Faced with high deficits and historic levels of debt, countries with limited access to financing are walking a fiscal tightrope between providing adequate support and preserving financial stability.

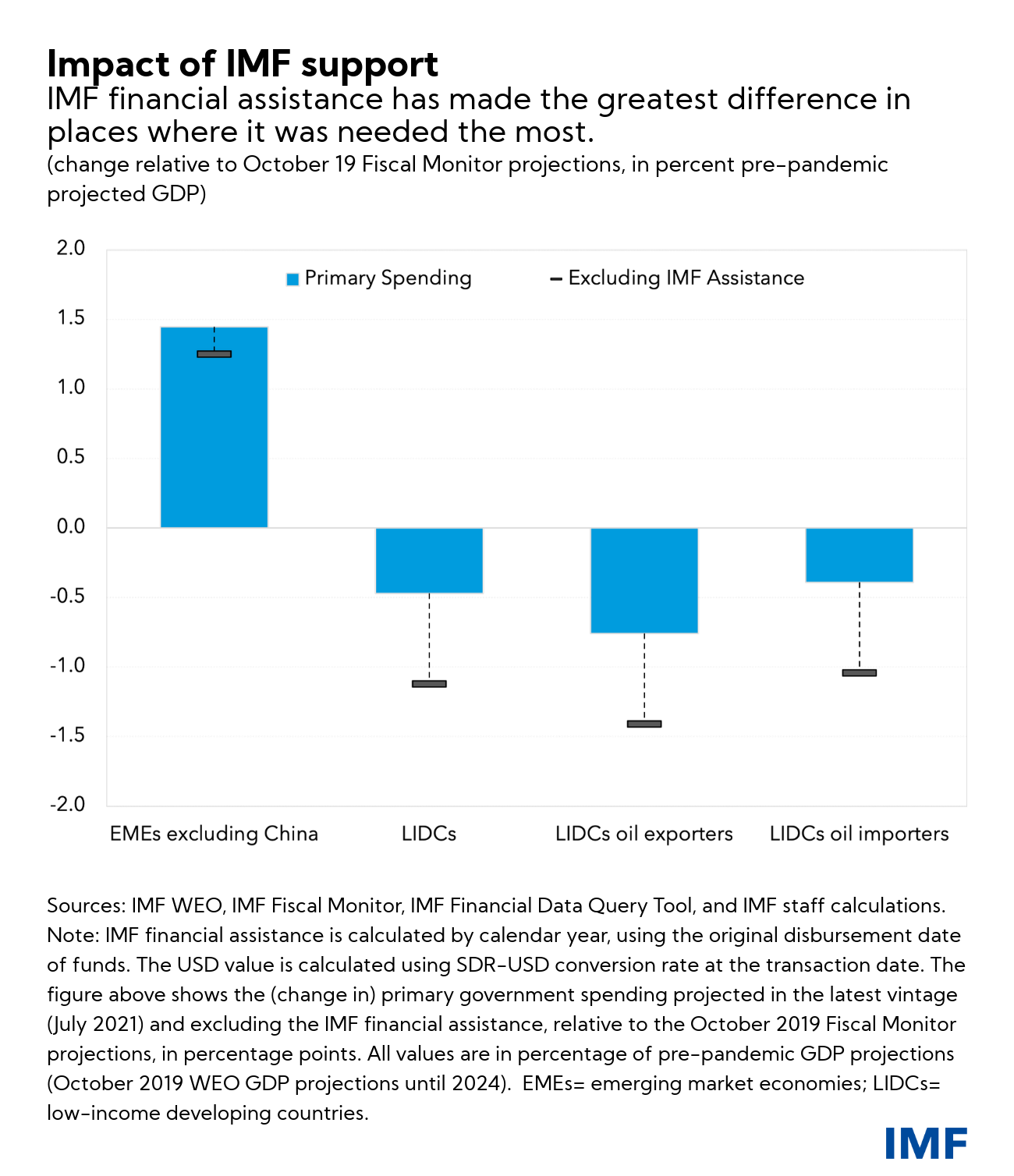

IMF support focused most where it mattered the most.

