The global financial crisis reminded us that banks often take risks that are excessive from society’s point of view and can damage the economy. In part, this is the result of the incentives embedded in compensation practices and of inadequate monitoring by stakeholders. Our analysis found the right policies could reduce banks risky behavior.

Our findings

In our latest Global Financial Stability Report we take stock of recent developments in executive pay, corporate governance, and bank risk taking, and conduct a novel empirical analysis.

Using a sample of 830 banks from 72 countries, several definitions of risk, and four different empirical methods we found that when banks align their compensation practices with long-term performance (for example, by paying bonuses with restricted stock), they also show lower levels of risk taking.

Policies to make banks safer

Recently, President Obama urged top regulators in the United States “to consider additional ways to prevent excessive risk-taking across the financial system, including as they continue to work on compensation rules and capital standards.”

Our analysis supports some of the policy measures currently being implemented in that area, and recommends new ones.

First, banks should better align compensation with risk. Banks could link compensation better to their overall financial health by paying managers partly with long-term bank bonds. Tying compensation to the bank’s default risk that way may help prevent managers and shareholders making risky bets when banks are financially weak.

Second, banks should make sure variable compensation becomes available to executives only with a lag. They should also include clawback provisions that would force managers to return past bonuses if, for example, their decisions cause losses over the longer term.

Third, the boards of directors of banks need to be independent of bank management and should establish risk committees.

Finally, policymakers should consider measures to ensure that boards effectively represent not only the interests of shareholders but also those of the creditors of the bank. For instance, they could consider granting board representation to certain types of bond holders. This could improve the ability of these creditors to monitor bank managers.

Measures can have an impact

How much can these types of measures contribute to prudent risk taking by banks and foster financial stability? Apparently quite a lot.

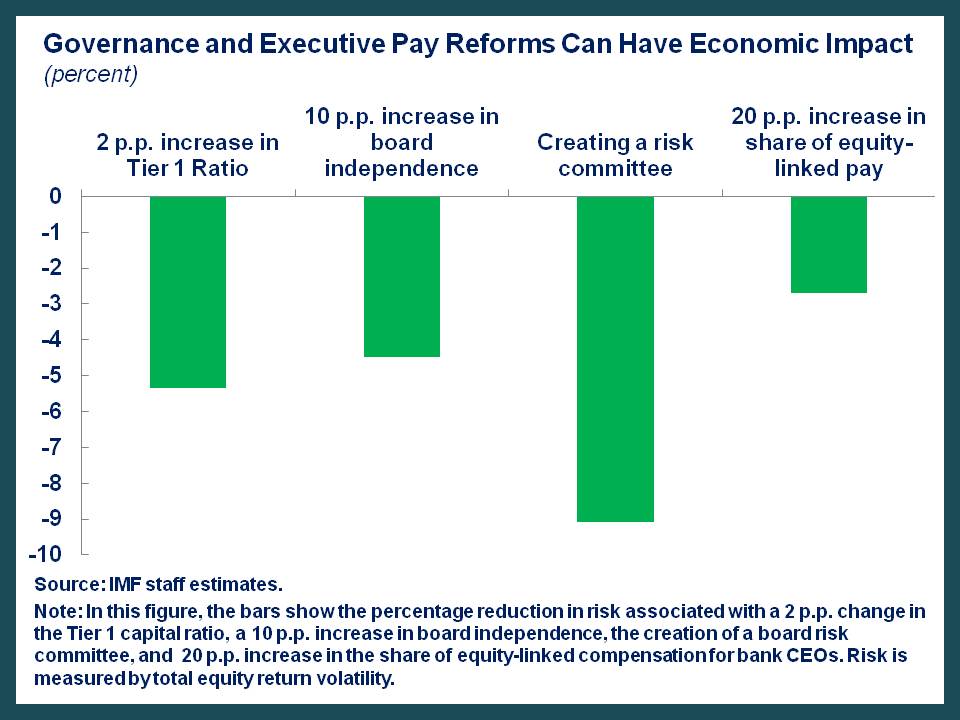

Policymakers so far have required increases in bank capital to make the financial system safer, and this has indeed had the effect of reducing the amount of risk that banks are willing to take.

Our data show that an increase in the Tier 1 Capital (the predominant form of regulatory capital under Basel III) of 2 percentage points generally leads to a decrease in risk taking of about 5 percent.

We then compare this decrease in risk with that which would result from the changes in governance structures and compensation practices that we propose. Our figure below shows that the associated risk changes are of similar magnitude. Still, we should keep in mind that capital requirements and improvements to governance and compensation practices should be seen as complements, not substitutes, and are best implemented together.

We are not done yet

We also found evidence that a bank’s risk culture matters. According to our study, banks where the CEO has a professional background in retail banking or risk management—where the risk culture is usually seen as more conservative—also show lower levels or risk. Figure 3.5 in the report shows this in more detail. The opposite is true for banks where the CEO comes from investment banking (where risk taking is more ingrained), even after controlling for bank specialization and other firm-level characteristics.

It is therefore important that bank supervisors complement their evaluation of the risk management function with a qualitative evaluation of a bank’s culture.

For instance, supervisors may inquire whether managers are setting the right “tone at the top” and whether this tone actually trickles down to the rest of organization. Does the organization reward responsible behavior? Does the staff understand the core values of the bank and are employees (including senior management) held accountable?

However, while we know that risk culture matters, we still do not fully understand why and how exactly. Academics and policymakers should make it a priority to find out.