In the European Union, income per person, one of the main gauges of living standards, is on average one-third less than in the United States, mostly because of lower productivity—as emphasized by Mario Draghi’s Sept. 9 competitiveness report for the European Commission. But what is the cause of the problem? As we show in the forthcoming Regional Economic Outlook, Europe's aggregate productivity problem can be traced back to performance differences at the firm level.

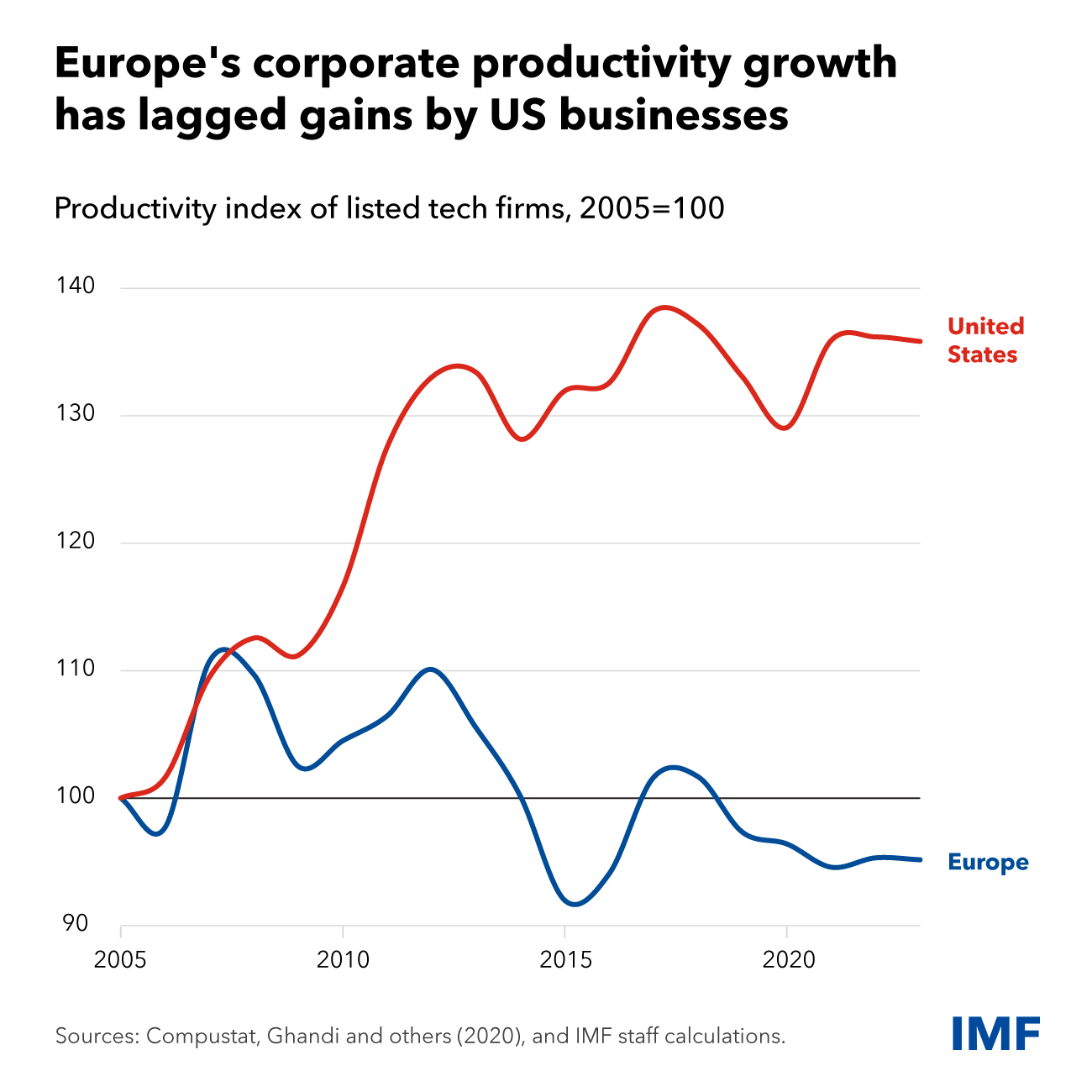

Among large, leading companies, productivity and innovation have diverged markedly across both sides of the Atlantic. Market valuations of US-listed firms have more than tripled since 2005, while Europe’s have grown by only 60 percent. While valuations can reflect expectations that end up unmet, our analysis suggests that the divergence stems also from a productivity gap across all industries and is particularly pronounced in technology sectors. Productivity for US technology firms has surged by nearly 40 percent since 2005, yet it’s little changed for European companies. This significant difference is underpinned by much greater innovation efforts among enterprises in the United States, where research and development spending as a share of sales is more than double that of Europe.

Europe also suffers from a broader lack of business dynamism beyond large corporations. There is a lower number of startups, and too few among them grow fast and eventually become large firms. In the United States, the fastest growing young companies employ six times more people (as share of total employment) than their European counterparts. With fewer successful young firms, there are also fewer large and highly productive companies later on. There is, instead, an overabundance of small and low-growth firms.

Europe’s weaker business dynamism is partly due to constraints to scaling up—particularly in innovation. Two key factors are a smaller market size and access to finance:

- Market size: While the EU and US markets are comparable in terms of purchasing-power parity gross domestic product, the EU’s is still highly fragmented. Trade intensity between EU countries is less than half the level between US states. That means a European business doesn’t benefit from economies of scale and network effects the way an American one does—which is especially harmful in tech, where scaling up quickly is critical.

- Access to finance: In the last two decades, US-listed firms have issued about twice as much equity relative to their size as their European counterparts. Equity is crucial to finance intangible investments like patents or trademarks that can’t be pledged as collateral for bank credit, and to protect these investments against short-term economic fluctuations. Funding through debt also bears higher interest rates, especially for younger businesses. Venture capital investment could help these firms, but the size of that market in the EU as a share of the economy is only around a quarter what it is in the US.

Addressing these root causes behind the underperformance of European businesses will require significant action at both the EU and domestic levels.

Deepening the European single market would lift constraints to growth for Europe’s most productive firms. Removing remaining barriers to trade within the EU and advancing the capital markets union would incentivize firms to undertake R&D and other investments that only pay off with a large customer base. For example, investing more in physical infrastructure to connect EU countries and deeper services trade liberalization can expand firms’ market access within Europe. Easing the constraints that inhibit venture capital would increase the availability of equity financing for startups and young firms. Measures include harmonizing regulations that hinder investments in larger venture funds; and having the European Investment Fund play a catalytic role by providing a quality seal, including through due diligence as a public good.

Improving business dynamism also requires strong domestic efforts that match EU-level ambitions. Easing remaining administrative barriers to entry would help more people start businesses, especially in services sectors. Facilitating the entry of new, innovative firms also calls for labor market regulations that protect workers, not jobs. This means combining more flexible layoff procedures with adequate unemployment benefits and strong active labor market policies that support job search and skill development. Tax and regulatory incentives for small firms should be made temporary to incentivize firm growth. Finally, supporting tertiary education and addressing skill mismatches are critical to foster ideas creation through new firms and technology adoption by existing businesses.

The EU must find common ground for removing barriers to goods, services, capital, and labor flows within the single market. The efforts will need to span multiple areas, opening protected sectors, lowering regulatory costs of operating across borders, expanding the capital market for innovative ventures, and investing in education. A thriving business sector is key to reducing Europe’s large productivity and income per capita gap.