Without resolute measures to address this growing divide, COVID‑19 will continue to claim lives and destroy jobs, inflicting lasting damage to investment, productivity, and growth in the most vulnerable countries. The pandemic will further disrupt the lives of the most vulnerable, and countries will see a rise in extreme poverty and malnutrition, shattering all hope of attaining the Sustainable Development Goals.

Narrowing the pandemic divide thus requires collective action to boost access to vaccines, secure critical financing, and accelerate the transition to a greener, digital, and more inclusive world.

Securing finance

As a result of the pandemic, debt and deficits have dramatically increased from already historically high levels. Average overall fiscal deficits as a share of GDP in 2021 have reached 9.9 percent for advanced economies, 7.1 percent for emerging market economies, and 5.2 percent for low-income developing countries. Global government debt is projected to approach 99 percent of GDP by the end of 2021.

In this context, IMF lifelines have made a critical difference in saving lives and livelihoods. To respond to the crisis, the IMF has extended $117 billion in new financing and debt service relief to 85 countries. This includes financial assistance to 53 low-income countries and grant-based debt service relief to 29 of its poorest and most vulnerable members. We estimate that in 2020, IMF support allowed for additional spending of about 0.5 percent of GDP in emerging market economies and nearly 1.0 percent of GDP in developing countries. IMF support focused most where it mattered the most.

