View this Issue Archive of F&D Issues Subscribe to Print Edition Write to us F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to: fanddletters@imf.org. F&D Magazine Free Email Notification Receive emails when we post new

items of interest to you. |

Recessions accompanied by credit crunches or asset price busts are deeper and longer lasting The financial turmoil that started in the United States has already affected the real economy in countries around the globe. But how severe the impact will be and how prolonged the resulting recession is a matter of intense debate among economists. This debate has highlighted a number of questions about the linkages between the financial sector and the real economy during recessions. For example, how do macroeconomic and financial variables behave during recessions, credit crunches, and asset (house and equity) price busts? And are recessions associated with credit crunches and asset price busts different from other recessions? To shed light on these questions, we undertook a comprehensive analysis of the linkages between key macroeconomic and financial variables around business and financial cycles for 21 Organization for Economic Cooperation and Development countries between 1960 and 2007 (Claessens, Kose, and Terrones, 2008). This is the first detailed, cross-country empirical study addressing the implications of recessions when they coincide with financial market difficulties, including credit crunches, house price busts, and equity price busts. Recessions, crunches, and busts There have been 122 recessions between 1960 and 2007. Recessions on average lasted about four quarters, with substantial variation across episodes—the shortest was 2 quarters and the longest 13 quarters (see Chart 1). The typical decline in output from its peak to its trough—the recession’s amplitude—tended to be about 2 percent. We also computed a measure of cumulative loss that combined information about both the duration and amplitude of a recession to estimate its overall cost. The cumulative loss from a recession was typically about 3 percent. Severe recessions—those in which the peak-to-trough decline in output was in the top quartile of all recession-related output declines—were more than three months longer than the average recession and much more costly.

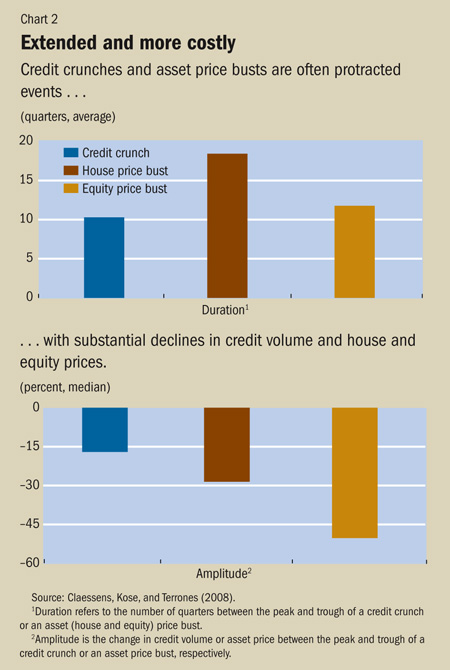

We identified 28 credit crunches, 28 house price busts, and 58 equity price busts. Credit crunches and asset price busts correspond to peak-to-trough declines in credit and asset prices that are in the top 25 percent of all episodes of credit and asset price declines, respectively. Credit crunches and housing busts are often long and deep. For example, a credit crunch episode typically lasted two and a half years and was associated with a nearly 20 percent decline in credit, which is measured by the volume of claims on the private sector (see Chart 2). A housing bust tended to last even longer—four and a half years, with a 30 percent fall in real house prices. An equity price bust lasted more than 10 quarters, and when it was over, the real value of equities had dropped by half.

If they were not followed by recessions, the episodes of crunches and busts were not necessarily associated with declines in output. In fact, although output growth slowed—especially during the early stages of credit crunches and house price busts—it often expanded at the end of these episodes. The eventual increase in output during crunches and busts is not surprising, because these episodes did not always fully overlap with recessions and lasted twice as long as the recessions. Still, the average growth rate of output during crunches and busts was much lower than during more tranquil periods in credit and housing markets. Both credit crunches and house price busts were, however, associated with significant declines in investment. Credit crunches tended to coincide with a decline in residential investment of about 6 percent, whereas house price busts were accompanied by about twice as large a drop. The unemployment rate increased significantly, especially during the early stages of these episodes, as economic activity started to soften. Cycles move in step across countries Just as many countries experience synchronized recessions, countries also go through simultaneous episodes of credit contraction. Moreover, declines in house and equity prices tend to occur at the same time. For example, house price declines are highly synchronized across countries—reflecting the importance of global financial factors, including common movements in national interest rates, in driving house price fluctuations. Equity prices exhibit the highest degree of synchronization, likely because of the high financial integration of equity markets. But the number of countries experiencing bear equity markets frequently exceeds the number experiencing a recession. As the popular saying goes, "Wall Street has predicted nine of the last five recessions." Double whammy Many recessions were indeed associated with credit crunches or asset price busts. In one out of six recessions, there was also a credit crunch under way, and in one out of four recessions a house price bust. Equity price busts overlapped for one-third of recession episodes. There can also be considerable lags between financial market disturbances and real activity. A recession, if one occurs, can start as late as four to five quarters after the onset of a credit crunch or housing bust. One of the key questions surrounding the current financial crisis is whether recessions associated with crunches and busts are worse than other recessions. Here, the international evidence is clear: these types of recessions are not only longer, but also are associated with much greater output losses than others. In particular, although recessions accompanied by severe credit crunches or house price busts last only three months longer on average, they typically result in output losses two to three times greater than recessions without such financial stresses (see Chart 3).

Why are recessions associated with crunches and busts longer and deeper? Financial market problems stemming from credit crunches and asset price busts can prolong and deepen recessions through a variety of channels. For example, sharp declines in asset prices can reduce the net worth of firms and households, limiting their capacity to borrow, invest, and spend. This in turn leads to further drops in asset prices. Banks and other financial institutions might restrict lending as their capital bases diminish during credit crunches, resulting in protracted and deeper recessions. A somewhat mechanical examination of changes in the main components of output during recessions reinforces that conclusion. Consumption and investment usually register much sharper declines, leading to more pronounced drops in overall output and employment during recessions coinciding with financial problems. For instance, the decline in consumption during recessions associated with house price busts was typically twice that of recessions without busts, likely reflecting the effects of the substantial loss of housing wealth. Moreover, the rate of unemployment typically registered a larger increase during recessions accompanied by crunches and busts. Although recessions associated with equity price busts also tended to be longer and deeper than recessions without, the differences across these episodes were not statistically significant. This confirms that equity price busts have a less tight relationship with developments in the real economy than do credit crunches and house price busts. Lessons for today Reference: Claessens, Stijn, M. Ayhan Kose, and Marco Terrones, 2008, �What Happens During Recessions, Crunches, and Busts?� IMF Working Paper 08/274 (Washington: International Monetary Fund).

|