(Versions in Español and Português)

Latin America continues to be one of the fastest growing regions in the world, even though growth slowed down a bit in 2012. Many economies in the region are operating at or near potential, inflation remains generally low, and unemployment is at historically low levels.

In the near term, the region will continue to benefit from easy external financing and relatively high commodity prices. In our May 2013 Regional Economic Outlook, we project that the region will expand by about 3½ percent in 2013. In Brazil—the region’s largest economy—economic activity is strengthening, driven by improving external demand, measures to boost investment, and the impact of earlier policy easing. In the rest of Latin America, output growth is expected to remain near potential.

Since 2003, Latin America has experienced a period of resurgence, with strong growth, low inflation, and improved social outcomes (see Chart 1). Prudent macroeconomic policies and important structural reforms have been the cornerstone of this performance. However, except for the period immediately following the 2008 global financial crisis, exceptionally benign external conditions also have been an important factor. Foreign financing has been cheap and abundant, and there has been a large and persistent increase in the prices of the region’s commodity exports.

Since 2003, Latin America has experienced a period of resurgence, with strong growth, low inflation, and improved social outcomes (see Chart 1). Prudent macroeconomic policies and important structural reforms have been the cornerstone of this performance. However, except for the period immediately following the 2008 global financial crisis, exceptionally benign external conditions also have been an important factor. Foreign financing has been cheap and abundant, and there has been a large and persistent increase in the prices of the region’s commodity exports.

However, even gold can lose its luster. These blissful external conditions will not last forever. Commodity prices are projected to stay flat or decline somewhat in the coming years, and interest rates will eventually rise as growth in the advanced economies returns.

The key challenge for policymakers in the region is to adjust policies to preserve macroeconomic and financial stability, and build strong foundations for sustained growth in the future, under possibly less favorable external conditions. In the rest of this piece, I will look at the way Latin America has managed the good times of the past decade, and discuss how it can best meet future challenges.

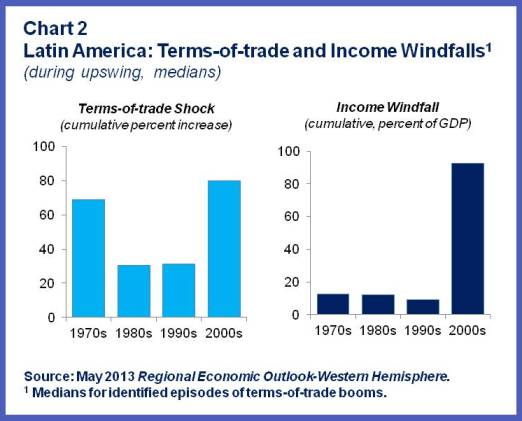

Managing the windfall

The income windfall from persistently high commodity prices over the past decade has been unprecedented. The windfall averaged 15 percent of domestic income on an annual basis, and close to 90 percent on a cumulative basis (see Chart 2). This good fortune has spurred rapid growth and has made possible a substantial improvement in government and external balance sheets. However, efforts to save the windfall have eroded since the 2008 global crisis. In many countries, public debt at end-2012 remains above pre-crisis levels and fiscal balances are much weaker.

The income windfall from persistently high commodity prices over the past decade has been unprecedented. The windfall averaged 15 percent of domestic income on an annual basis, and close to 90 percent on a cumulative basis (see Chart 2). This good fortune has spurred rapid growth and has made possible a substantial improvement in government and external balance sheets. However, efforts to save the windfall have eroded since the 2008 global crisis. In many countries, public debt at end-2012 remains above pre-crisis levels and fiscal balances are much weaker.

Looking forward, it would be prudent to increase fiscal savings, so that the economies are in better shape to manage the likely fading of the external tailwinds. Fiscal consolidation will also help to alleviate pressures on capacity and help narrow the external current account deficits.

Higher capital inflows

Easy monetary conditions in advanced economies and stronger fundamentals in the region have fueled large private capital inflows. Net capital flows to the financially integrated economies in Latin America have more than doubled from an average of below 2 percent of GDP during 2005–07 to about 4 percent in 2010–12, with the increase explained mainly by higher net portfolio flows (see Chart 3).

Easy monetary conditions in advanced economies and stronger fundamentals in the region have fueled large private capital inflows. Net capital flows to the financially integrated economies in Latin America have more than doubled from an average of below 2 percent of GDP during 2005–07 to about 4 percent in 2010–12, with the increase explained mainly by higher net portfolio flows (see Chart 3).

Preventing these inflows from generating financial excesses remains a key policy challenge. Bank credit continues to grow at a relatively fast pace, and asset prices have increased significantly (including housing prices in key metropolitan areas). These developments call for tighter fiscal policy. In addition, exchange rate flexibility should be used to discourage speculative flows, while faster reserve accumulation could be considered in cases where currencies are on the strong side of the range consistent with fundamentals. Prudential measures, such as tighter loan-to-value ratios, higher capital requirements, and limits on sectoral exposure, could also be deployed to prevent a buildup of financial vulnerabilities.

Sustaining high growth

From a supply perspective, Latin America’s growth over the last decade continued to be driven by increases in physical capital and labor. Productivity growth also picked up, contrary to the trends of past decades, but remains well below that recorded in other fast growing regions. During 2003–12, labor and capital accumulation contributed 3¾ percentage points to Latin America’s annual GDP growth, while total factor productivity contributed around ¾ percentage points.

With labor participation at historically high levels and very low unemployment rates, future growth would have to rely increasingly on productivity gains. Boosting productivity is not an easy task and countries need to tailor measures to the circumstances of each country. Policies that would be conducive to this outcome include higher investment in infrastructure and human capital, more modern legal frameworks, and more efficient and competitive product and labor markets. In the near term, it would be important for policymakers to calibrate macroeconomic policies based on a realistic assessment of the supply potential of the economy.

The key challenge for Latin America is to take advantage of the still favorable external conditions to anchor its progress in the last decade and lay the foundations for sustainable growth. This entails strengthening fiscal positions further, prudent management of capital flows to avoid financial excesses, and pressing ahead with structural reforms to increase productivity and potential growth.