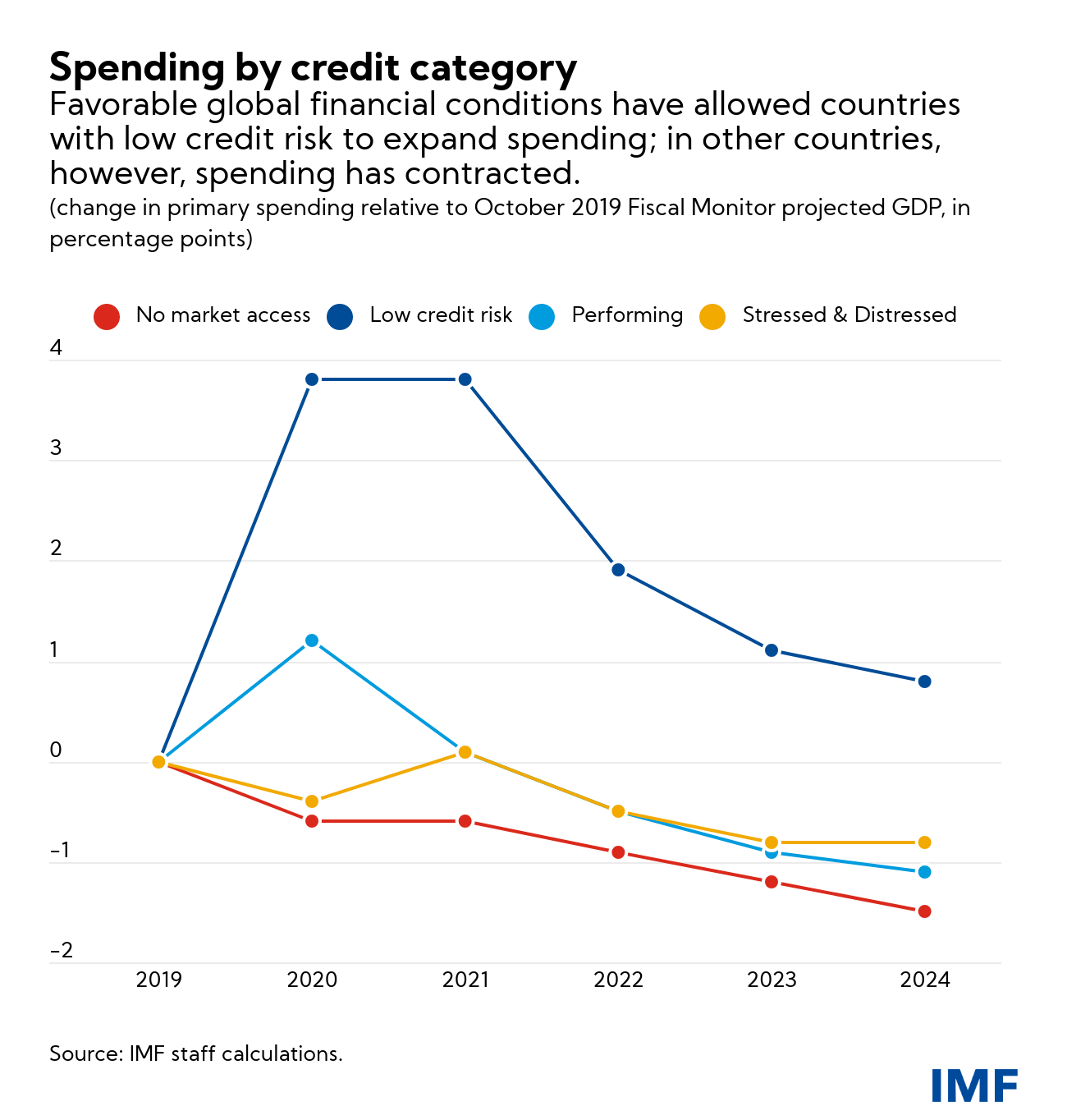

The favorable global financial conditions have allowed countries with low credit risk to deploy a sizable and durable expansion in government spending to respond to the pandemic. In those countries with more limited access to external financing, however, primary spending is now projected to be even lower than forecast before the pandemic.

