View this Issue Archive of F&D Issues Subscribe to Print Edition Write to us F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to: fanddletters@imf.org. F&D Magazine Free Email Notification Receive emails when we post new

items of interest to you. |

Priorities for regulatory reform after the meltdown The financial crisis has exposed weaknesses in the current regulatory and supervisory frameworks. The recent developments have made it clear that action is needed in at least four areas to reduce the risk of crises and address them when they occur. These are (a) finding a better way to assess systemic risk and prevent its buildup in good times; (b) improving transparency and disclosure of risks being taken by various market participants; (c) expanding the cross-institutional and cross-border scope of regulation while safeguarding constructive diversity; and (d) putting in place mechanisms for more effective, coordinated actions.

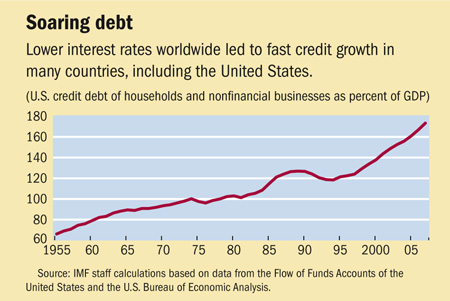

Effective regulation is needed to realize the potential of open financial markets. How to improve regulation was central to the discussion at the November G-20 Summit on Financial Markets and the World Economy. Financial innovation and integration have increased the speed and extent to which shocks are transmitted across asset classes and countries, blurring boundaries between systemic and nonsystemic institutions. But regulation and supervision have remained geared toward individual financial institutions. The regulatory mechanisms do not adequately consider the systemic and international implications of domestic institutions’ actions. This article takes a look at substantive issues in the current debates on reforming the financial sector. The first section identifies crucial weaknesses that the reforms need to address, and the second outlines key areas for policy action. What went wrong Global imbalances and housing bubbles

