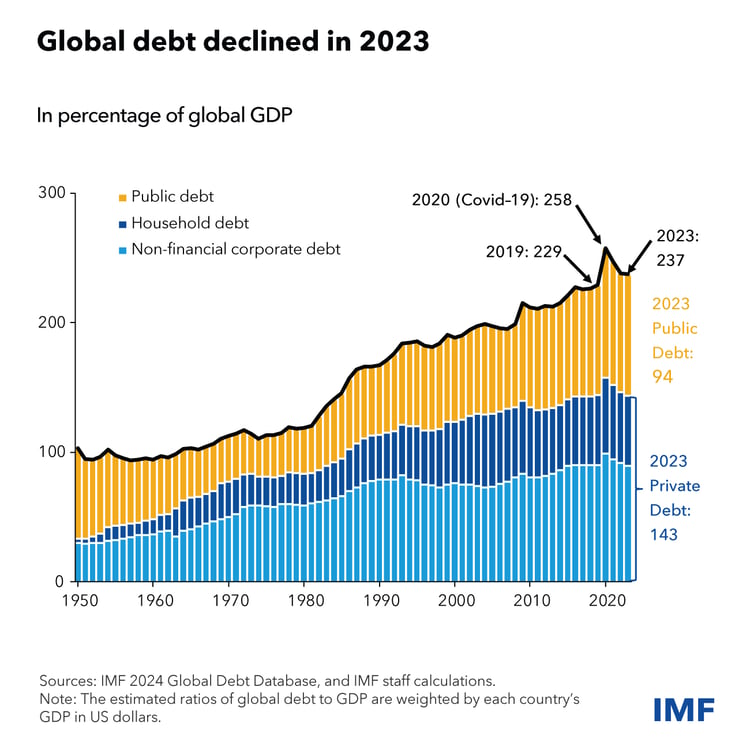

Global debt decreased about one percentage point to 237 percent GDP. The values for 2023 are now available from the just released IMF’s Global Debt Database.

Global private debt fell by 2.8 percentage points to 143 percent of GDP, below the 2019 level and more than compensated for the turning up in public debt. According to the latest Fiscal Monitor, global public debt is high, rising, and risky.

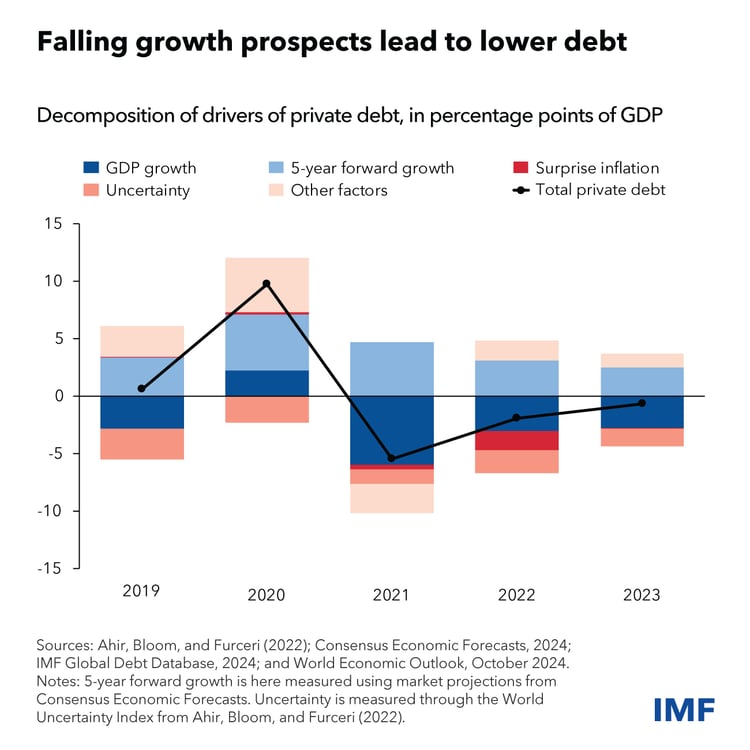

Low Growth Prospects

Empirical analysis points to low growth prospects as the main driver of the fall in private debt in 2023.

The way households and businesses react to current and expected future growth is very important for private debt. Given weak growth prospects many firms and households are opting to pay down debt. The fall in private debt slowed down compared to 2022 mainly because of a reduction in the contribution from unexpected inflation to debt erosion.

As a matter of fact, surprise inflation was a major factor in 2021-2022. Since debt is fixed in nominal terms, unexpected inflation can actually erode the real value of debt and lower its ratio to GDP. In 2022, inflation reached levels unprecedented since the Great Inflation of the 1970s and early 1980s.

A simple way to visualize the relation between private debt, growth and growth prospects is to look at the elasticity of private debt to the difference between growth prospects and current growth (see our Global Debt Monitor). As economic prospects brighten compared to the current situation, households and firms are more inclined to resort to debt financing. In recent years deteriorating growth prospects have made this logic operate in reverse.

Addressing private and public debt risks

Although declining, in 2023, non-financial corporations and household global debt is elevated at more than $150 trillion. Financial stability risks and policies to mitigate and manage them are comprehensively covered in the Global Financial Stability Report. The role of deteriorating growth prospects in the decline of private debt is a reminder of the unfortunate combination of high debt and low growth that heightens the challenge of balancing the fiscal equation. Chapter 3 of the recent World Economic Outlook emphasizes that structural policies are crucial to deliver sustainable and inclusive growth.

The launch of the 2024 Vintage of the IMF Global Debt Database

The last Fiscal Monitor argues that, in most countries, additional efforts are necessary now to contain public finance risks with a high degree of confidence. But it also argues fiscal has a central role—for example through public investment and policies that support innovation and research—among the structural policies that must be deployed to deliver enduring, sustained, and inclusive growth.

Moderator:

Chris Giles (FT)

Panelists:

Vitor Gaspar (Director, IMF Fiscal Affairs Department)

Gian Maria Milesi Ferretti (Senior Fellow, Hutchins Center on Fiscal and Monetary Policy, the Brookings Institution)

Luiz Awazu Pereira da Silva (Visiting Professor, University of Tokyo, LSE, and Sciences-Po Paris)

Ruth Yang (Managing Director and Global Head of Private Market Analytics, S&P Global)