Version in Español (Spanish)

Borrowing and saving in foreign currencies—so-called dollarization—seem like a rational response by citizens in some emerging market economies to financial crises and runaway inflation. But dollarization usually persists many years after the problems that triggered it are alleviated and limits the effect that central banks can have on economic activity and inflation.

As a result, many countries have tried to slowly wean their economies off dollar use (see Chart 1). Letting the exchange rate change according to market conditions would help a de-dollarization effort by making it as risky to save as it is to borrow in dollars rather than in the domestic currency.

The recent sharp terms-of-trade shock faced by many dollarized emerging markets has added urgency to the issue. The marked decline in export prices has put depreciation pressures on the currencies of commodity producers. Currency depreciation creates winners (such as households with savings in foreign currencies) and losers (such as corporates and households that borrow in foreign currencies because repayments in dollars cost more). As a result, the probability of loan defaults rises as do risks to the financial sector.

The question policymakers in highly dollarized economies must confront is whether to allow their exchange rate to adjust fully to the shock of lower commodity prices and expose the financial sector to these negative balance-sheet effects, or to curb exchange-rate flexibility, even if it hinders de-dollarization.

In our study, we look at data for 33 emerging-market economies from 1997 to 2015 and find that greater exchange-rate flexibility reduces incentives to lend in dollars.

Effect of exchange rate flexibility on dollarization

Our research on the effect of exchange rate flexibility on dollarization reveals the following:

First, the exchange rate had moved more in countries that subsequently experienced a significant reduction in dollar loans (measured as a reduction of loan dollarization of at least 20 percentage points over the sample period, to below 20 percent).

Second, statistical estimates confirm that more exchange-rate flexibility causes more rapid de-dollarization. These estimates hold even after controlling for the differential in domestic and foreign interest rates, the macroeconomic framework in individual countries (such as whether the country is an inflation targeter), measures of external volatility, the amount of inflation volatility, and other measures of domestic risks. The analysis also suggests that restoring (nearly) full exchange-rate flexibility—and, along with it, the risks of lending and borrowing in foreign currency—would provide incentives to save and borrow in local currency.

Our results suggest that policymakers should allow the exchange rate to adjust fully when facing external shocks if they want to reduce dollarization and gain greater control of monetary policy. However, the question remains of how to manage risks from mismatched balance sheets—that is, corporations and households who borrow in dollars but whose income is in the now depreciated local currency.

A look at Peru

Peru—a commodity producer—is a good case study. Following the hyperinflation of the late 1980s and early 1990s, which led to dollarization levels of around 90 percent, Peru embarked upon serious macroeconomic reforms. A new fiscal responsibility law helped keep deficits and debt low, while an inflation-targeting regime, adopted in 2002, bolstered confidence in the local currency. As a result, Peru’s inflation rate, averaging 2¾ percent annually since 2002, is among the lowest in Latin America.

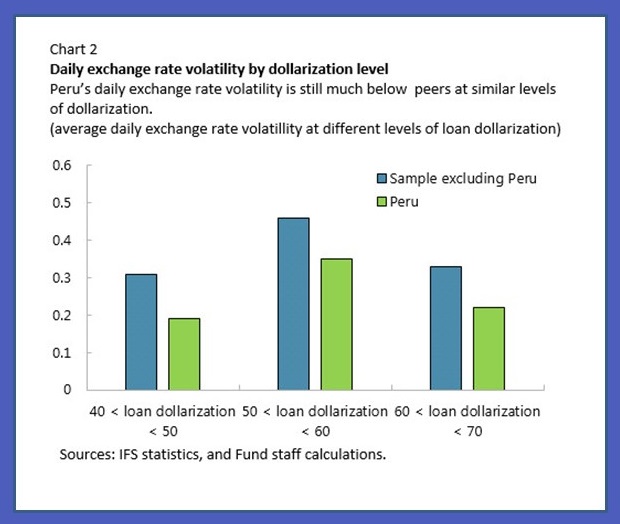

The economic house was put in order and dollarization receded, but it remained at around 40 percent in 2014. At this level, dollarization still kept the banking system potentially vulnerable to exchange rate movements. Indeed, to support a strategy of limiting financial risks from dollarization, the central bank curbed exchange rate volatility for many years—a decision that could have limited the extent of de-dollarization in the country (see Chart 2).

However, recently Peru has put in place macroprudential measures (i.e. measures aimed at overall financial stability rather than the health of individual institutions) to address financial stability risks, while at the same time triggering more rapid de-dollarization.

Among the de-dollarization measures, the Peruvian government made it more expensive for banks to lend in foreign currencies—taxing foreign exchange lending, imposing stricter requirements (such as more stringent loan-to-value ratios) on foreign currency loans, and making it less profitable for banks to accept foreign currency deposits by increasing the percentage of those deposits banks must maintain with the central bank (that is higher reserve requirements). Moreover, since 2013, the Peruvian government has set explicit de-dollarization targets and raised the costs of dollar lending in banks that failed to comply with them.

These strong incentives for lower lending in U.S. dollar clashed with incentives to keep savings in dollars, as the central bank leaned against fundamental pressures for further currency depreciation. With dollar deposits surpassing dollar loans, the central bank has been offering currency repos (buying dollars with soles, Peru’s domestic currency, with a promise to reverse the transaction at a set date in the future). This provides banks the soles they need for local currency lending. As a result of these prudential measures, loan dollarization has declined from 40 percent in 2014 to about 29 percent in recent months without a credit crunch, which supported the growth recovery following the 2014 economic slowdown.

While continuing to keep one eye on financial stability risks, our research suggests that further exchange-rate flexibility would bring Peru’s dollarization further down and help to keep it low, while possibly alleviating the need for accompanying macro-prudential measures to deal with balance-sheet mismatches—a message that also applies to several other emerging market countries.