Innovation and structural changes Four sets of innovations and structural changes in particular have contributed to weakening risk management and rendering the system more prone to instability: the originate-to-distribute business model and reliance on wholesale funding markets; procyclical capital and accounting practices and regulations; excessive reliance on backward-looking, market-based risk management models and systems; and a more complex and opaque configuration of players. The originate-to-distribute model and wholesale funding. Securitization and the development of private-label complex structured credit instruments have undeniably improved access to credit. However, they may also have contributed to greater aggregate risk-taking and, instead of resulting in an efficient dispersion of risks, have led to a destabilizing shift of risks toward institutions that could not adequately manage them, to the reversion of some of these risks to banks that had supposedly offloaded them, and to much more uncertainty about the actual distribution of risks among market participants. In addition, both banks and the off-balance-sheet special-purpose vehicles created in the securitization process have come to rely excessively on wholesale funding markets, thus incurring maturity mismatches without adequate consideration of the risks of such funding drying up. Although the originating and arranging entities lacked appropriate credit screening and monitoring incentives, many investors failed to sufficiently question such incentives or to examine the quality of the loans underlying structured products. Instead, they relied excessively on the reputation of the institutions involved and on the credit ratings of the instruments (FSF, 2008). Credit rating agencies, in turn, assigned high ratings to complex structured subprime debt based on limited historical data; in some cases, on flawed models; and on inadequate due diligence of underlying collateral. They also failed to adequately disclose assumptions, criteria, and methodologies; clarify the meaning and risk characteristics of structured finance ratings; and address conflicts of interest (FSF, 2008). Finally, financial institutions did not always sufficiently disclose the type and magnitude of their on- and off-balance-sheet risk exposures, particularly those related to structured products. Procyclical capital requirements and accounting. During upswings, the value of marked-to-market assets and collateral increases, while loan-loss allowances decrease because default rates are expected to decline in the short run. This raises the value of reported equity and lowers the typically shortsighted probability of default estimates for both borrowers and lenders. At the same time, risk-based capital requirements can be eroded in good times because risk measures tend to ignore risk buildup during upswings. This underestimation of risks allows lenders to increase leverage and credit, which in turn reinforces asset price increases, generating a self-feeding spiral between leverage and asset prices (Adrian and Shin, 2008). Conversely, when risk measures mount during a downswing and losses materialize, capital buffers insufficiently built up in good times are eroded and cannot be easily replenished, since external capital becomes more scarce in bad times. Interactions between capital, credit, and asset markets can then magnify the intensity of the turmoil by forcing broad-based chain reactions of asset fire sales, and a self-reinforcing credit crunch and contraction of economic activity can ensue. Excessively market-based, backward-looking risk management. Too much reliance on market prices and on oversimplified, backward-looking models to manage risks, while neglecting due diligence and analysis of fundamentals, appears to have resulted in grossly underestimating risks, inducing complacency, and decreasing monitoring. Moreover, when many market participants use similar models, they may be induced to take similarly oriented market positions, thus exacerbating systemic risk. A more complex but less differentiated configuration of players. Compared with 30 years ago, the current financial system shows more blurred distinctions between different types of players, greater consolidation, many new types of players, and tighter but more opaque interconnections between them (Borio, 2007). Although these developments may have come about as a result of innovations aimed at improving the efficiency of financial intermediation, they also created opportunities for increasing leverage and for shifting risks among players in opaque ways. This made it more difficult for the market and for regulators to assess risks at any given level, while reduced diversity may have increased the likelihood of coordinated movements that could destabilize the system. Destabilizing incentives Leverage and risk. Shareholders and managers of leveraged financial institutions have incentives to increase returns upfront by taking on excessive longer-term tail risks—they can exploit information asymmetries to shift those risks to the future or to less-informed market participants. In particular, they can be driven to boost the short-run return on equity by increasing leverage, even though this raises the risk of default, as long as creditors do not price this risk into the cost of debt (for example, because of deposit insurance or lack of transparency), and as long as the shareholders’ and managers’ own exposure to downside risks is small (Dewatripont and Tirole, 1994; and Rajan, 2005). Disregard of systemic risk. In past financial crises, incentives for financial institutions to internalize systemic risk have also proven to be weak. The following are examples of behavior that can create systemic risk when many financial institutions act similarly: (a) increasing leverage during an upswing, without regard for the potential creation of unsustainable asset price bubbles; (b) replacing core deposit funding and liquid asset reserves with volatile wholesale financing and backup liquidity facilities that can suddenly dry up in a crisis; and (c) excessively increasing the supply of credit to certain sectors when interest rates are abnormally low, thereby disregarding risks to loan portfolios when interest rates eventually rebound and hit highly leveraged borrowers. Financial institutions and their managers also have incentives to follow the herd and increase risks together, because of competitive pressure to retain market shares, compensation schemes based on relative performance, or the expectation that losses from systemic risks will be socialized. Regulatory reform priorities Systemic risk and procyclical risk-taking Reassessing mark-to-market accounting. The discussion on this topic is more heated. On the one hand, maintaining