Even before the latest euro area GDP numbers and Italian elections cast a shadow over the continent, economists were struggling to reconcile the steady improvement in market sentiment with the more downbeat data on the economy, production, orders, and jobs.

This video looks at this puzzle from a somewhat different perspective than the usual—and still correct—narrative of weak banks and over-indebted public sectors caught in a vicious cycle. More specifically, we examine the role of household and corporate balance sheets in the countries under financial market stress and the implications for policy priorities.

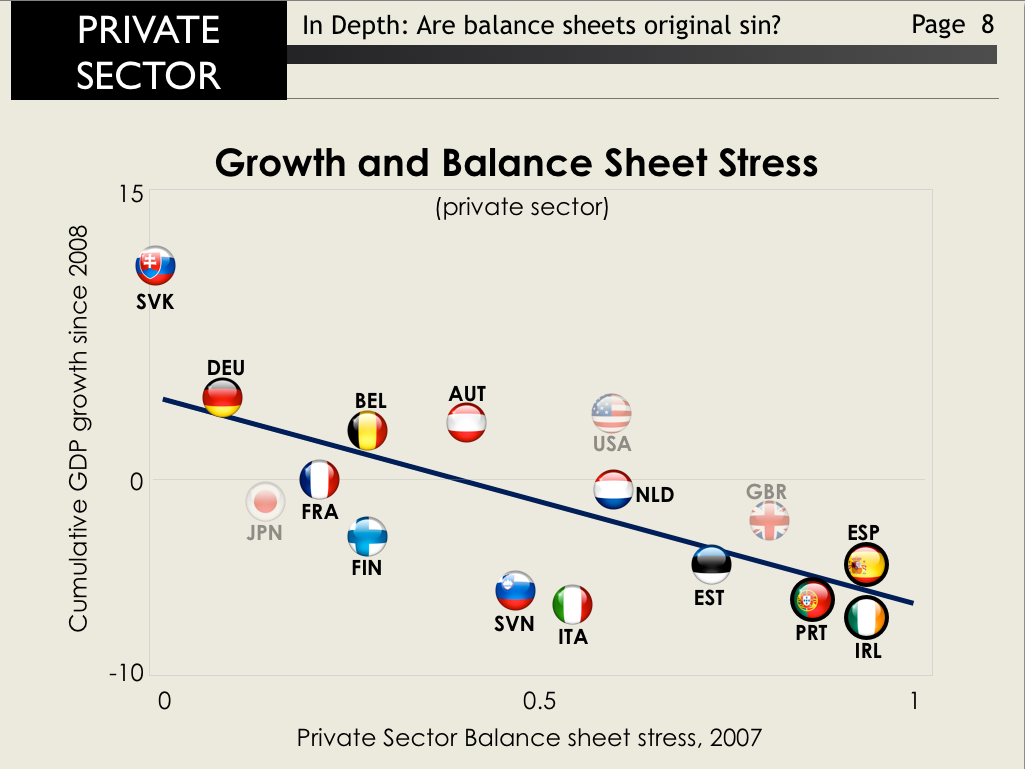

Some countries in the euro area do not just suffer from over-extended government and bank balance sheets, but also from over-extended household and corporate balance sheets. While the type of stress (household, corporate, or bank) differs from country to country, it is sufficiently large to be a potential drag on domestic demand. The negative relationship between pre-crisis indebtedness and post crisis growth—in incomes, consumption, and investment— is striking.

The downdraft on growth from corporate and household balance sheet problems is likely to be with us for some time. Obviously this affects the financial situation of governments and banks, worsening the interdependence between flagging growth, public finances, and banking health. This has resulted in lending rates that are still too high in countries such as Spain and Italy, despite strong efforts from the European Central Bank. As this chart makes clear, the transmission of easy monetary policy remains impaired.

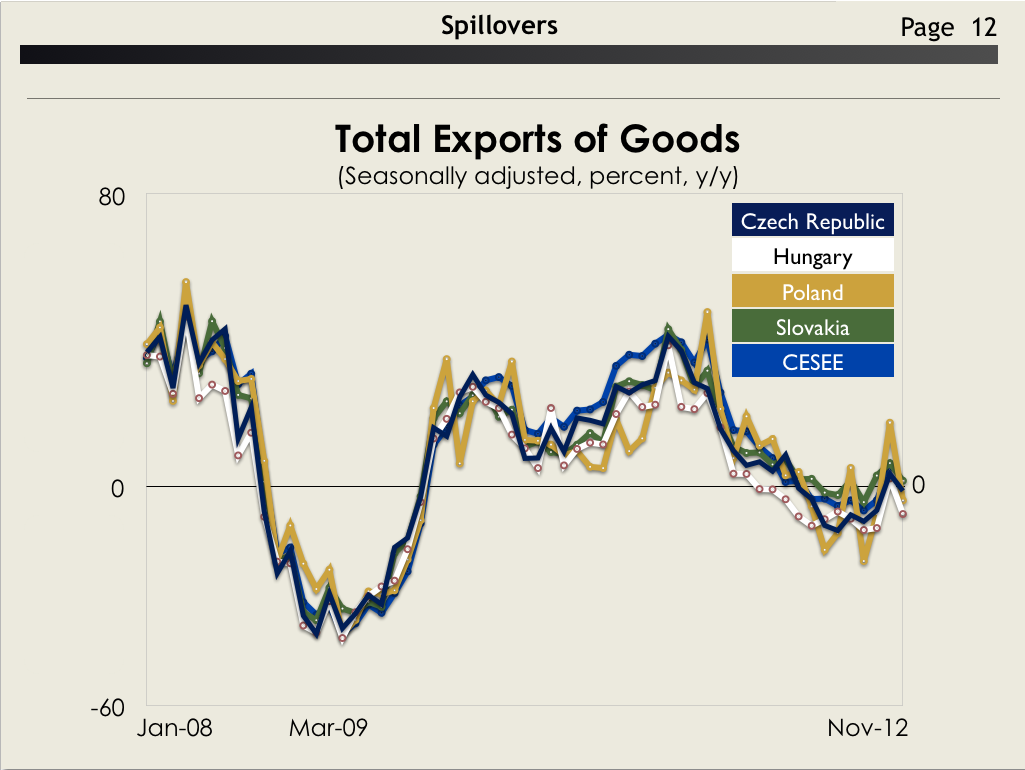

Meanwhile, there have been spillovers via trade, financial linkages, and confidence to Europe more widely. Growth has been weak even in economic powerhouses like Germany and in the emerging markets to the east.

All this argues for a more nuanced policy response by countries and European institutions that allows balance sheets to adjust but with minimum output and job losses:

Pressing ahead with orderly balance sheet repair at the national level, and supportive monetary policy and European Monetary Union architecture will help translate the financial market recovery into a real economic rebound.

Watch the video:

[youtube http://www.youtube.com/watch?v=dpgGkgAg2eE]