A decisive moment

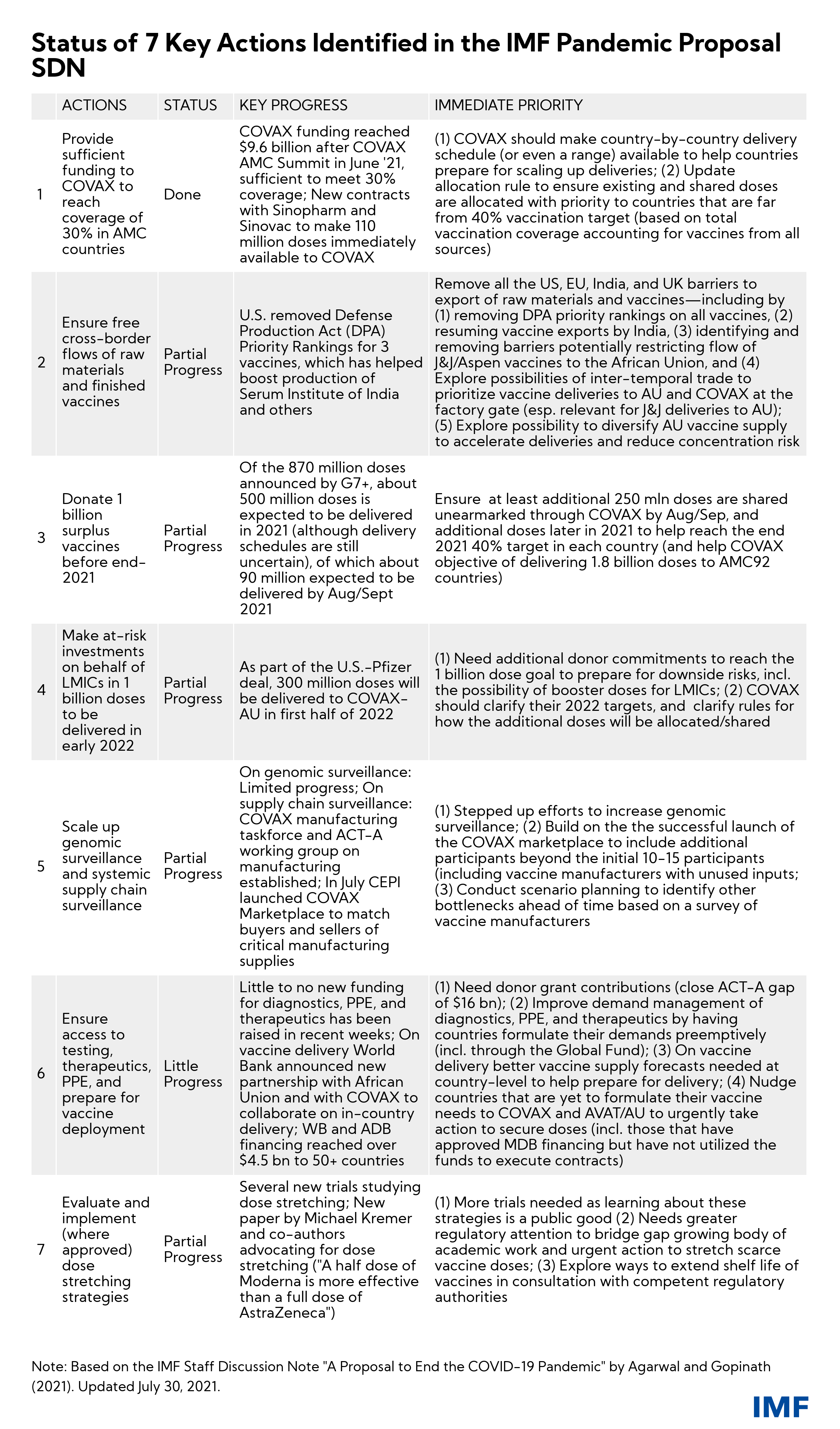

Multilateral action is urgently needed to close gaps in access to vaccines and bring about an end to the pandemic. IMF staff’s recent $50 billion proposal in this regard, endorsed by the World Health Organization, World Bank, and World Trade Organization, sets a goal of vaccinating at least 40 percent of the population in every country by the end of 2021 and at least 60 percent by mid-2022, alongside ensuring adequate diagnostics and therapeutics. Progress has been made across several fronts, but a stronger push is needed. The Taskforce on COVID-19 Vaccines has also launched a dashboard to clearly identify and urgently address gaps in access to COVID-19 tools.

Countries will also have to see how they can mobilize resources at home and increase the quality of spending. COVID-19 has aggravated the tension between large development needs and scarce public resources. To raise the much-needed revenue, governments will need to strengthen tax systems. This is especially challenging as tax competition, issues in allocation of the tax base, and aggressive tax planning techniques have put income taxation under pressure.

But raising revenue is possible, and it will have to be carried out in a way that promotes growth and favors inclusiveness. Governments should look to improve efficiency, simplify tax codes, reduce tax evasion, and increase progressivity. Strengthening state capacity to collect taxes and leveraging the role of the private sector will also be key. As long as the pandemic persists, fiscal policy needs to remain agile and responsive to the ever-evolving circumstances.

Collective actions can help narrow divides. The Next Generation European Union (NGEU) fund, of which 50 percent is grants, has been an important financing source for EU member states with limited fiscal space. Access to NGEU support and low borrowing costs are decisive factors explaining the projected lack of divergence between advanced and emerging market economies in the European Union.

The international community accordingly will have to play a major role in securing financing for the most vulnerable countries. The recently approved general allocation of $650 billion of SDRs by the IMF will provide countries with additional liquidity cushions and help them address the difficult policy trade-offs they face. The channeling of SDRs from rich nations to developing nations will further boost this support. The IMF is engaging with its members on a new facility—the Resilience and Sustainability Trust—aimed at helping emerging and developing economies meet the challenges of climate change and build resilient economies. This assistance alone will not suffice, however; other sources of donor support will also be needed.

An encouraging sign is the historic international corporate tax agreement endorsed by more than 130 countries. The agreement includes a corporate income tax rate floor of at least 15 percent. It will stop the race to the bottom in international corporate tax. It is crucial to work out the details so that the agreement helps deliver resources for crucial investments in health, education, infrastructure, and social spending in developing countries.

This promising sign shows a window of opportunity. The urgency of global challenges—COVID-19, climate change, and inclusive development—requires global action. This is a decisive moment in history. 2021 should be the year of coming together.