adequate transparency is important. On the other, market prices tend to delink from fundamentals during both speculative booms and panic situations. Mark-to-market accounting could therefore unrealistically exaggerate procyclical swings in equity and regulatory capital, potentially contributing to financial instability, as discussed above. Transparency criteria, as well as prudential and systemic stability concerns, thus lend support to the suggestion that the effect on capital of adjustments to market values may need to be slowed down or limited—especially when market prices go up—for a range of assets beyond those held to maturity (excluding assets held for immediate liquidity). The intended dampening effect, as well as the desired transparency, may be obtained through appropriately disclosed provisions or reserves that are built up when prices rise above some threshold and drawn down as prices recede. Making securitization more compatible with incentives. Portfolio diversification is not enough to manage credit risk, and it cannot fully replace due diligence. Securitization contracts should make sure that originating and sponsoring institutions retain sufficient risks on the securitized assets, so that these institutions have an incentive to adequately screen and monitor individual loans. In addition, the Basel Committee on Banking Supervision recently (BCBS, 2008b and 2008c) issued proposals to raise capital requirements for certain complex structured credit products; to introduce additional capital charges for incremental risks in the trading book due to factors such as default, credit migration, or changes in credit spread or in equity price; and to strengthen the capital treatment of liquidity facilities to off-balance-sheet conduits. Strengthening liquidity management. An updated set of principles for sound liquidity risk management and supervision were issued by the Basel Committee in September 2008 (BCBS, 2008a), addressing weaknesses identified in the recent turmoil. The importance of maintaining adequate liquid asset buffers may need to be stressed more in the future. Reassessing risk management models and systems. Pillar 2 of the Basel II framework can be used by supervisors to strengthen risk management practices by banks, sharpen banks’ control of tail risks, and mitigate the buildup of excessive exposures and risk concentrations (Caruana and Narain, 2008). This could help ensure that risk management, capital buffers, and estimates of potential credit losses are appropriately forward looking and take account of uncertainties associated with models, valuations, concentration risks, and expected variations through the business cycle. Regulators and supervisors could work with market participants to mitigate the risks arising from perverse incentives in remuneration policies (FSF, 2008). Transparency and disclosure Securitization processes and markets. Information on securitized products and their underlying assets at each stage could be expanded. In particular, transparency by originators and issuers of securitized products about underwriting standards for, and the results of due diligence on, the underlying assets could be strengthened (FSF, 2008). Role of credit ratings Uses of ratings. Investors should not use ratings to replace strong risk analysis and management, appropriate to the complexity of the instruments they buy and the importance of their holding. In this context, supervisory authorities might consider reviewing the use of ratings in regulations, to ensure that such use does not induce uncritical reliance on credit ratings as a substitute for independent evaluation. Balancing comprehensiveness and diversity Improving cross-border information exchange and cooperation. The use of international colleges of supervisors has proved helpful in developing good practices, diagnosing large and complex financial institutions, and addressing cross-border issues. Such arrangements should be established in the short run for each of the largest global financial institutions (FSF, 2008; and G-20, 2008). Safeguarding diversity to promote systemic complementarities. The degree to which financial institutions with long-maturing liabilities (for example, pension funds and life insurance companies) should be subject to mark-to-market requirements or to risk management standards based on risk models focused on short-run price volatility in managing their assets could be reconsidered. Regulations could increase the scope for such institutions to play the role of long-term, hold-to-maturity investors. But low-leverage financial institutions with limited systemic importance may need only light, if any, regulation, thus allowing them to play a potentially stabilizing role in taking more risky or contrarian positions compared with other market participants (Nugée and Persaud, 2006). References: Adrian, Tobias, and Hyun Song Shin, 2008, “Liquidity, Monetary Policy, and Financial Cycles,” Current Issues in Economics and Finance, Vol. 14, No. 1, Federal Reserve Bank of New York (January/February). Basel Committee on Banking Supervision (BCBS), 2008a, “Principles for Sound Liquidity Risk Management and Supervision” (unpublished; Basel: Bank for International Settlements), June. ———, 2008b, “Proposed Revisions to the Basel II Market Risk Framework” (consultative document issued for comment; Basel: Bank for International Settlements), July. ———, 2008c, “Guidelines for Computing Capital for Incremental Risk in the Trading Book” (consultative document issued for comment; Basel: Bank for International Settlements), July. Borio, Claudio, 2007, “Change and Constancy in the Financial System: Implications for Financial Distress and Policy,” BIS Working Paper No. 237 (Basel: Bank for International Settlements). Caruana, Jaime, and Aditya Narain, 2008, “Banking on More Capital,” Finance & Development (June), pp. 24–28. Dewatripont, Mathias, and Jean Tirole, 1994, The Prudential Regulation of Banks (Cambridge, Massachusetts: MIT Press). Financial Stability Forum (FSF), 2008, “Report of the Financial Stability Forum on Enhancing Market and Institutional Resilience” (Basel), April 7. Group of 20 (G-20), 2008, “Declaration of the Summit on Financial Markets and the World Economy,” November 15. International Monetary Fund, 2008, Global Financial Stability Report: Containing Systemic Risks and Restoring Financial Soundness (April). International Organization of Securities Commissions (IOSCO), 2008, Code of Conduct Fundamentals for Credit Rating Agencies, revised (Madrid). Nugée, John, and Avinash Persaud, 2006, “Redesigning Regulation of Pensions and Other Financial Products,” Oxford Review of Economic Policy, Vol. 22, No. 1. Rajan, Raghuram, 2005, “Has Financial Development Made the World Riskier?” NBER Working Paper 11728 (November).

|