This is a crisis like no other. It is worse than the Global Financial Crisis, and Asia is not immune. While there is huge uncertainty about 2020 growth prospects, and even more so about the 2021 outlook, the impact of the coronavirus on the region will—across the board—be severe and unprecedented.

This is a real economic shock and requires protecting people, jobs, and industries directly.

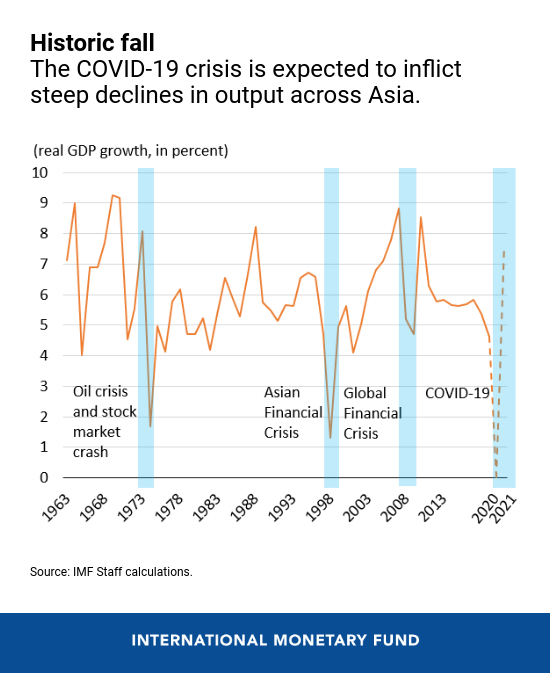

Growth in Asia is expected to stall at zero percent in 2020. This is the worst growth performance in almost 60 years, including during the Global Financial Crisis (4.7 percent) and the Asian Financial Crisis (1.3 percent). That said, Asia still looks to fare better than other regions in terms of activity.

Downward revisions are substantial, ranging from 3.5 percentage points in the case of Korea—which appears to have managed to slow the spread of the coronavirus while minimizing prolonged production shutdowns—to over 9 percentage points in the case of Australia, Thailand and New Zealand—all hit by the global tourism slowdown, and in the case of Australia by lower commodity prices. Within the region, Pacific Island countries are among the most vulnerable given the limited fiscal space, as well as comparatively underdeveloped health infrastructure.

Double slowdown

In addition to the impact from domestic containment measures and social distancing, two key factors are shaping the outlook for Asia:

-

The Global slowdown: The global economy is expected to contract in 2020 by 3 percent—the worst recession since the Great Depression. This is a synchronized contraction, a sudden global shutdown. Asia’s key trading partners are expected to contract sharply, including the United States by 6.0 percent and Europe by 6.6 percent.

-

China slowdown: China’s growth is projected to decline from 6.1 percent in 2019 to 1.2 percent 2020. This sharply contrasts with China’s growth performance during the Global Financial Crisis, which was little changed at 9.4 percent in 2009 thanks to the important fiscal stimulus of about 8 percent of GDP. We cannot expect that magnitude of stimulus this time, and China won’t help Asia’s growth as it did in 2009.

Prospects for 2021, while highly uncertain, are for strong growth. If containment measures work, and with substantial policy stimulus to reduce “scarring,” growth in Asia is expected to rebound strongly—more so than during the Global Financial Crisis. But there is no room for complacency. The region is experiencing different stages of the pandemic. China’s economy is beginning to get back to work, other economies are imposing tighter lockdowns, and some are experiencing a second wave of virus infections. Much depends on the spread of the virus and on how policies respond.

Policy priorities

This is a crisis like no other. It requires a comprehensive and coordinated policy response.

The first priority is to support and protect the health sector to contain the virus and introduce measures that slow contagion. If there is not enough space within countries’ budgets, they will need to re-prioritize other spending.

Containment measures are severely affecting economies. Targeted support to hardest-hit households and firms is needed. This is a real economic shock—unlike the Global Financial Crisis—and requires protecting people, jobs, and industries directly, not just through financial institutions.

The pandemic is also affecting financial markets and how they function. Monetary policy should be used wisely to provide ample liquidity, ease financial stress of industries and small and medium-sized enterprises, and, if necessary, relax macroprudential regulations temporarily.

External pressures need to be contained. Where needed, bilateral and multilateral swap lines and financial support from the multilateral institutions should be sought. In the absence of swap lines, foreign-exchange market interventions and capital controls may be the alternatives.

Targeted support, combined with domestic demand stimulus in a recovery, will help to reduce scarring, but it needs to reach people and smaller firms.

Asian economies have taken several initiatives in this direction with direct support for health sectors, direct fiscal stimulus packages—which in some advanced Asian economies are substantially bigger than the response during the Global Financial Crisis. And many economies have put in place measures aimed at helping small and medium-sized enterprises.

Central banks across the region have moved to provide ample liquidity, cut interest rates and some have used quantitative easing. For example, the Bank of Japan has expanded its repurchase operations, coordinated with other central banks around the world in efforts to ensure smooth functioning of the market, and introduced measures to facilitate corporate financing.

But additional actions may be needed for emerging-market Asian economies that have limited space for increased spending in their budgets. If the situation deteriorates, many emerging economies may to be forced to adopt a “whatever it takes” approach, despite their budget constraints and non-internationalized currencies. In many cases, they will face policy trade-offs.

For example, central bankers are considering buying government bonds in the primary market to support critical financial lifelines to smaller firms and households to avoid mass layoffs and defaults. An alternative to direct monetization could be to use the central bank’s balance sheet more flexibly and aggressively to support bank lending to small and medium-sized enterprises through risk-sharing with the government. In doing so, there can be a role for temporary outflow capital controls to help ensure stability in the face of large capital flows, balance sheet mismatches, and limited scope to use other policy tools.

IMF support

Since the outbreak of COVID-19, we are in continuous contact with the authorities in the region to offer advice and assistance. The Fund has several tools at its disposal to help its members surmount this crisis and limit its human and economic cost, and more than 15 countries from across the region have expressed interest in our two emergency financing instruments—the Rapid Credit Facility and the Rapid Financing Instrument. A Short-term Liquidity Line has also been established as part of the Fund’s global financial safety net; it provides a backstop for member countries with very strong policies and fundamentals in need of short-term moderate balance of payments support.