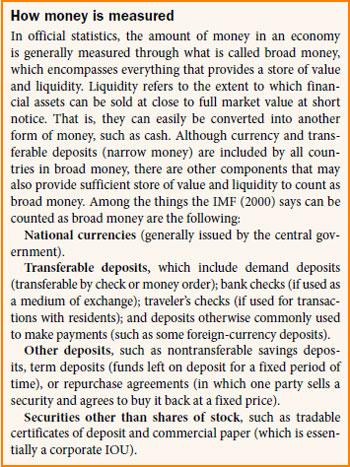

Fiat money is more efficient to use than precious metals. Adjustments to its supply do not depend on the amount of precious metal around. But that adds its own complication: Precisely because there is a finite amount of precious metals, there is a limit on the amount of notes that can be issued. If there is no gold or silver to back money, how do governments know how much to print? That gets into the dilemmas governments face. On the one hand, the authorities will always be tempted to issue money, because governments can buy more with it, hire more people, pay more wages, and increase their popularity. On the other hand, printing too much money starts to push up prices. If people start expecting that prices will continue to rise, they may increase their own prices even faster. Unless the government acts to rein in expectations, trust in money will be eroded, and it may eventually become worthless. That is what happens during hyperinflation. To remove this temptation to print money willy-nilly, most countries today have delegated the task of deciding how much money to print to independent central banks, which are charged with making the call based on their assessment of the economy’s needs and do not transfer funds to the government to finance its spending (see “What Is Monetary Policy?” in the September 2009 issue of F&D). The term “printing money” is something of a misnomer in itself. Most money today is in the form of bank deposits rather than paper currency (see box).

Belief can fade

Countries that have been down the path of high inflation experienced firsthand how the value of money essentially depends on people believing in it. In the 1980s, people in some Latin American countries, such as Argentina and Brazil, gradually lost confidence in the currency, because inflation was eroding its value so rapidly. They started using a more stable one, the U.S. dollar, as the de facto currency. This phenomenon is called unofficial, or de facto, dollarization. The government loses its monopoly on issuing money—and dollarization can be very difficult to reverse.

Some policies governments have used to restore confidence in a currency nicely highlight the “faith” part of money functioning. In Turkey, for example, the government rebased the currency, the lira, eliminating six zeros in 2005. Overnight, 1,000,000 liras became 1 lira. Brazil, on the other hand, introduced a new currency in 1994, the real. In both countries, citizens went along, demonstrating that as long as everyone accepts that a different denomination or a new currency is the norm, it simply will be. Just like fiat money. If it is accepted as money, it is money. ■

Reference

International Monetary Fund (IMF), 2000, Monetary and Financial Statistics Manual (Washington).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org